The economics of the airline industry are dreadful. Here are some reasons why I believe so.

- high fixed costs - employee, fuel, rents (terminal, etc),

- no pricing power - commodity like pricing which is often dependent on your competitor,

- violently cyclical - each time the economy sneezes, the industry catches a bad cold

- capital intensive - simply think of the cost of a single airplane,

- highly mobile capital assets - if one market is unprofitable, airplanes can be flown to the next location

- labor intensive - each large airline has tens of thousands of employees,

- asymmetric exposure to negative events - think 9/11,

- fluctuating raw material costs - no one really knows what oil prices will do next

- tight safety, security and other regulations leading to higher cost

Thus, it is easy to understand why Mr. Buffett has been so vocal in his opinions against the industry over the last three decades:

"Since our purchase of US Air, the economics of the airline industry have deteriorated at an alarming pace, accelerated by the kamikaze pricing tactics of certain carriers. The trouble this pricing has produced for all carriers illustrates an important truth: In a business selling a commodity-type product, it's impossible to be a lot smarter than your dumbest competitor." - 1990

"As the seat capacity of the low-cost operators expanded, their fares began to force the old-line, high-cost airlines to cut their own. ... Eventually a fundamental rule of economics prevailed: In an unregulated commodity business, a company must lower its costs to competitive levels or face extinction." - 1994 shareholder letter

"The worst sort of business is one that grows rapidly, requires significant capital to engender the growth, and then earns little or no money. Think airlines. Here a durable competitive advantage has proven elusive ever since the days of the Wright Brothers. Indeed, if a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down." - 2007

"Investors have poured their money into airlines ... for 100 years with terrible results. ... It's been a death trap for investors." - 2013

This is why it was mystifying when he recently bought large stakes in the four large airlines: American Airlines (NasdaqGS: AAL), Delta Air Lines (NYSE: DAL), United (NYSE: UAL) and Southwest Airlines (NYSE: LUV). So I decided to dig deeper into the airline industry, and found something that mystified myself even further.

Southwest Airlines ("Southwest" or the "Company") has not become bankrupt even once since it started flying in 1971. In an industry beset by bankruptcies, and where some airlines become bankrupt multiple times, this is quite an achievement.

Now get this - Southwest has never made a loss since 1973 - it has 44 consecutive years of profitability. This is a stunning achievement when you realize that this period includes the Arab oil embargo, the Gulf War, the 9/11 and the Great Recession. In fact, in the previous decade, the terrorist attack, a worldwide credit crisis, and the five-fold rise in energy prices have resulted in total financial losses for the US airline industry in excess of $50 billion.

You would be wrong to assume that it is because of their labor advantage. Southwest is one of the most unionized airlines in the US at 83%. And it has never fired or furloughed any employees, and almost never instituted pay-cuts. Its employees are in fact among the highest paid in the industry.

Southwest also does not have pricing power. In fact, they pride themselves on having among the lowest fares in the country.

And despite all this, the Company has not just survived, but thrived as indicated by the fact that it is a 145 bagger since 1980, a CAGR of approximately 15%. This made me very, very curious.

Business Model - Keep Fares Low, Keep Costs Lower, Have Fun

Southwest's business model can be summed up in one sentence as articulated by co-founder, Chairman Emeritus and former CEO of Southwest Herb Kelleher:

"If we offer our customers a quick, safe and convenient mode of transportation at a very low fare (rivaling that of land travel) and ensure they have a little fun too, why would they choose anything else?"

Southwest's strategy is to keep fares low and volumes high. Any new route Southwest enters has to have enough local traffic which would support this business model. The principal strategy has been the same since its inception: Focus on the local short-haul traveler, keep the fares low which would increase demand for air travel, provide services at high frequency and ensure the customers have fun. Here is a little example of the fun provided by Southwest.

After zeroing in on a city, Southwest would enter the market with low fares, often much lower than that of the incumbent carriers there. This would lead to the other airlines slashing their fares as well. The lower fares would drive up the traffic as more customers begin choosing air travel; in some cities the traffic has risen by 300%-500%. And within a short time, Southwest substantially increases the number of flights from that city to ensure the customers have frequent, conveniently timed options. This phenomenon has actually been named by the Department of Transportation as the 'Southwest effect' in the early 1990s.

By keeping fares low and following up with multiple conveniently timed flights, the Company increases its market share in its cities of operation. It is in most cases the largest or the second largest airline in its markets by customers. Larger volumes of customers allow it to spread its fixed costs (ground employees, facilities' rents) across a larger base, ensuring that the Company has a low unit cost of operation per customer. This low unit cost further reinforces its ability to charge low fares and still maintain a profit. The frequent flight availability also ensures customer loyalty.

Because the focus is primarily on the local short-haul customer, aircrafts are scheduled on a point-to-point, not hub-and-spoke basis. The hub-and-spoke system concentrates most of an airline’s operations at a limited number of central hub cities and serves most other destinations in the system by providing one-stop or connecting service through a hub. Any issue at a hub, such as bad weather or a security problem, can create delays throughout the system. Additionally, an extra stop results in unnecessary delays for the passengers. By not concentrating operations through one or more central transfer points, the Company’s point-to-point route structure allows for more direct non-stop routing than hub-and-spoke service and therefore allows better control over delays and total trip time. Also, direct passenger base is more resilient than connecting passenger base, as the passengers might be agnostic to which connecting hubs they fly through.

The fanatic focus on costs comes across in other avenues as well. The Company uses a single class of airplanes - the Boeing 737. This has multiple advantages. This allows for simplified scheduling, maintenance, operations, and training activities, which in turn substantially lower costs. It also increases the safety of operations as the maintenance personnel and pilots have to get familiar with a single type only. And it also makes Southwest the largest customer for this type, reducing capital costs.

Another focus is on providing services from downtown or secondary airports in different cities as opposed to the major airports. These conveniently located airports are typically less congested than other airlines’ hub airports, which has enabled Southwest to achieve high asset utilization because aircraft can be scheduled to minimize the amount of time they are on the ground. This, in turn, has reduced the number of aircraft and gate facilities that would otherwise be required and allows for high employee productivity (headcount per aircraft). Southwest has a less than 25-minute turn philosophy which means the planes on average spend less than 25 minutes on the ground in each airport before they take off again.

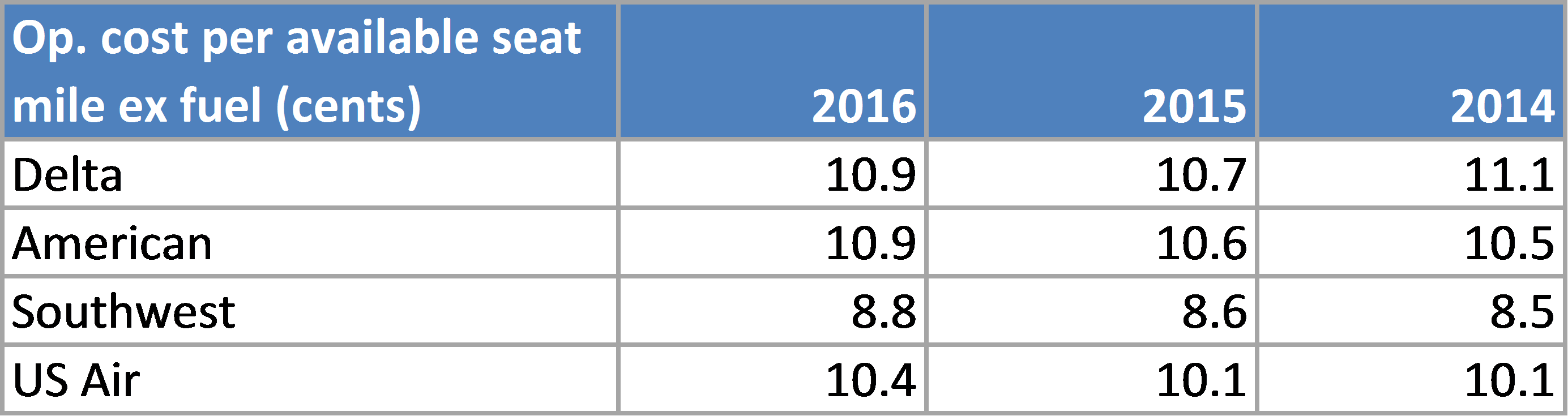

The net effect of the strategy is that Southwest has become the largest domestic air carrier in the United States, as measured by the number of domestic originating passengers boarded. The company also has among the lowest unit costs per available seat mile (ASM) among its peers. ASM is an indicator of an airlines passenger carrying capacity and is calculated by the seats available * miles flown.

Further benefits of low costs: The low-cost structure allows the Company to levy fares which are very low and without any hidden components. Southwest continues to be the only major U.S. airline that offers up to two checked bags that fly free. In addition, regardless of the fare product, Southwest does not charge fees for changes to flight reservations. Also unlike most of its competitors, Southwest does not impose additional fees for items such as seat selection, snacks, curb-side check-in, and telephone reservations. In addition, Southwest allows each ticketed Customer to check one stroller and one car seat free of charge, in addition to the two free checked bags. These factors which delight the customer, further increase their loyalty.

People: The Most Important Pillar

"If the employees come first, then they’re happy... A motivated employee treats the customer well. The customer is happy so they keep coming back, which pleases the shareholders. It’s not one of the enduring green mysteries of all time, it is just the way it works." - Herb Kelleher

The Southwest leadership frequently refer to the employees as their most important focus and it is easy to understand why. The airline industry is labor intensive and a successful airline takeoff requires near perfect coordination amongst diverse departments - pilots, flight attendants, baggage handlers, booking officials, and ground staff. The downside to any mishap can be calamitous. Also, to keep your end customers (who are hurtling through the air at high speeds, thousands of feet above the ground in a small metal tube) calm and happy enough so that they keep coming back is not an easy task.

Southwest leadership has put employees first, customers second and shareholders third. Happy employees would take good care of the customers which would then lead to good returns for the shareholders. So how does the Company ensure a great culture and happy employees?

Good cost, bad cost routine: While Southwest is quite fanatic about keeping costs low, it is important to remember that the focus is on bad costs. For example, most Southwest flights do not have elaborate meals and have basic snacks given to the customers. However, they are quite generous on the amounts they spend on its employees.

Southwest was the first airline to institute a profit-sharing plan, which it implemented in the first year it generated profits way back in 1973. Employees are in fact one of the largest shareholders in the organization. This incentive alignment between the shareholders and the employees are a major reason for the success of the Company. As employees are the major shareholders, there is a sense of ownership amongst them which has come out on multiple occasions when the Company was in trouble. Additionally, Southwest pays its employees above average wages when compared with the industry. Employees are also given substantial freedom to make their own decisions. Southwest has a separate department called 'Culture Services' whose primary role is to take care of employees, ensure their happiness and maintain the culture of the organization. The department includes various teams like:

- Internal customer care team which supports employees who have "life events" take place, such as the birth of a baby, the death of a family member, or a serious illness in the family.

- Customer communications team which pass along all praise from customers to Southwest’s employees. If the letter is vague, there are researchers whose job is to identify which employee was referred to. Every employee who receives positive feedback from a passenger receives a commendation directly from the CEO.

- Celebrations, festivities, and banquets.

- Culture committee team whose major role is to help employees across the field to perform service projects that range from grilling burgers for baggage employees to arranging a "Pizza Day" for employees in the airport or setting up an ice cream bar for fellow employees on busy travel days to show appreciation for the hard work.

When this is combined with the fact that the Company has never furloughed employees in an industry rife with bankruptcies or induced pay cuts, one can understand the powerful loyalty Southwest enjoys. Employees love their work and highly value their association with Southwest. And it has repaid Southwest in multiple ways including better productivity, better customer service (topped the customer satisfaction index >15 times in the last 25 years) and resourcefulness. The investment in these good costs go a long way in strengthening Southwest's competitive advantage. In fact, I would assess the extra spending on employees to be capex and not opex as the benefits of the same accrue over a long period, as is evident from below.

Institutional Spirit: How Goliaths created David

Southwest's tale, since its inception, has been a tale of spirit. When Herb Kelleher and Rollin King decided to start the airline in 1968 as a Texas intrastate carrier, the incumbent airlines tied them up in litigation (arguing that there were enough carriers in Texas) for three-and-a-half years trying to shut them down before they even began. Kelleher, a lawyer by profession, worked for free to ensure Southwest takes off. His tenacity was due to the belief that he was fighting for the American spirit of free enterprise. The first flight finally took off in 1971.

In 1973, Braniff began the $13 Fare War offering a $13 fare from DAL to HOU (Southwest's only profitable route then). Southwest responded by offering customers the choice of a $13 fare or a free bottle of premium liquor with every full fare ticket ($26). (Southwest became the largest distributor in Texas of Chivas, Crown Royal, and Smirnoff for the following two months). Needless to say Southwest won this war.

Southwest was barely able to pay its employees in the beginning years (due to competitive intensity and its small scale). The way it solved it was interesting, it sold one of its four jets to pay its employees and ran a four jet schedule using three jets. This was the origin of the asset sweating approach that later became a big part of the Southwest strategy: customers pay to be in the air not to be on the ground.

In the early 1970s, all airlines in Dallas shifted to the larger, newly constructed DFW airport (from Love Field) as part of the agreement made in late 1960s. Southwest was not part of the agreement and refused to move as it would compromise its operations. The other airlines dragged Southwest to the courts again where the verdict allowed Southwest to remain at Love Field as long as the airport remained open. And when in 1978, the airline industry was deregulated, the airlines and DFW airport through Jim Wright, the Congressman of Fort Worth passed the Wright amendment which severely restricted Southwest's operations from Love Field (flights only to neighboring states; even connecting flights were not allowed). This amendment was finally changed post-2005. Even within the stifling constraints in their home market, Southwest found ways to grow steadily due to the doggedness of the leadership and the employees.

In the 1990s, to combat the growing threat of Southwest, the giants of the industry including United and American started low-cost services under different sub-brands at core markets of Southwest. Driven by this, Southwest lowered its costs further, making it even more competitive. What the competing airlines did not realize was that Southwest employees owned a major stake in the Company and were fiercely loyal. The culture of loyalty and low cost had been developed over long years by design and strengthened by adversity. While the competing airlines designed the tangible, they were unable to match the intangible - the culture of loyalty and frugality. Within a few years, all the incumbents reduced or closed down their LCC operations.

In addition to the above, at the same time the computer reservations systems (CRSs) used by travel agencies owned by United Airlines (Apollo) and Continental Airlines (System One) disabled automated ticketing for Southwest travel. Southwest decided to counter this by introducing 'ticketless' travel, introduced its own CRS for very high volume travel agencies (TAs), and other effective ticket delivery systems for other customers. In fact, because of its ouster from the traditional distribution system, the Company's resourcefulness enabled it to develop its own new system which helped it lower the costs further in the long-term.

What comes across is a pattern of thriving under adversity. I believe that Southwest is this strong today because it was bullied by the competitors, not unlike how David became David because of Goliath. And given this institutional spirit, adverse conditions would be beneficial for Southwest's strength as it would come out stronger.

Conservatism: Manage Good Times To Prepare For The Bad Times

“My employees know that if anybody talked about seat market share I would punch their nose. I would rather have a 5% market share and be profitable rather than have a 90% market share and be unprofitable… We decided that while we may have a Maverick marketing image in the marketplace, we will maintain a very conservative financial structure to ensure our survival.” - Herb Kelleher

Discipline and conservatism in the financial policy and is a major pillar on which the Southwest empire rests. Despite more than four decades of consistent profitability, the strategy continues to be expansion within means and within its circle of competence. Southwest only expands to markets where they believe they can implement their strategy, and have never over-extended themselves. They had no international flights till after 2010! This uncommon discipline allowed them to expand and take profitable market share in both benign and difficult conditions. For example, when the airline market was reeling from 2001 to 2005 as a result of 9/11 (one of the worst periods of airline distress) and generated losses in excess of $5 billion, Southwest continued to remain profitable and actually increased the passengers carried by a 5% CAGR and the fleet size by 90 planes!

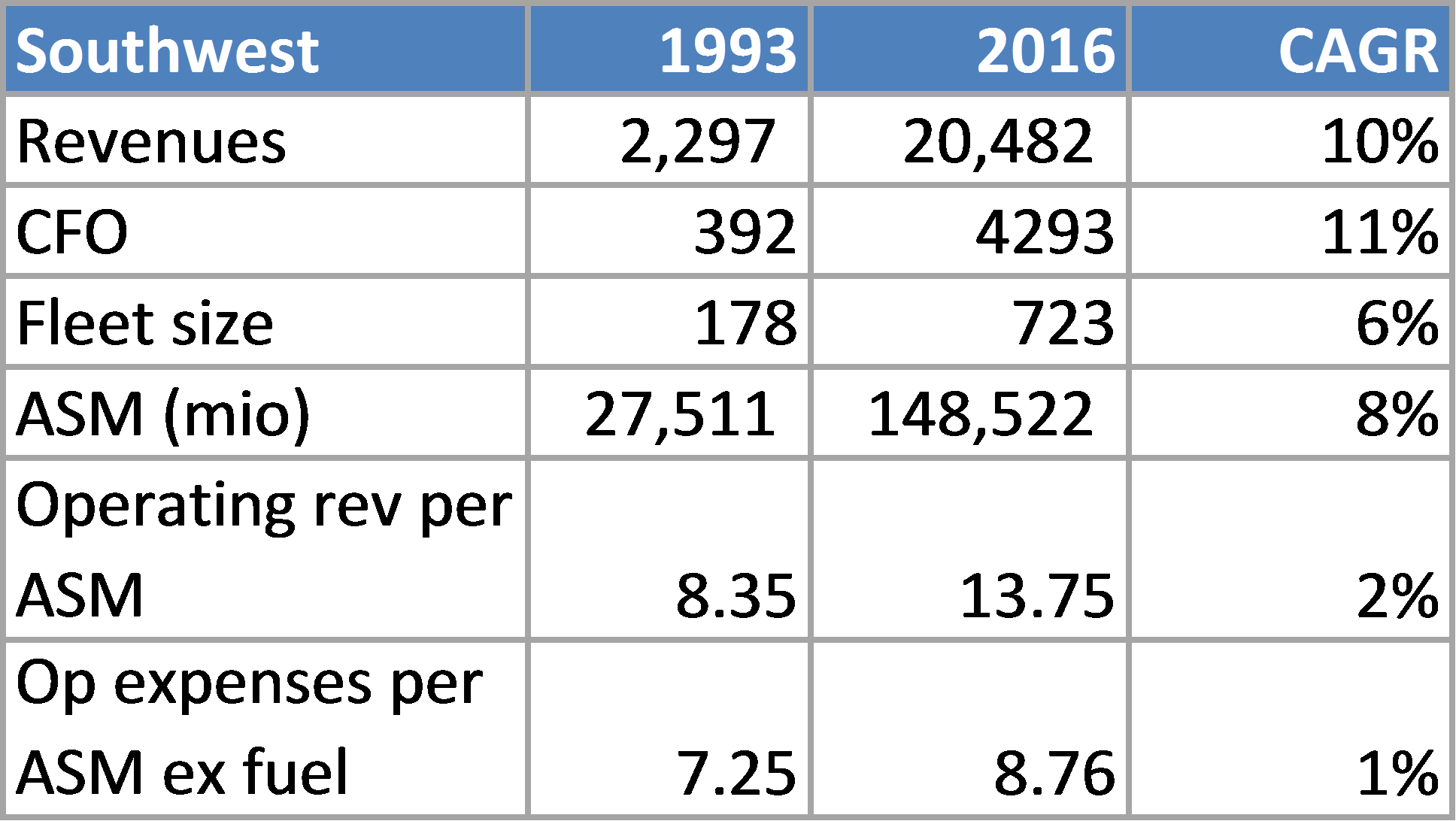

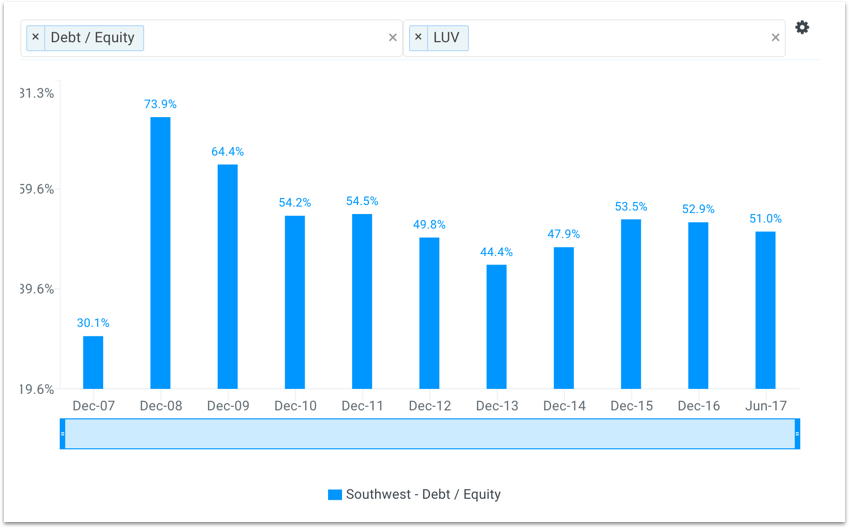

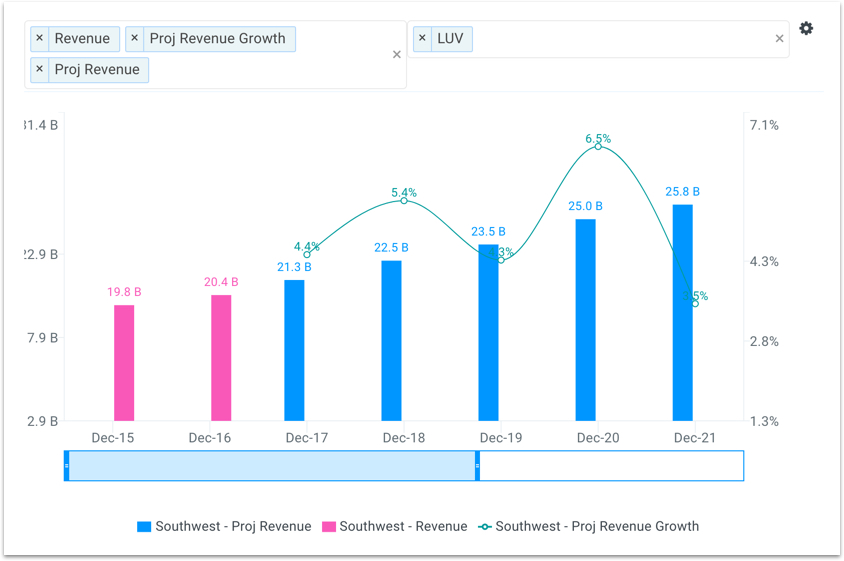

The focus on growth is better evident from the table above. From 1993 to 2016, revenues have grown at a healthy annual pace of 10%. The entire growth is primarily driven by the addition of airplanes, while the fare increase has been small. The extremely low operating expense increase driven by multiple initiatives and motivated employees are an important competitive strength as discussed previously. Throughout the entire period, the Company has maintained a very conservative capital structure, and the debt to equity has never been above 100%.

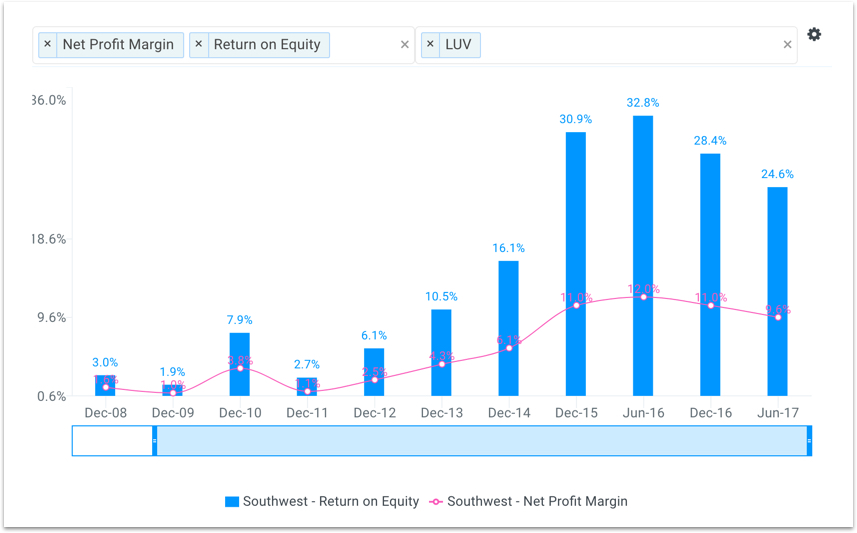

The graph below indicates the movement in margins and returns on equity over the prior ten years. The low margins and returns in the early part of the last decade was a result of the Great Recession and uncertainty from and high oil prices.

However, a couple of developments in this decade indicate that the future of the airline industry could potentially be quite different. First, the slew of bankruptcies and consolidation among the airlines has greatly reduced the capacity in the industry. This is evident from the very high load factors observed across the industry (>80%) over the last few years, highest in the last two decades.

In addition, the period of high fluctuations in oil prices may have come to an end due to two reasons: reduced demand for oil, driven by electric cars, and better technology for drilling and extraction which would make production cost effective at lower prices. This is reflected in the growing margins and returns observed for all airlines.

Very Attractive Valuation

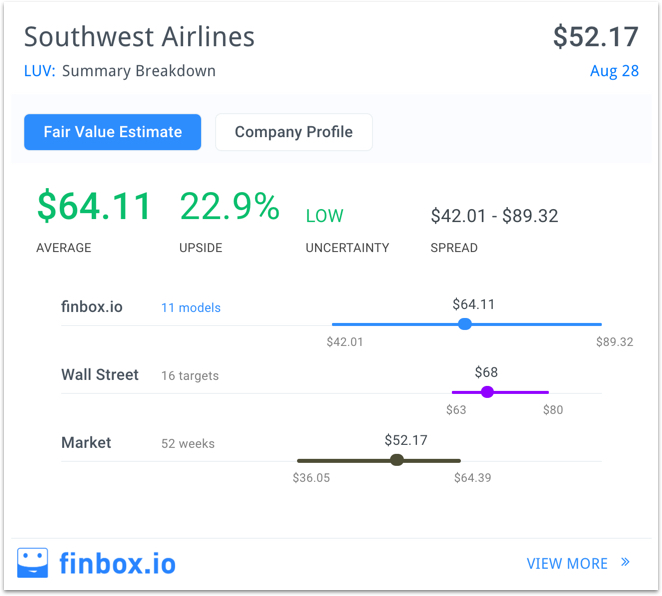

Using multiple approaches for valuation is important. If all approaches point to undervaluation, then investors should be quite excited about the prospect of a stock. Finbox.io calculates a fair value estimate of just over $64 per share for Southwest implying that the stock has over 20% upside. Nine of the eleven valuation analyses used to determine Southwest's fair value indicates that shares are undervalued.

For the five-year projections, we have used a 5% CAGR growth in revenues for the next five years, and EBITDA margins are projected to remain nearly flat around 24%. For the 10-year projections, we have taken revenue CAGR of 5% for the first five years and 3% for the next five years, while the EBITDA margins are projected to remain at approximately 24%. Overall, this forecast is conservative based on the company's recent performance.

The list below indicates the fair value based on each discounted cash flow approach using the above forecast along with the upside from the current price at the time of writing ($52.17). Overall, the company appears to be quite undervalued.

- 5-Year DCF Model: Gordon Growth Exit = $89.32 (70%)

- 5-Year DCF Model: EBITDA Exit = $72.86 (38%)

- 5-Year DCF Model: Revenue Exit = $59.29 (13%)

- 10-Year DCF Model: Gordon Growth Exit = $84.31 (60%)

- 10-Year DCF Model: EBITDA Exit = $72.51 (38%)

- 10-Year DCF Model: Revenue Exit = $62.78 (19%)

Risks To The Thesis

Industry risk: Airline industry has historically been one of the most brutal industries to operate in. The business model risk discussed in the beginning continues to exist for Southwest.

Competition: While Southwest has been successfully been able to counter the competition from the incumbents who have been unable to match the nimbleness of Southwest, the competition from new generation players like Jetblue and Spirit is quite real. These newer players have been able to emulate Southwest successfully so far.

Oil prices: It is extremely difficult to predict what oil prices will do next.

Conclusion: Buy and Hold

Southwest runs its business in a way that generates a net benefit to society. It has created a beautiful virtuous cycle: low fares and high frequency attracts more customers, which leads to more revenues, which in turn results in more money and amenities for the employees, who in turn take great care of the customers. New and repeat customers lead to more capital to conservatively self-fund expansion to newer markets and repeating the process again. It has all the features of a franchise that Charlie Munger likes best. It delivers essential service to society at a low cost and takes care of all stakeholders: employees, customers, shareholders, government (no bailouts and regular taxes), and runs the business in a way that minimizes inefficiency and waste.

Note this is not a buy or sell recommendation on any company mentioned.

Photo Credit: Southwest

{kind=link}