Authors of Commonsense Corporate Governance Principles

- A consortium of CEOs and money managers recently released a series of Commonsense Corporate Governance Principles on Thursday, July 21st.

- One of the principles provides a recommendation for companies to eliminate quarterly earnings guidance.

- In this post I'll explain the reasoning for the recommendation and how it impacts fundamental investors and valuations.

The Problem

Management of public companies frequently manipulate quarterly earnings because their compensation is often directly tied to the company’s stock performance - there are typically big swings in a company’s stock performance when reported earnings don’t meet management’s guidance or Wall Street expectations.

Earnings tinkering is no secret and has been an issue for years. However, it’s currently in the spotlight (as it should) because Warren Buffett, one of the Commonsense authors, told CNBC that “Guidance can lead to a lot of malpractice... There's a lot of attempts to find a couple extra pennies someplace. There are ways to move earnings toward the end of a quarter, and sometimes even after the end of a quarter.” The interview can be viewed in the video below.

Manipulating Earnings

Net income and earnings per share (EPS) are metrics that investors frequently follow during earnings season. However, they can often misrepresent the true operating performance of a company due to accounting malpractice. A few ways management teams massage earnings:

- Adjusting an asset's useful life (depreciation). A non-cash expense that runs through the income statement.

- Selling assets for one-time gains which is then added to earnings.

- Capitalizing expenses to the balance sheet rather than running them through the income statement

- Inflating revenue: recording sales prior to completing all services.

Unfortunately, these accounting adjustment are afforded to management teams by the Generally Accepted Accounting Principles (GAAP).

In addition, SEC filings often include supplemental non-GAAP earnings which are based on whatever logic management finds suitable. Barron’s touched on this issue in a recent article (which finbox.io was featured in) explaining that 92% of companies using non-GAAP measures make earnings look better by excluding real operating expenses.

Quarterly earnings discrepancies have become so distorted that even SEC Chair Mary Jo White has publicly suggested that new regulations may be needed. And now with Warren Buffett’s comments bringing this issue into the national spotlight, what type of changes can be expected?

The Solution: Scrap Earnings Guidance

The Commonsense Corporate Governance Principles recommends that less companies report short-term guidance and focus rather on longer-term shareholder value. Warren Buffett suggests that management should “report two real numbers; this year versus last year.”

The hope is that by eliminating quarterly earnings guidance, management's focus will turn to long-term results which in effect will reduce financial statement malpractice.

Should we expect real changes?

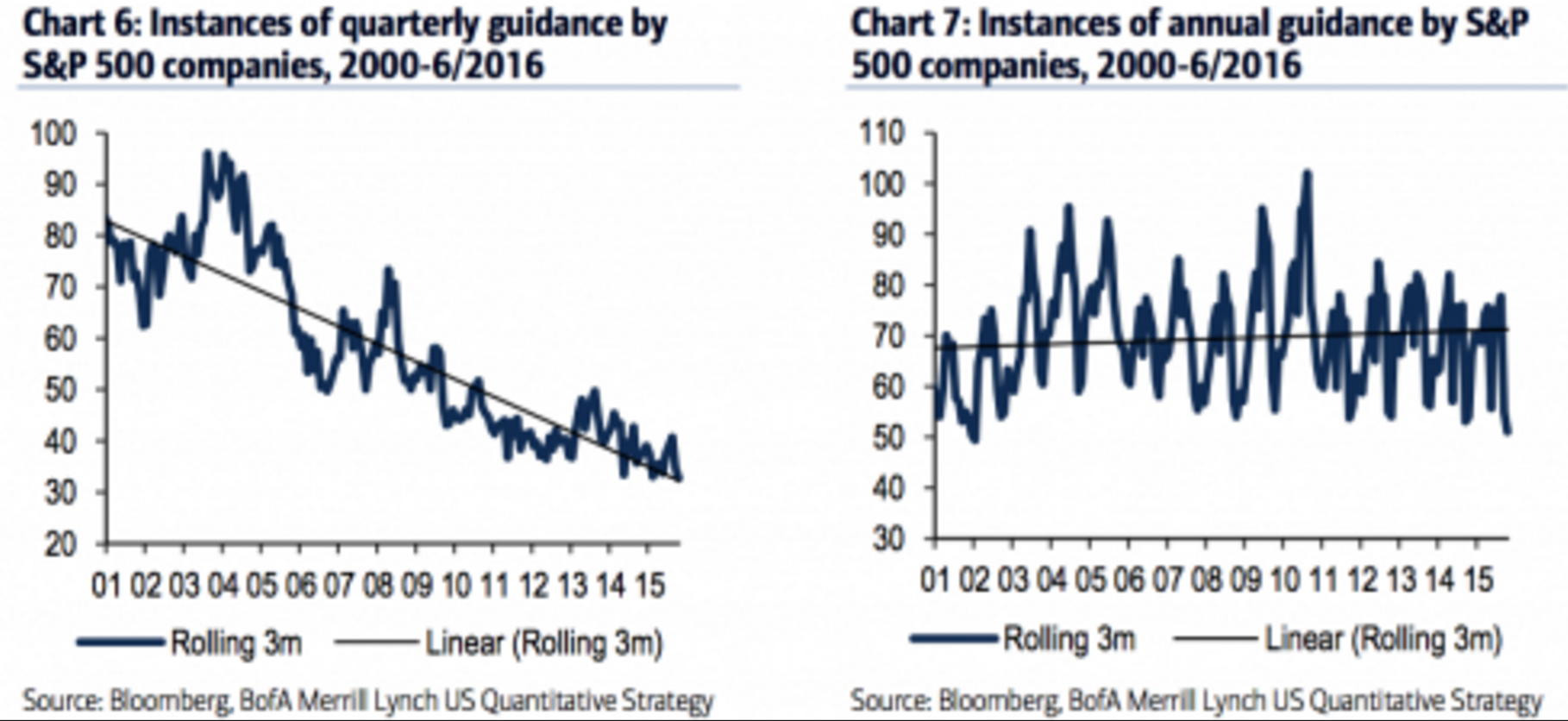

There’s already a trend towards giving less short-term guidance as reported by Yahoo Finance. The article shares data compiled by Bank of America Merrill Lynch’s Savita Subramanian saying, “Corporates have gradually been doing away with quarterly guidance (but maintaining annual guidance) in what may be a shift away from short-termism.”

Charts highlighting this trend:

<img width="100%" src='http://res.cloudinary.com/finbox/image/upload/v1469206023/Earnings_Guidance_Instances_yujbmx.png' alt= ‘Earnings Guidance Trends’>

How does this impact investors?

This is great news for fundamental investors and finbox.io because it will improve:

- The accuracy of reported earnings

- The accuracy of finbox.io fair value estimates

The most obvious impact of these trends is that reported earnings will become a more accurate representation of a company’s true operating profit. Earnings data will improve with management focusing more on long-term shareholder value.

Note that finbox.io members never rely on window dressing figures. Company data has and will continue to be adjusted for unusual items (adjustments can be viewed in the historical financials model).

Better data means better inputs and assumptions

Finbox.io’s financial models already take a long-term fundamental view of a company. Our discounted cash flow (DCF) models forecast company earnings over 5 and 10 year periods. The assumptions driving these models will undoubtably improve as company data improves. This means that finbox.io’s fair value estimates, which provides a great starting point for figuring out how much a stock is really worth, will become even more accurate.

Finbox.io is continuously adding measures to improve the accuracy and reliability of our fair value estimates. This is why we recently added uncertainty ratings which you can learn more about here.

The elimination of quarterly earnings guidance is a win for all fundamental investors.

Get Started Now!

This article was written by Matt Hogan.

{kind=link}

{kind=link}