GrubHub Inc (NYSE: GRUB), an information technology firm with a market capitalization of $9.6 billion, saw its share price increase by 54.0% over the prior three months. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. But is there still an opportunity here to buy? Let’s examine GrubHub's valuation and outlook in more detail to determine if there’s still a bargain opportunity.

What Is GrubHub Worth?

According to our 9 valuation models, GrubHub seems to be fairly priced in the market at 2.3% above its intrinsic value. This means if you were to buy GrubHub today, you'd be paying a reasonable price for it. If you believe that the stock is really worth $103.46, then there isn’t much room for the share price to appreciate beyond where it’s currently trading.

| Analysis | Model Fair Value | Upside (Downside) |

|---|---|---|

| 10-yr DCF Revenue Exit | $145.10 | 37.0% |

| 5-yr DCF Revenue Exit | $137.11 | 29.4% |

| Peer Revenue Multiples | $62.58 | -40.9% |

| 10-yr DCF EBITDA Exit | $130.24 | 22.9% |

| 5-yr DCF EBITDA Exit | $110.49 | 4.3% |

| Peer EBITDA Multiples | $54.16 | -48.9% |

| 10-yr DCF Growth Exit | $129.66 | 22.4% |

| 5-yr DCF Growth Exit | $108.82 | 2.7% |

| Peer P/E Multiples | $52.97 | -50.0% |

| Average | $103.46 | -2.3% |

Click on any of the analyses above to view the latest model with real-time data.

In addition, it seems like GrubHub’s share price is quite stable, which could mean there may be less chances to buy low in the future now that it’s fairly valued. This is because the stock is less volatile than the wider market given its beta of 0.61.

How Much Growth Will GrubHub Generate?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company’s future expectations.

source: finbox.io data explorer

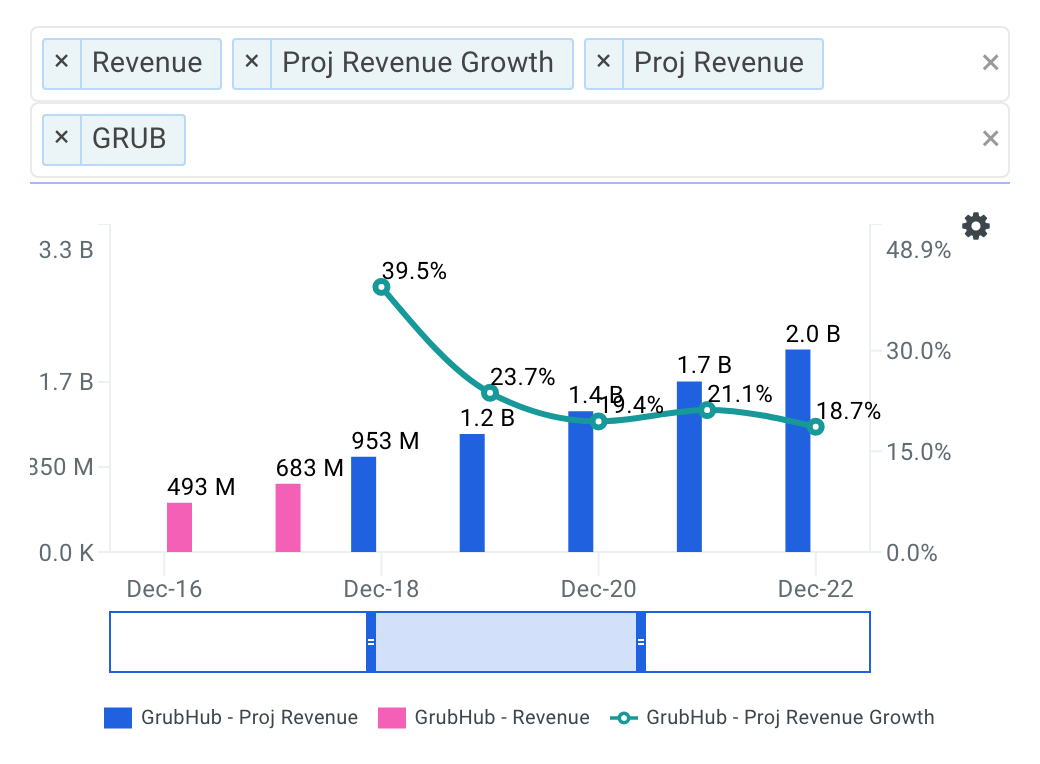

GrubHub's revenue growth is expected to average 24.3% over the next five fiscal years, indicating a solid future ahead. Unless expenses grow at the same level, or higher, this top-line growth should lead to robust cash flows, feeding into a higher share value.

Why Combine Value And Growth Techniques?

While many investors tend to categorize stocks as either value or growth plays, the most successful investors view growth in conjunction with a company's value. Take legendary investor Peter Lynch for example, who is widely known for popularizing the term growth at a reasonable price (GARP).

GARP is a strategy that combines aspects of both growth and value investing techniques by finding high growth companies that don't trade at overly high valuations. In the application of this strategy, Lynch achieved 29% annualized returns as the manager of Fidelity's Magellan Fund from 1977 to 1990. Needless to say the importance of analyzing a company's fair value in addition to its growth prospects.

Unfortunately, GrubHub's optimistic future growth appears fully factored into the current share price with the stock now trading near its intrinsic value. As a shareholder, you may have already conducted your fundamental analysis on the company and the stock's recent 54% appreciation may have been expected. Therefore, it may be time for investors to take some chips off the table. For prospective investors looking to purchase shares of GrubHub, it may be worth holding off until the stock develops a wider margin of safety.

However, if you have not done so already, I highly recommend you complete your research on GrubHub by taking a look at the following:

Valuation Metrics: how much upside do shares of GrubHub have based on Wall Street's consensus price target? Take a look at our analyst upside data explorer that compares the company's upside relative to its peers.

Risk Metrics: what is GrubHub's CapEx coverage? This is the amount a company outlays for capital assets for each dollar it generates from those investments. View the company's CapEx coverage here.

Forecast Metrics: what is GrubHub's projected EBITDA margin? Is the company expected to improve its profitability going forward? Analyze the company's projected EBITDA margin here.

Author: Andy Pai

Expertise: financial modeling, mergers & acquisitions

Andy is also a founder at finbox.io, where he's focused on building tools that make it faster and easier for investors to do investment research. Andy's background is in investment banking where he led the analysis on over 50 board advisory engagements involving mergers and acquisitions, fairness opinions and solvency opinions. Some of his board advisory highlights:

- Sears Holdings Corp.'s $620 mm spin-off via rights offering of Sears Outlet, Hometown Stores and Sears Hardware Stores.

- Cerberus Capital Management's $3.3 bn acquisition of SUPERVALU Inc.'s New Albertsons, Inc. assets.

Andy can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

%20When%20Prices%20Drop%3F){kind=link}