Value investors long these three stocks may want to re-evaluate their positions amidst the recent insider activity.

Insider Selling: Simpson Manufacturing Co

Sharon Simpson, Trustee of the Barclay and Sharon Simpson 2007 Trust, sold 120,825 shares of Simpson Manufacturing Co (NYSE: SSD) worth a total of $7.2 million on Tuesday, January 30.

What's more interesting in fact, Simpson has sold $41.5 million worth of stock since the beginning of December according to MarketBeat. That's roughly 1.5% of the company's total market capitalization.

The company's shares last traded at $58.85 as of Wednesday approximately 95.8% of its 52-week high. While the stock is near its high, could the recent insider transactions signal a troubling road ahead for shareholders?

| Analysis | Model Fair Value | Upside (Downside) |

|---|---|---|

| 10-yr DCF Revenue Exit | $40.95 | -30.4% |

| 5-yr DCF Revenue Exit | $42.67 | -27.5% |

| Peer Revenue Multiples | $39.74 | -32.5% |

| 10-yr DCF EBITDA Exit | $52.07 | -11.5% |

| 5-yr DCF EBITDA Exit | $59.64 | 1.3% |

| Peer EBITDA Multiples | $49.67 | -15.6% |

| 10-yr DCF Growth Exit | $37.08 | -37.0% |

| 5-yr DCF Growth Exit | $36.76 | -37.5% |

| Peer P/E Multiples | $58.94 | 0.2% |

| Dividend Discount Model | $30.05 | -48.9% |

| Dividend Discount Model (multi-stage) | $32.64 | -44.5% |

| Earnings Power Value | $31.49 | -46.5% |

| Average | $42.64 | -27.5% |

| Median | $40.35 | -31.4% |

Finbox.io applies pre-built valuation models to calculate a fair value for a given stock and uses consensus Wall Street estimates for the forecast when available. The company's average fair value of $42.64 implies -27.5% downside and is calculated from 12 separate analyses as shown in the table above.

Insider Selling: Seritage Growth Properties

Bruce Berkowitz is the founder of Fairholme Capital Management and in 2009, he was named the DS fund manager of the decade by Morningstar. Fairholme owned $173.5 million worth of Seritage Growth Properties (NYSE: SRG) stock as of September 30th which was reported by the fund's 13F filing with the SEC.

This position represented 19.1% of the firm's stock portfolio. However, Berkowitz has been reducing his position in Seritage Growth Properties since November. Fairholme has sold 1,205,400 shares worth $49 million which has effectively cut his position by 28%.

Seritage Growth Properties is a publicly-traded REIT with 230 wholly-owned properties and 28 joint venture properties totaling over 40 million square feet of space across 49 states and Puerto Rico. The Company was formed to unlock the underlying real estate value of a high-quality retail portfolio it acquired from Sears Holdings in July 2015.

Shares of the company are up 3.3% over the last year offering minuscule returns for investors. The stock last traded at $41.06 as of Wednesday and 7 separate valuation analyses imply that there is 25.6% downside relative to its current trading price.

| Analysis | Model Fair Value | Upside (Downside) |

|---|---|---|

| 10-yr DCF Revenue Exit | $24.34 | -40.7% |

| 5-yr DCF Revenue Exit | $24.54 | -40.2% |

| Peer Revenue Multiples | $33.38 | -18.7% |

| 10-yr DCF EBITDA Exit | $33.53 | -18.3% |

| 5-yr DCF EBITDA Exit | $36.49 | -11.1% |

| Peer EBITDA Multiples | $39.13 | -4.7% |

| Dividend Discount Model (multi-stage) | $22.40 | -45.5% |

| Average | $30.54 | -25.6% |

| Median | $33.38 | -18.7% |

Although Fairholme has been reducing its position, it is important to note that the hedge fund still owns more than 3 million class A common shares.

Insider Selling: At Home Group

A number of top executives have been selling shares of At Home Group (NYSE: HOME) according to MarketBeat including Lewis Bird III (CEO), Judd Nystrom (CFO), and Peter Corsa (COO). Total insider selling has totaled $12.3 million in the month of January alone representing almost 1% of At Home Group's market capitalization.

At Home Group operates home decor superstores in the United States. The company’s stores offer items such as accent furniture, frames, pottery, bar stools, garden décor, rugs and mats, bedding and bath products, beds and mattresses. As of November 15, 2017, it operated 150 stores in 34 states. The company was founded in 1979 and is headquartered in Plano, Texas.

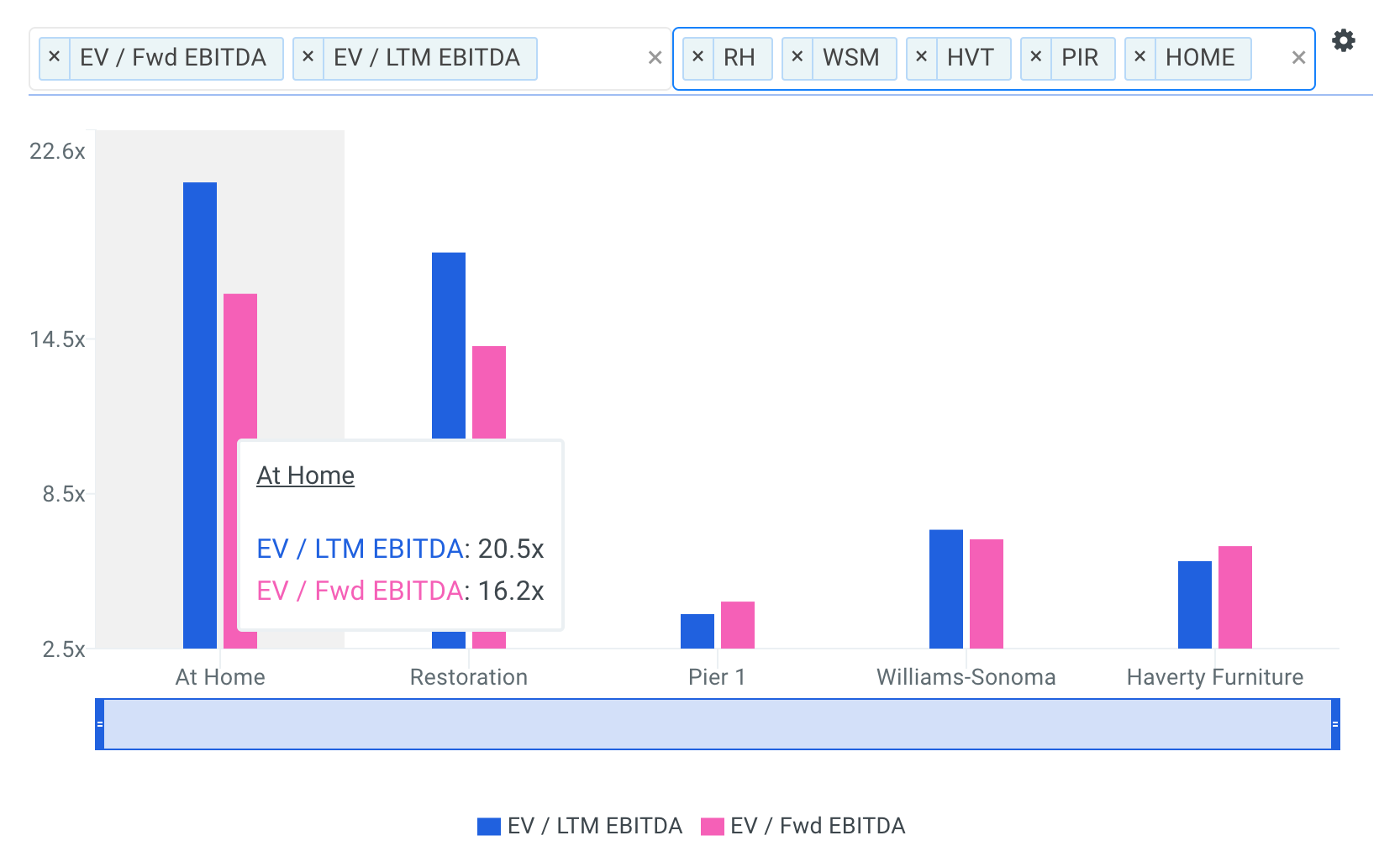

Analysts covering the stock often compare the company to a peer group that includes Haverty Furniture (NYSE: HVT), Williams-Sonoma (NYSE: WSM), Pier 1 Imports (NYSE: PIR) and Restoration Hardware (NYSE: RH). Analyzing At Home Group's valuation metrics and ratios provides further insight into why these insiders may be selling their shares.

A company's EBITDA multiple is calculated by dividing its Enterprise Value by EBITDA and is often used to benchmark the fair market value of a company. Its key benefit over the P/E multiple is that it's capital structure-neutral, and, therefore, better at comparing companies with different levels of debt.

At Home Group's LTM EBITDA multiple of 20.5x is above all of its selected comparable public companies: HVT (5.9x), WSM (7.1x), PIR (3.8x) and RH (17.8x). The company's Forward EBITDA multiple of 16.2x is also above all of its selected peers.

source: finbox.io

Shares of At Home Group are up 55.5% over the last three months and up 112.1% over the last year. Although investors have enjoyed the recent gains, the stock's valuation is becoming stretched which is likely the reason for the insider transaction.

While insider activity on its own is not necessarily a buy or sell signal, it may offer insight into how ownership and management feel about a company's future prospects. Keeping an eye on the activities of insiders and institutions can help investors make more informed investment decisions.

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

{kind=link}