- U.S. oil and gas production is hitting records after surviving OPEC’s price war. The continued recovery of oil prices is driving investment back into shale oil drilling. Oilfield service companies are big beneficiaries of this expansion.

- RPC specializes in providing services for recovering shale oil. Its biggest money maker is pressure pumping (hydraulic fracturing). This zero-debt firm is doubling its capex in 2018, and rewarding shareholders with an expanded repurchase program and higher dividend.

- Most of RPC’s peers had negative profits in 2017, making relative valuations unreliable. However, Wall Street analysts are calling for 22.5% price appreciation. Quant-based valuations confirm the potential, with expectations for a 19.5% upside.

U.S. Oil Production Rises from the Ashes

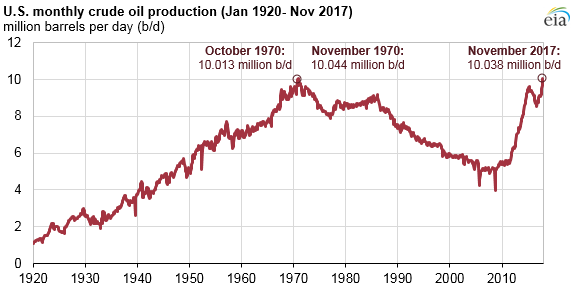

In November 2014, OPEC and Russia picked a fight with the U.S. oil industry, namely shale oil producers. With the goal of shutting down the higher-cost wells, the cartel drove prices down, cratering the number of operational oil rigs and denting production. However, the industry has managed to rebound to record levels, producing 10.381 million barrels per day as of last week and surpassing the November 1970 high (chart below). The U.S. Energy Information Administration (EIA) also expects U.S. natural gas production to hit all-time levels this year. As oil prices continue to rise, more production will come online, a major concern for some OPEC members, especially Iran who is at loggerheads with Saudi Arabia about letting prices rise any further.

Source: U.S. Energy Information Administration

The price for U.S. benchmark West Texas Intermediate (WTI) crude crossed above $60 recently for the first time since January 2014; great news for producers and oilfield service companies. The EIA expects oil prices to remain stable around the current level over the next few years. Aside from price support due to the discord in OPEC, a floor on U.S. prices was put in place in 2016 when a four decade ban on exporting oil was removed. While the infrastructure is still being built up, only one port on the Gulf Coast can handle the largest tankers (VLCC’s), exports have taken off quickly. Additional customers for previously land-locked oil will help prevent gluts that can drive prices down.

Source: U.S. Energy Information Administration

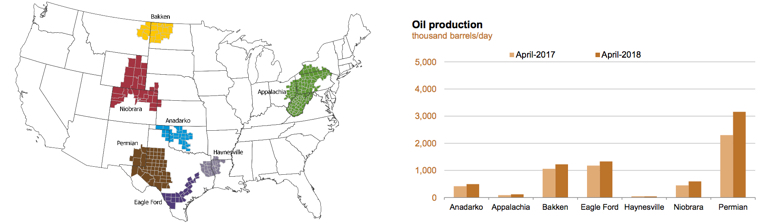

One of America’s most fruitful “tight” oil producing regions is the Permian Basin. Tight oil, another name for shale oil, made up 54% of U.S. oil production in 2017 according to the EIA. The Permian, shown in brown on the map below, sits mostly in Texas, but also crosses the border into New Mexico. It is the largest producer of the major tight oil regions, almost outproducing all of them collectively (chart right).

Source: U.S. Energy Information Administration

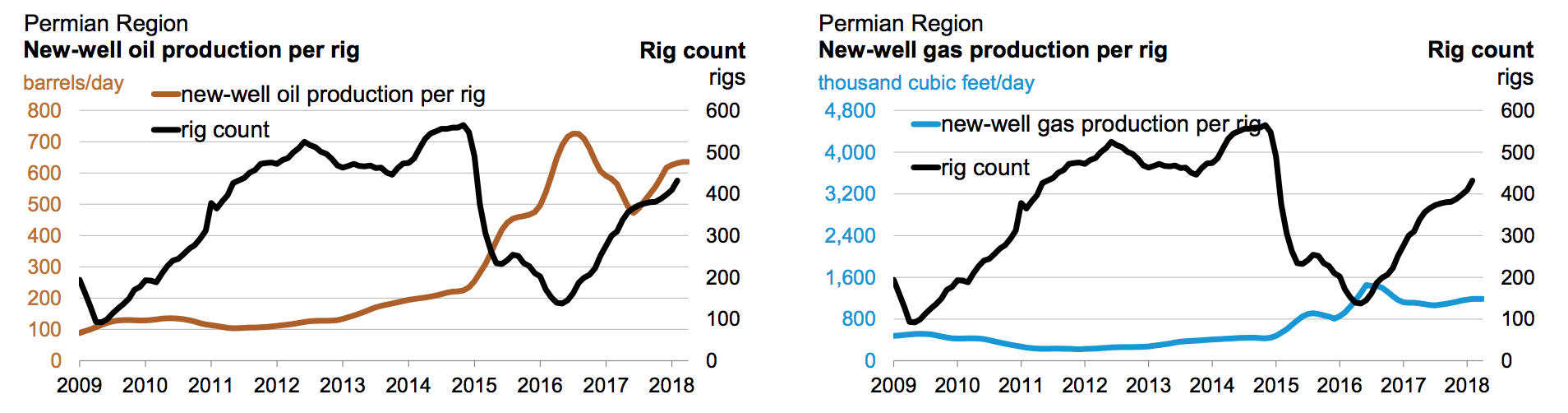

The Permian continues to see investment, with both the oil and gas rig counts rising (charts below, black lines). They have yet to recover to the level prior to OPEC’s price war and have plenty of room to grow.

Source: U.S. Energy Information Administration

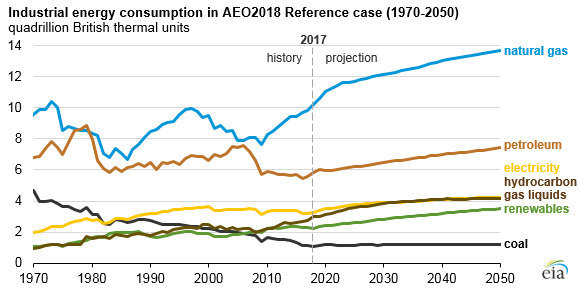

The Permian Basin is the second largest natural gas producer among the shale plays. Growing demand from U.S. industry should continue to aid growth in investment. The chart below illustrates how natural gas consumption has increased steadily since 2010, and is expected to grow for decades.

Source: U.S. Energy Information Administration

Also helping natural gas demand are power plants. According to the EIA, natural gas is now the top fuel, responsible for 32% of electricity generation, up from 24% in 2010. Coal generation back then generated 45% of electricity but is now only producing 30%.

The oil and gas production industry in the U.S. certainly looks set for strong growth. One of the interesting ways to play it is by investing in oilfield services. RPC, Inc. (NYSE: RES) is a services company with a strong position in the Permian Basin that derives a major chunk of its revenues from pressure pumping, i.e. hydraulic fracturing.

Profiting from Black Gold

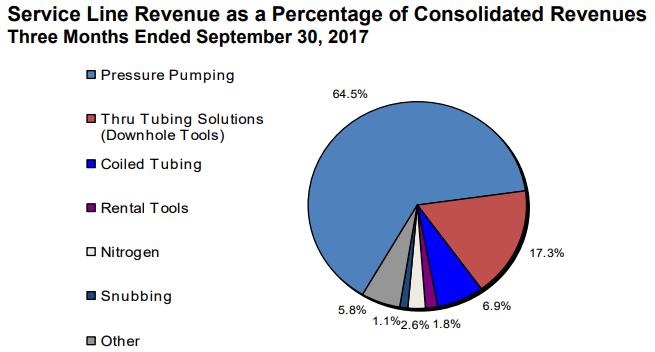

RPC is a holding company housing Cudd Energy Services, Thru Tubing Solutions, and Patterson Services. Its services center around shale oil production with a majority of its revenues generated by pressure pumping, i.e. fracking. While RPC has a strong presence in the all-important Permian Basin, it operates in all of the major shale oil fields.

Source: RPC, Inc.; Jefferies 2017 Energy Conference Presentation

With a capital structure that allowed it to make acquisitions during previous oil busts, the company understands the need for a long-term view. This conservative approach has positioned the firm well to handle booms and busts; carrying zero debt and not dependent on any single customer for more than 10% of sales.

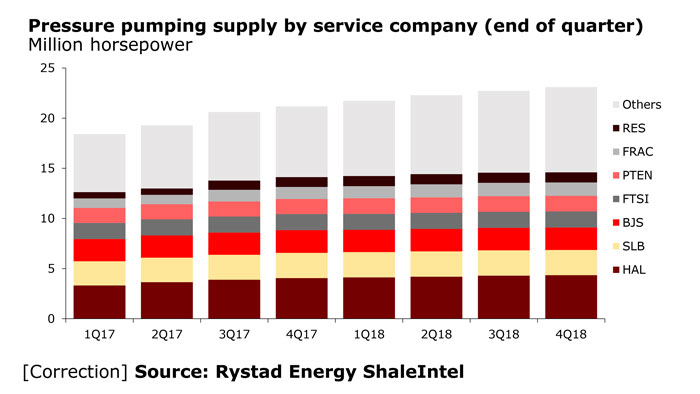

Its initial reaction to the current oil production recovery was to reactivate its mothballed pressure pumper fleet. It has since embarked on increasing the size of its fleet, ordering new trucks last year to be delivered in the next few months. These fracking fleets are measured in terms of horsepower. RPC is adding 127,000hp to its existing 925,000hp, bringing it up to about a quarter of Haliburton’s (NYSE: HAN) industry-leading output. Rystad Energy’s ShaleIntel lists RPC as having the seventh largest pressure pumper fleet.

Source: Rystad Energy’s ShaleIntel

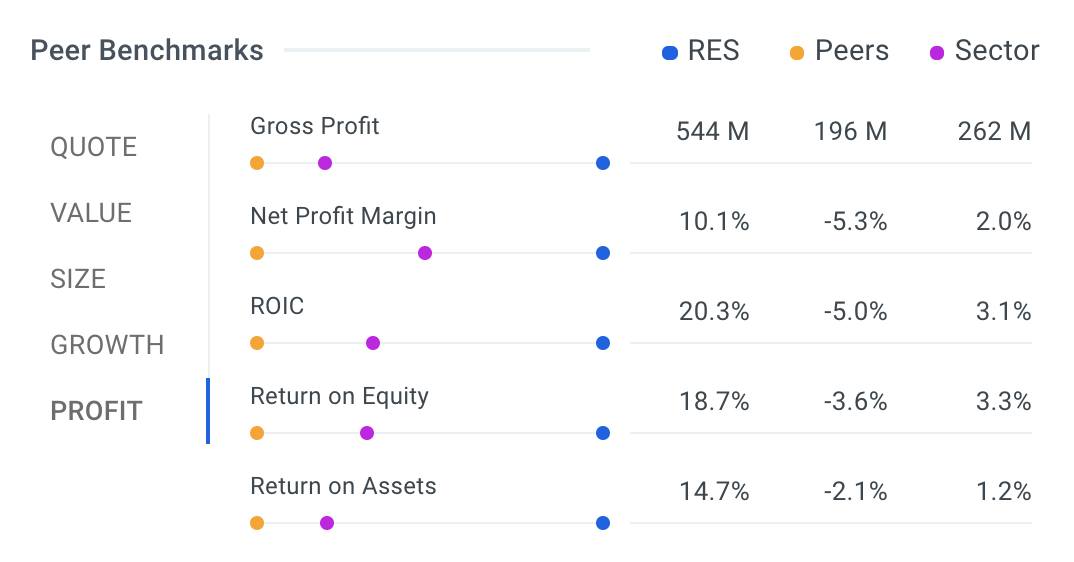

Management’s no-nonsense balance sheet (zero debt, $91 million in cash) allows it to both make investments and return money to shareholders. Despite their plans to double capex in 2018, the company expanded its share buyback program by 10 million and increased dividends. The dividend yield currently is 2.0% in an industry where few firms return cash.

The industry also does not have a lot of positive earnings. RPC has bested its peers and sector by a mile in profit benchmarks, and takes great pride in its Return on Invested Capital (ROIC).

Source: finbox.io

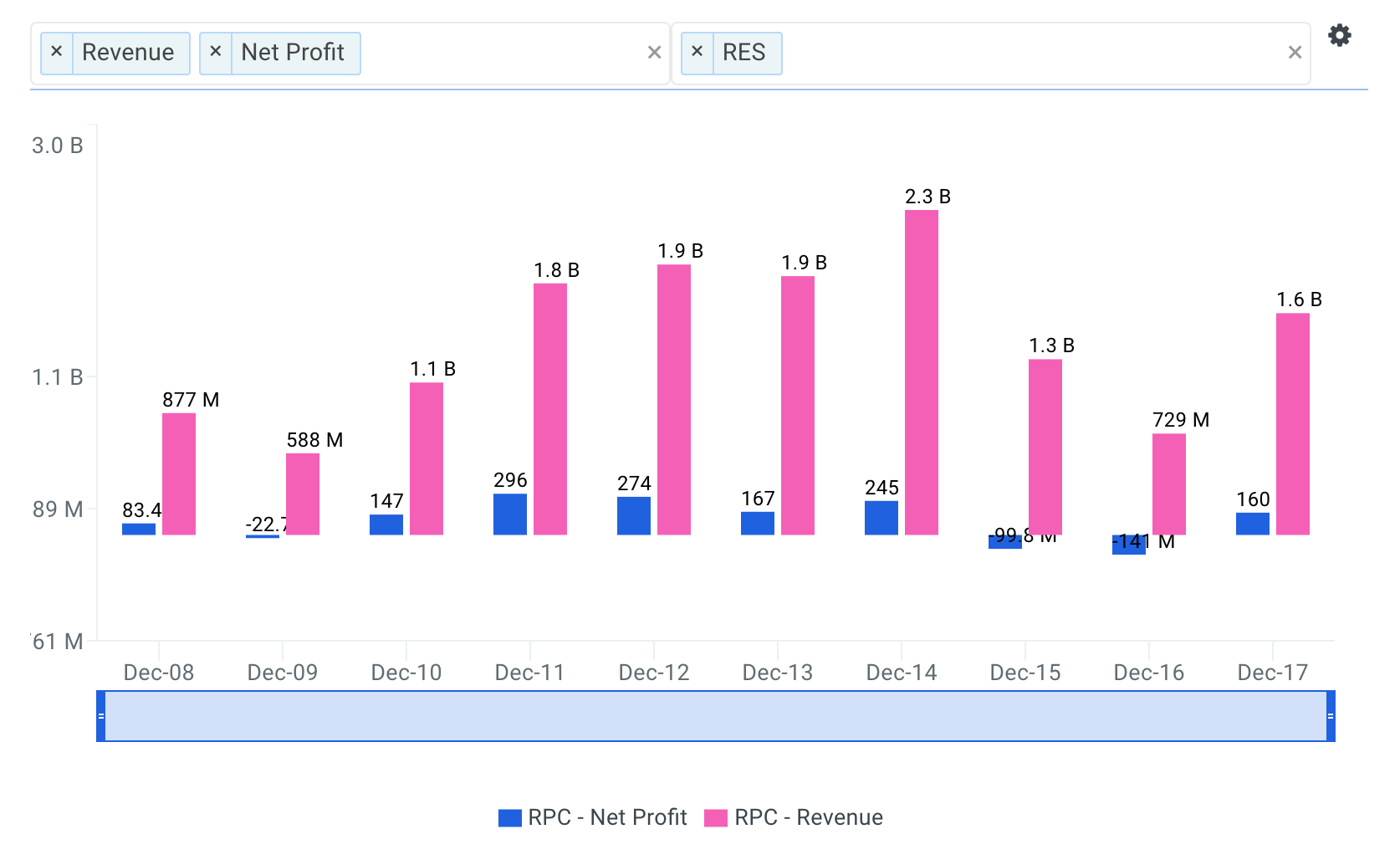

This is a volatile industry. RPC was able to survive the OPEC price war, but as shown below, profits can be elusive. The company returned to its winning ways in 2017, and Wall Street is forecasting 36.8% topline growth and 142% EPS growth in 2018.

Source: finbox.io

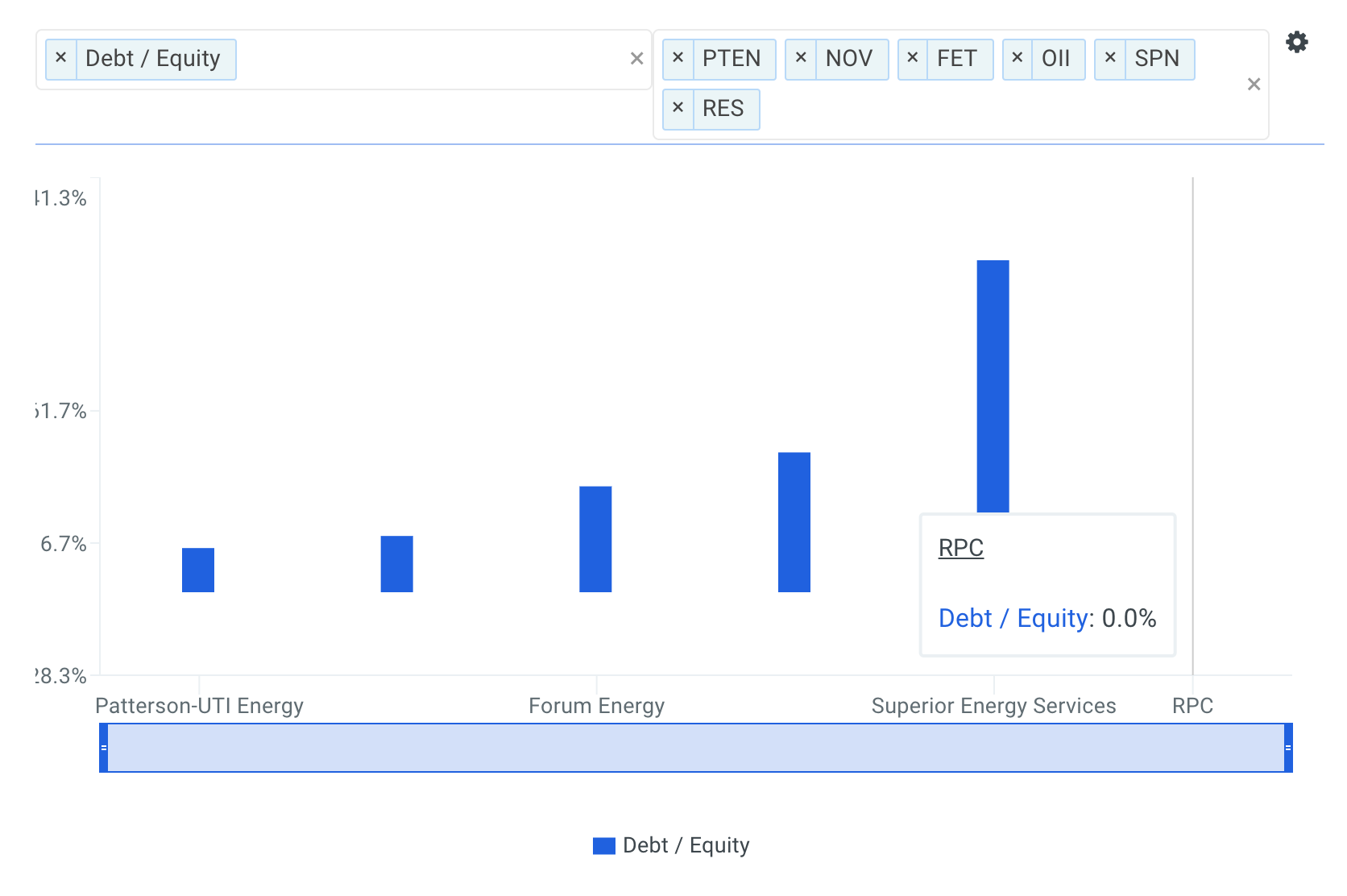

While RPC’s peers may lack positive earnings, one thing they do not lack is debt as illustrated in the chart below.

Source: finbox.io

RPC Primed to Pump Up 20% Gains

Another view of the stock’s potential is through the eyes of Wall Street experts. As noted earlier, analysts expect strong top and bottom line growth in 2018. They also forecast that the stock will appreciate by 22.5%. Confirming this upside is finbox.io’s fair value estimate. This quant-based model indicates room for the stock to increase by nearly 20%.

source: finbox.io

The U.S. oil and gas production industry is beginning to heat up. Record oil and gas production in 2018 coupled with strong growth projections create a great environment for oilfield service companies to invest and profit. RPC’s debt-free structure puts it in prime position to seize the day, and the expected doubling of capex this year shows that management is taking advantage. Overall, the firm’s recent financial performance, investment in growth, and support by Wall Street indicate the stock is ready to fly.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt is the lead reporter on Form 4 filings and general insider activity.

Matt Hogan is also a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

{kind=link}