Multiples Valuation: Revenue Multiples

How to Build a Revenue Multiples Comparable Company Analysis Model

A Multiples Valuation, also known as a Comparable Companies Analysis, determines the value of a subject company by benchmarking the subject's financial performance against similar public companies (Peer Group).

We can deduce if a company is undervalued or overvalued relative to its peers by comparing metrics like growth, profit margin, and valuation multiples. finbox.io offers pre-built Multiples Valuation models based on EBITDA, Revenue, and P/E. This guide will walk through the Revenue Multiples Valuation model.

A Revenue Multiple, also known as Enterprise Value to Revenue Multiple (EV/Revenue), measures the dollars in Enterprise Value for each dollar of revenue. To determine if a company is "expensive" it's far more useful to compare EV/Revenue multiples than the absolute stock price.

For example, let's assume Company A and Company B, are identical businesses that operate with no debt. You can purchase Company A stock for $5/share and Company B stock for $5,000/share. Company B trades at 1.0x EV/Revenue and Company A trades at 5.0x EV/Revenue. All else equal, Company B is "cheaper" than Company A since shareholder's receive a greater claim to earnings for each dollar invested.

The general formula behind a Revenue Multiples model is the following:

Enterprise Value = Revenue x Selected Multiple

Once we've estimated Enterprise Value, we can use an Equity Waterfall to get to a Fair Value per Share

Here is an outline of the process:

- Step 1: Select Comparable Companies

- Step 2: Select LTM Revenue Multiple

- Step 3: Select Forward Revenue Multiple

- Step 4: Conclude on a Fair Value Range

I've created an Illustrative Revenue Multiples model for Apple that you can use to follow along with this guide:

Google Spreadsheet of Multiples Valuation: Revenue

You can also build your own updated model on finbox.io here.

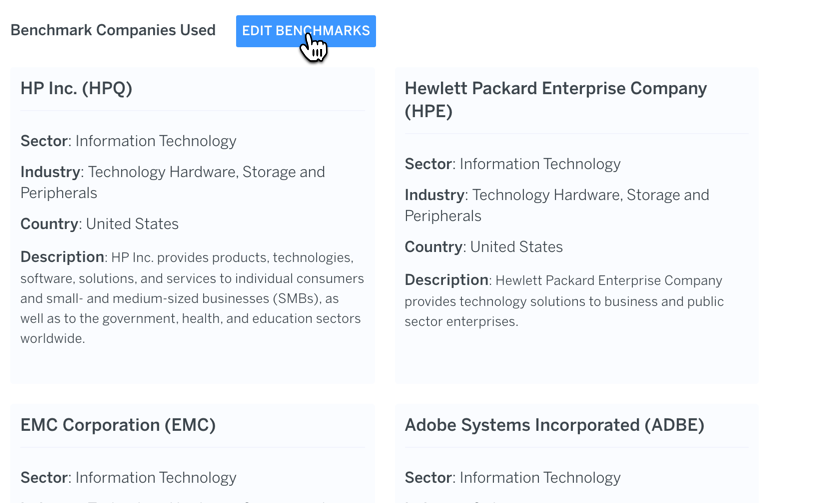

Select Comparable Companies

Selecting a good peer group is critical in a Multiples Valuation analysis. When defining the Peer Group, it's important to understand the key characteristics of a company's operations. Good comparable companies generally operate in similar industries and have similar business models and operating metrics.

finbox.io has algorithms that select the default peer group but you can use sources like SEC filings, news, research reports, and your industry knowledge to customize the peer group.

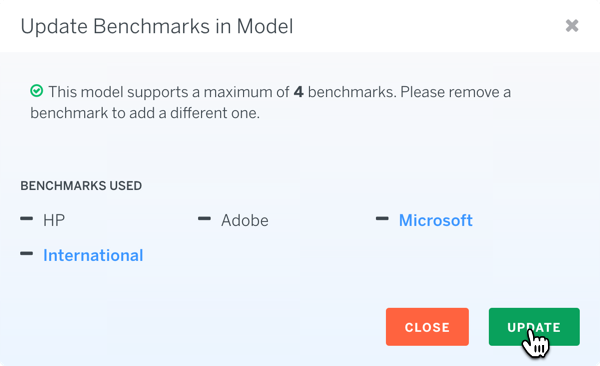

To edit the default benchmark companies used in the model:

- On the

BENCHMARKS EDITORtab, click the EDIT BENCHMARKS button

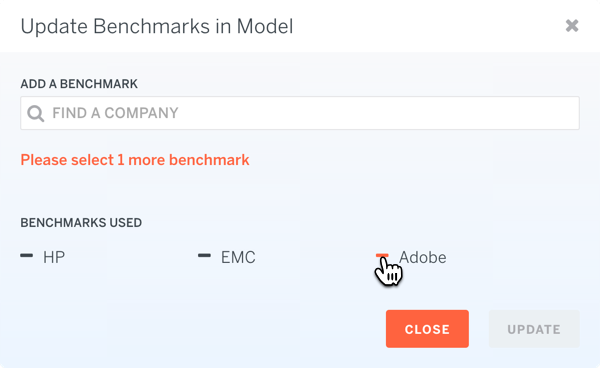

- Benchmarks are limited to 4 companies. You can remove an existing company by clicking the

--sign next to it. In my model, I wanted to replace Hewlett Packard and Adobe with Microsoft and IBM:

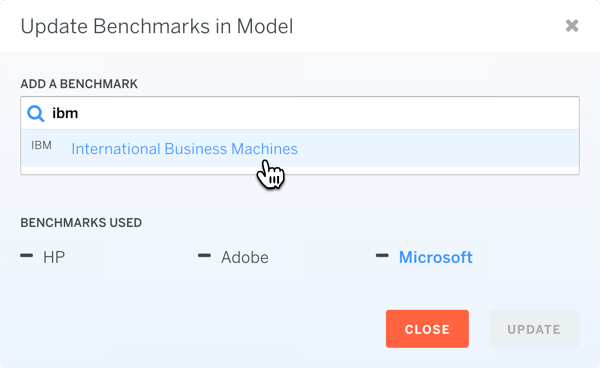

- Search for the company you would like to add:

- Once you hit Update, your model will update with data for your new benchmarks

Select LTM Revenue Multiple

The key question we're trying to answer in this step is the following -- are the differences in operating metrics like growth and margin in the peer group accurately reflected in the market EV/Revenue multiples?

To determine whether the subject company is being valued appropriately I like to first identify the "best" and the "worst" company in the peer group. Ranking the peer group from best to worst provides me with a range of valuation multiples that I can apply to the subject company.

Some questions worth exploring during this step:

- Which company has the best historical and projected growth profile?

- Which company has the best profit margins?

- Which company is the biggest?

- Which company has the best returns on invested capital?

If all else is equal, higher quality businesses deserve higher valuation multiples. Questions like these can help you discern how the subject company ranks against the peer group. Revenue multiples are highly correlated with profit margins so differences in EBITDA margin often explain differences in valuation.

The model has a table you can use to answer many of these questions:

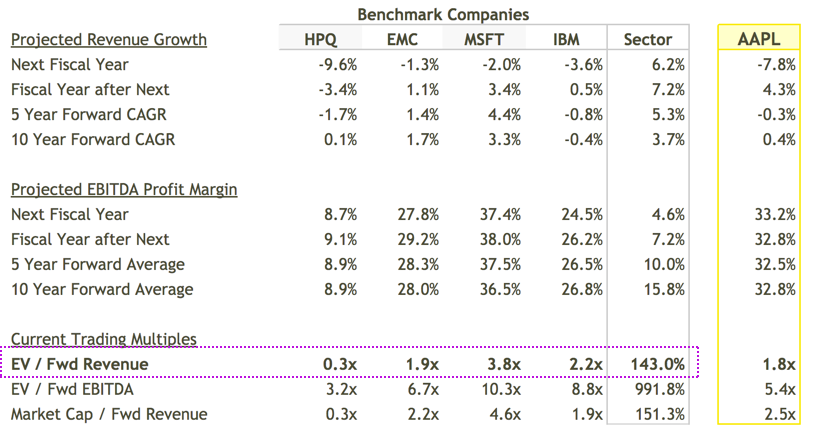

In the illustrative peer group (HPQ, EMC, MSFT, and IBM), HPQ has the lowest EBITDA profit margin and unsurprisingly trades at the lowest EV/Revenue multiple of 0.3x. Microsoft (MSFT) has the best EBITDA profit margin. MSFT trades at the highest EV/Revenue multiple of 4.0x.

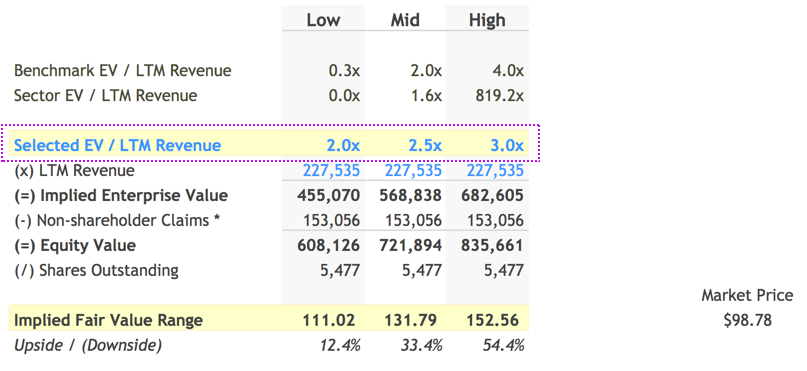

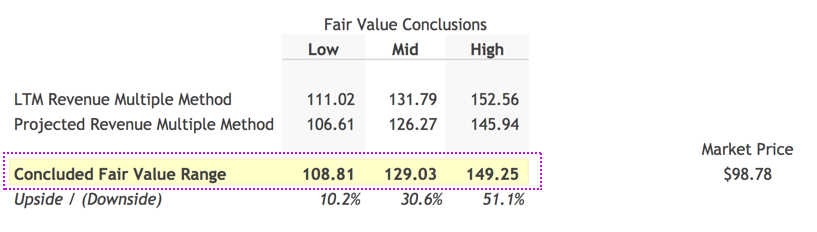

Given these data points, I decided to value Apple somewhere between 2.0x to 3.0x times LTM Revenue, near IBM on the low-end but below Microsoft on the high-end. When I input these selections into the model, it yield an implied per share range of $111.02 to $152.56, with a mid-point of $131.79.

Select Forward Revenue Multiple

You can follow the same thought process discussed in the previous step to select a multiple based on projected or Forward Revenue.

In the illustrative example, Microsoft (MSFT) has the best projected growth profile and profit margin outlook. Microsoft also commands the highest EV/Fwd Revenue multiple of 3.8x. Again, HPQ is at the bottom of the pack with EBITDA margins around 9% and a 0.3x EV/Fwd Revenue multiple.

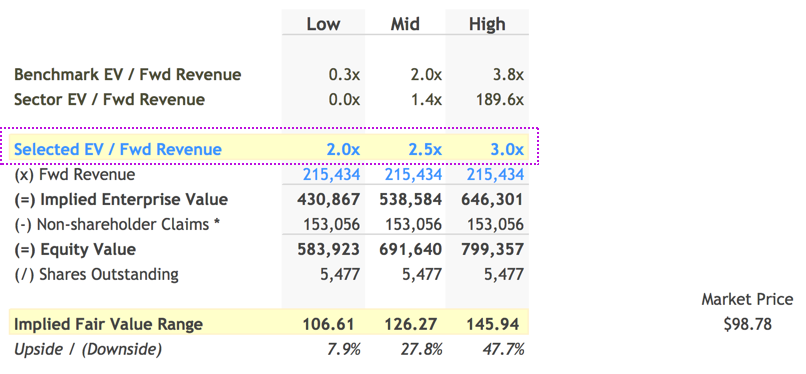

Considering these factors, I decided to value Apple between 2.0x to 3.0x Fwd EBITDA, above EMC on the low-end and below MSFT on the high-end. When I input my selections into the model, it yield an implied per share price range of $106.61 to $145.94, with a mid-point of $126.27.

Conclude on a Fair Value Range

Based on the range of fair values detemined using LTM and Forward Revenue, in this step you can input your concluded Fair Value Range and see how it compares to the current market price.

By default finbox.io uses a simple average of the two estimates. I felt equally confident in my LTM and Fwd Multiple selections so left the conclusion unchanged.

Apple appears to have a rich upside of +30% based on my EBITDA Multiples Valuation. Apple might be a stock worth digging into! finbox.io's Price Target and Alerts features are great for tracking such price targets and receiving alerts when there are big movements in stock price that present a potential entry point.

Next Steps

Multiples Valuation models are useful in getting a sense of an industry quickly. Has the industry experienced a downturn recently? Is it on the upswing? How optimistic are analysts on the industry's prospects? What range of valuation multiples does the market assign to companies in this space?

You can answer many of these questions with a quick glance at the numbers. Then with a few assumptions, you can determine if a company justifies further research. Pretty awesome! Since no one valuation approach is perfect, we recommend using a combination of models to get a sense for the risks involved and triangulate a fair value before making an investment.

{kind=link}