Oracle Corporation (NYSE:ORCL) is expected to report earnings on Thursday after the market closes. The company's shares last traded at $40.47 as of Monday, approximately 96% of its 52 week high. Finbox.io fair value data implies that the stock is currently 9% undervalued while Wall Street's consensus price target of $44.13 also implies 9% upside.

<img src='http://res.cloudinary.com/finbox/image/upload/v1481601254/ORCL_haywjg.jpg' alt= ‘ORCL finbox.io fair value estimate’>

Oracle's efficiency ratios look attractive when compared to its publicly traded peer group: salesforce.com, inc. (NYSE:CRM), Red Hat, Inc. (NYSE:RHT), Microsoft Corporation (NasdaqGS:MSFT) and VMware, Inc. (NYSE:VMW). The company's return on equity (ROE) of 19% is above the group average of 14%. Similarly, return on assets (ROA) and return on invested capital (ROIC) are also above the group average. Microsoft is the only peer that has outperformed Oracle in all three categories.

<img src='http://res.cloudinary.com/finbox/image/upload/v1481601253/ORCL_Efficiency_Ratios_pop2zt.jpg' alt= ‘ORCL efficiency ratios’>

However, Oracle's net income and EBITDA growth rates have generally underperformed relative to the same comparable company group.

<img src='http://res.cloudinary.com/finbox/image/upload/v1481601253/ORCL_Growth_phrxzc.jpg' alt= ‘ORCL Net Income and EBITDA growth chart’>

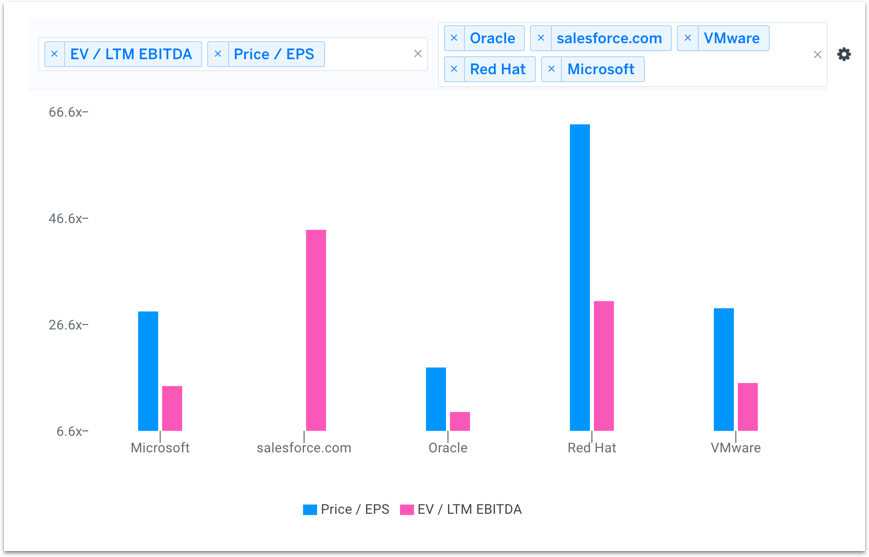

These growth figures help explain why the company's price to earnings (P/E) and EBITDA multiples trade at a significant discount.

<img src='http://res.cloudinary.com/finbox/image/upload/v1481601255/ORCL_Multiples_qawvu6.jpg' alt= ‘ORCL pe and EBITDA multiples’>

Should Oracle be trading at such a steep discount? They are facing stiff competition as they shift into cloud computing (currently 8% of revenues), but the company is still a clear leader in the database space. Overall, Oracle remains an attractive long-term investment boasting industry leading returns and a favorable balance sheet. Value investors may want to take a closer look at the stock prior to earnings. Both Wall Street and finbox.io valuation models support a fair value close to $44 per share.

{kind=link}

{kind=link}

{kind=link}

{kind=link}