Oracle (ORCL) is facing stiff competition as it shifts into cloud computing (currently 8% of revenues), but the company is still a clear leader in the database space. Overall, Oracle remains an attractive long-term investment boasting industry leading margins and a favorable balance sheet.

<img src='http://res.cloudinary.com/finbox/image/upload/e_shadow:40,q_100/v1473895987/ORCL_DCF_Fair_Value_cwwa5o.jpg' alt= ‘ORCL DCF Summary’>

Full model

My discounted cash flow (DCF) analysis results in a fair value of approximately $46.50 per share which implies a 15% margin of safety. This does not signal huge upside but investors long the stock should feel comfortable going into Thursday’s expected earnings report.

Calculating Oracle’s fair value...

Projecting Free Cash Flows

Finbox.io uses analyst forecasts for revenue and EBITDA as the starting assumptions in a DCF model. I typically review the analyst forecast and modify the growth rates based on historical performance, news, and other insights.

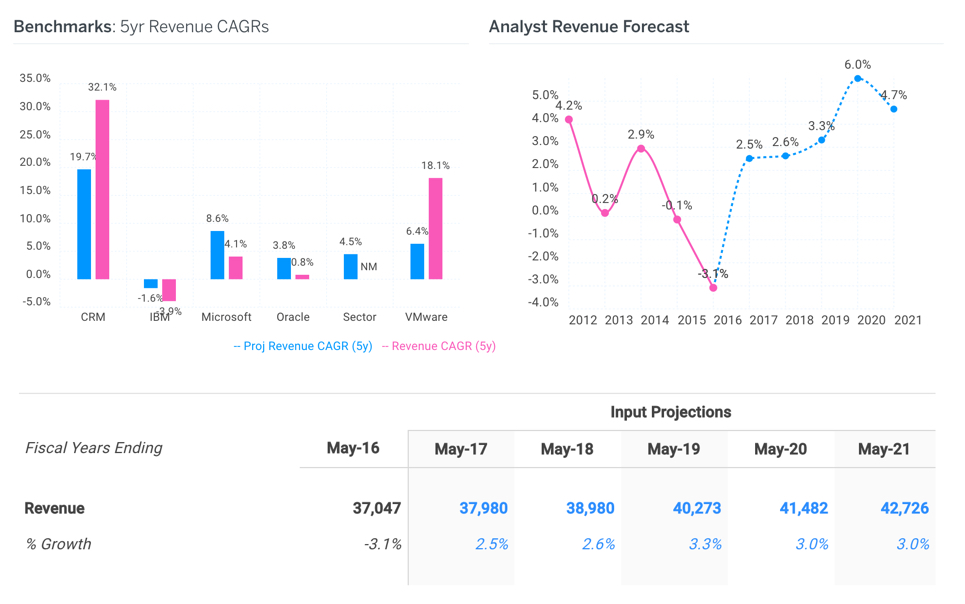

Oracle’s historical and projected revenue compared to peers: salesforce (CRM), IBM (IBM), Microsoft (MSFT) and VMware (VMW) is shown below.

<img src='http://res.cloudinary.com/finbox/image/upload/v1473896046/Revenue_Forecast_xpbgbf.jpg' alt= ‘Oracle Revenue Forecast’>

Fiscal year 2020 and 2021 figures appear aggressive so I lowered revenue growth rates to 3% for the final two years.

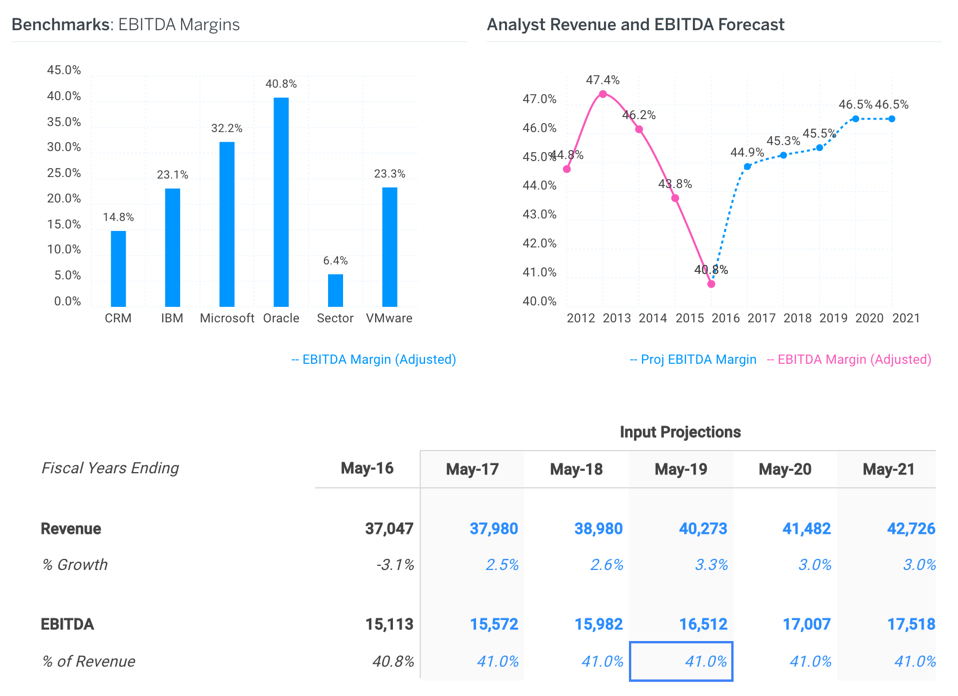

The analyst EBITDA margin forecast for Oracle also looks aggressive. I have little faith in their projections while margins continue to trend lower amidst competitive pricing pressure. I selected a flat 41% EBITDA margin for the entire 5 year forecast - below Oracle's historical average but still well above the comparable companies.

<img src='http://res.cloudinary.com/finbox/image/upload/v1473896003/EBITDA_Forecast_xoeepi.jpg' alt= ‘Oracle EBITDA Forecast’>

Terminal Value

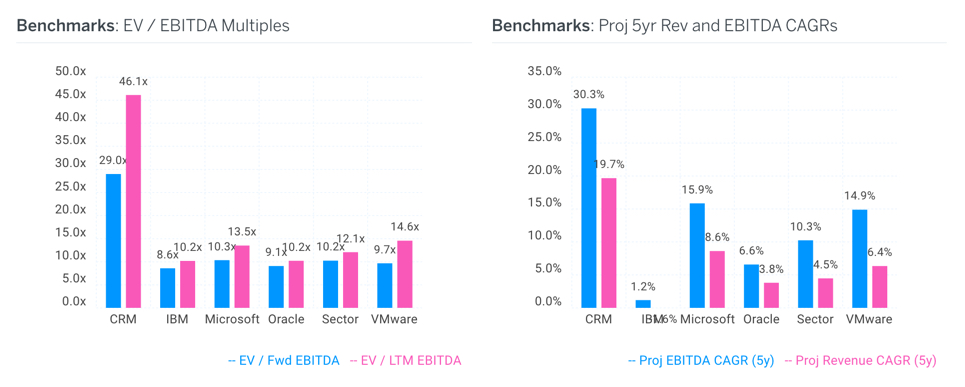

An EBITDA exit multiple is applied to calculate Oracle’s terminal value at the end of the 5 year forecast. Outside of Salesforce, the peer group’s EBITDA multiples trade in a fairly tight range.

<img src='http://res.cloudinary.com/finbox/image/upload/v1473895994/TV_-_EBITDA_Mults_wvra1k.jpg' alt= ‘Oracle Peer Group EBITDA Multiples Analysis’>

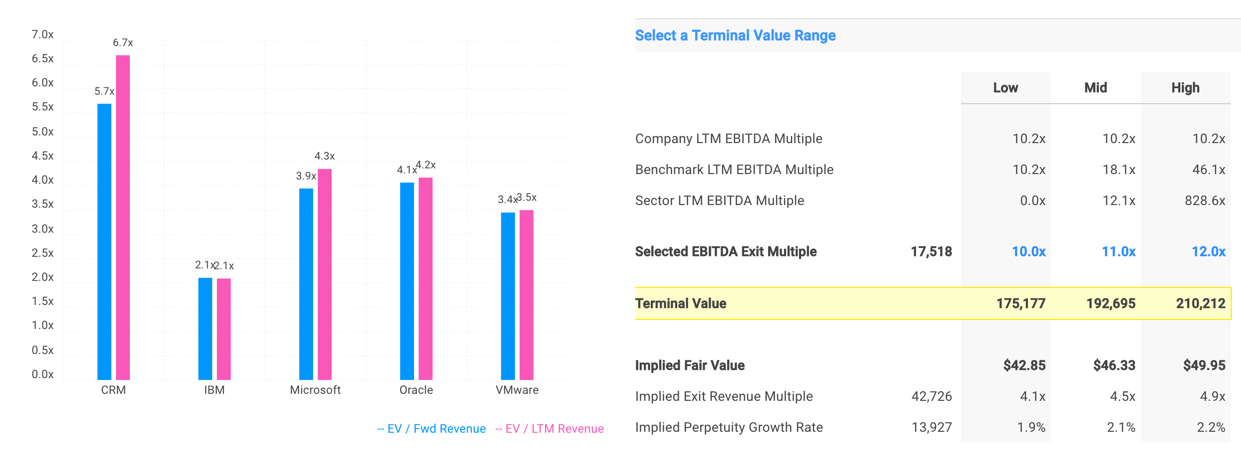

I’ve selected an EBITDA exit multiple of 11.0x at the midpoint which is generally in line with the peer group. Notice Oracle’s implied revenue exit multiple of 4.5x at the midpoint which is slightly above Microsoft’s current 4.3x multiple. This helped me get comfortable with my 11.0x selection since Oracle should be trading at a higher revenue multiple due to its superior profit margins.

<img src='http://res.cloudinary.com/finbox/image/upload/v1473895984/Terminal_Value_uaip7c.jpg' alt= ‘Oracle Terminal Value’>

The DCF analysis above results in a fair value of approximately $46.50 per share implying a 15% margin of safety. Again, this is not huge upside but investors long the stock should feel comfortable given the conservative adjustments made to the forecast. Value investors may even want to pick up shares on an earnings miss.

Get Started Now!

Article written by Matt Hogan.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}