While earnings season is coming to a close, there’s still some notable companies expected to report earnings this week including Home Depot (HD), Wal-Mart Stores (WMT), Intuit (INTU), and Cisco Systems (CSCO).

Using finbox.io’s fair value estimate data, which provides a quick sanity check on a company’s fundamental value, I screened companies expected to report earnings this week (11/13 - 11/17) to find stocks that may be trading off their intrinsic value prior to earnings. The results showed that Cisco was one of the most undervalued of these companies.

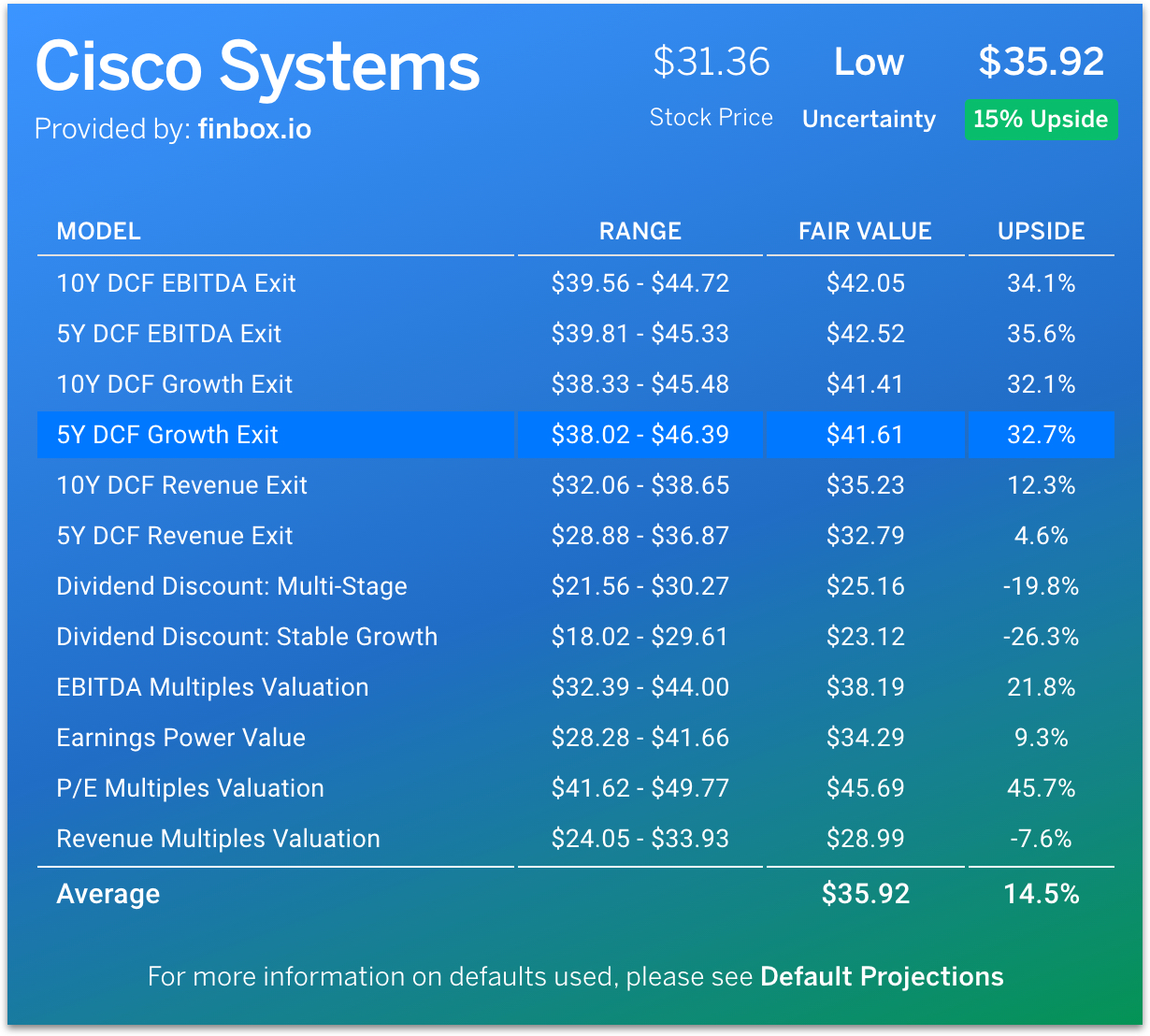

Cisco’s fair value estimate:

<img width="75%" src='http://res.cloudinary.com/finbox/image/upload/v1479141626/CSCO_Fair_Value_aummte.jpg' alt= Cisco Finbox.io Fair Value’>

The fair value estimate above implies that Cisco is currently 15% undervalued. However, notice how the discounted cash flow (DCF) models show even more upside which is the real story here.

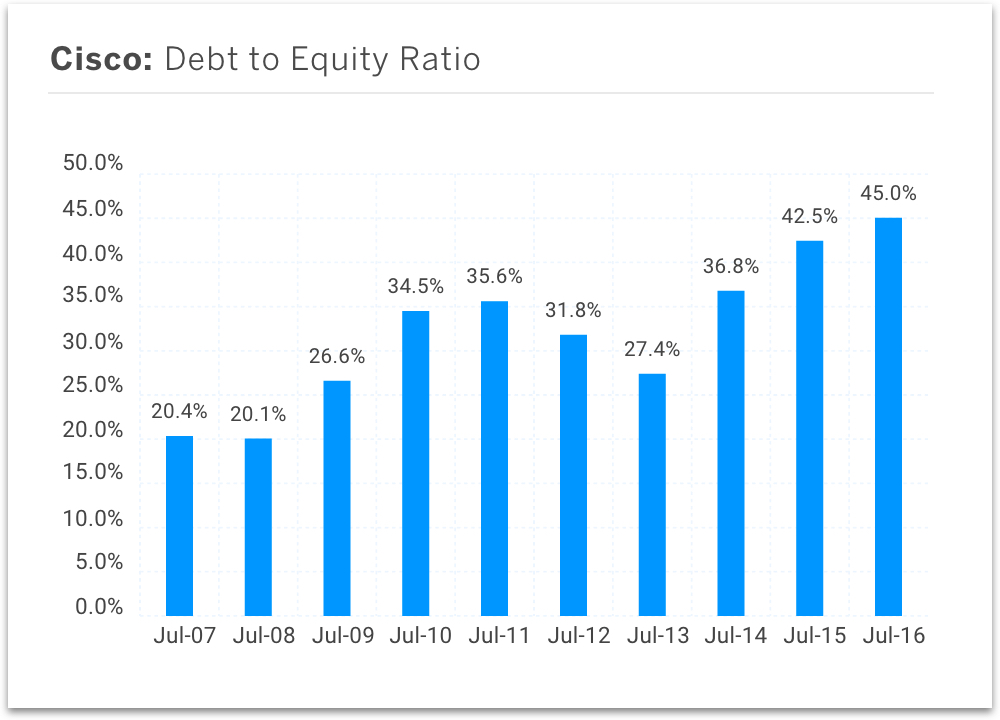

Using multiple valuation methodologies can help triangulate a stock’s fair value but some may be more relevant for a given company. Understanding leverage trends will help determine which valuation approach should be more heavily relied upon. Take Cisco for example:

<img width="75%" src='http://res.cloudinary.com/finbox/image/upload/v1479141606/CSCO_Debt_to_Equity_xln7oq.jpg' alt= Cisco Debt to Equity Ratio Chart’>

Over the last ten years, Cisco’s debt to equity ratio has steadily increased from 20% to 45%. Because of this leverage fluctuation, a DCF analysis is the most reliable valuation approach. The main reason for this is because projecting debt payments becomes too difficult. Additional detail on this can be found here.

<img width="100%" src='http://res.cloudinary.com/finbox/image/upload/v1479141625/CSCO_DCF_mkdue5.jpg' alt= Cisco Finbox.io DCF Analysis’>

View full DCF analysis here.

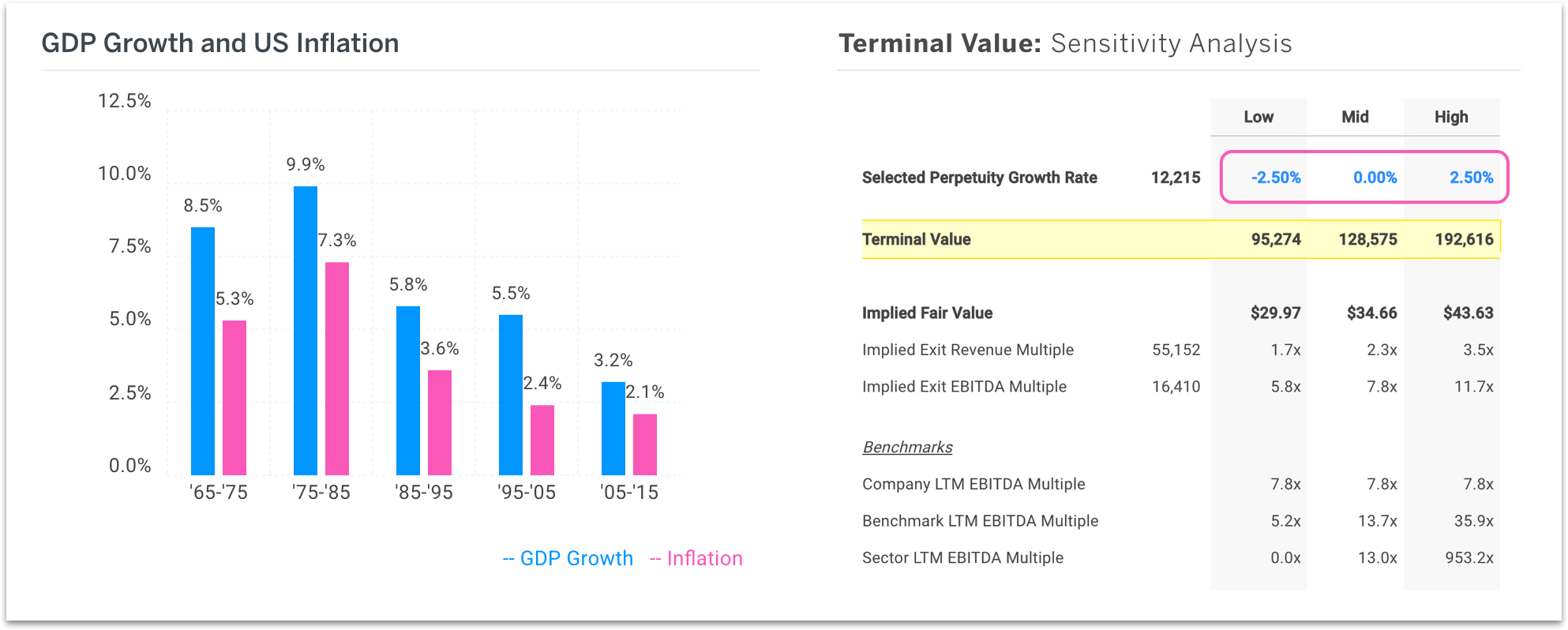

The DCF analysis above concludes that Cisco has over 30% upside when using consensus Wall Street projections for the 5-year forecast period. The valuation model then applies a 2.5% perpetuity growth rate after the 5-year forecast to calculate a terminal value.

Further analysis of this growth rate offers additional insight on how the market seems to be severely discounting Cisco.

<img src='http://res.cloudinary.com/finbox/image/upload/v1479141620/Terminal_Value_Support_rlb3ur.jpg' alt= Cisco Terminal Value Support’>

The perpetuity growth rate used in such analysis is typically between the historical inflation rate of 2-3% and the historical GDP growth rate of 4-5%. However, inputting a negative (2.5%) growth rate results in a fair value of approximately $30 per share; not too far off Cisco’s current trading price. This implies that the market is actually expecting Cisco’s cash flows to decline forever. A negative growth rate seems unreasonable especially when comparing the company’s positive 5.6% EBITDA CAGR over the last 5 years.

While Cisco does face stiff competition from smaller players like Arista Networks (ANET), it is still the world’s largest supplier of high-performance computer networking systems. It is unlikely the company becomes irrelevant over the next several years which is why value investors may want to take a closer look at CSCO prior to reporting earnings Wednesday. Shares could easily trade close to $40 over the next 6-12 months.

{kind=link}

{kind=link}

{kind=link}