Following the Smart Money

One often discussed investment strategy among investors is following the so-called “smart money.” This strategy involves coat-tailing large, institutional investors such as hedge funds, pension funds and mutual funds into their investments.

The basis for the strategy is that these larger investors have superior resources and expertise to identify attractive investments and there are several studies supporting this notion. Shares that have gained the largest institutional ownership have outperformed the market, at least in the short-term.

So where is the smart money investing today? The Wall Street Journal recently profiled an area of the market that these investors are targeting and it appears to be a contrarian bet. Retail stocks have underperformed year-to-date, with the SPDR S&P Retail ETF (NYSEArca: XRT) off 5% while the S&P 500 is up 11%. However, institutional investors have begun increasing their stakes in such battered names as Nordstrom Inc. (NYSE: JWN) and Macy’s (NYSE: M).

While retail valuations may be depressed, picking stocks with relatively more resilience to e-commerce may provide additional protection. Footwear is thought to be better protected from online shopping than other goods, given customers’ propensity to try on shoes before purchasing.

With athletic footwear and apparel retailer Foot Locker, Inc. (NYSE: FL) set to announce earnings later this month (expected August 17th), let’s take a closer look at the company and assess the stock’s attractiveness relative to its current trading levels.

Nike’s New Amazon Partnership

Foot Locker is a leading retailer of athletic shoes and apparel, operating over 3,300 stores in 23 countries. The company’s stores include footwear and apparel retailers Lady Foot Locker, Kids Foot Locker, Footaction and Champs Sports.

Store sales contribute 87% of all revenue, with the balance coming from its direct-to-customer segment, which includes FootLocker.com and Eastbay, Inc. The company derives its revenue primarily from footwear, with 82% of sales coming from the category.

The biggest, recent development for Foot Locker has been Nike’s (NYSE: NKE) decision to partner with Amazon, Inc. (NasdaqGS: AMZN) to begin selling products directly on the retailer’s website. Investors did not take the news well, with Foot Locker shares immediately selling off 5%.

Source: finbox.io

The new partnership shouldn’t be taken lightly, as Nike products and shoes including the Jordan, LeBron, KD, and Air Max represent 68% of Foot Locker’s overall sales. Any significant shift of sales towards Amazon could cause a material change in Foot Locker’s results. However, there are a few dynamics that investors may not be considering:

Product Segmentation Incentives

Nike’s footwear business is heavily launch-driven, and the company may be more dependent on sales through brick-and-mortar than Foot Locker bears expect. Much like Apple, Inc.'s (NasdaqGS: AAPL) iPhone fanatics, sneaker aficionados tend to spend hours in line outside of stores anticipating new releases. Nike often under supplies these releases to further stoke demand and create additional pricing power.

While no distributor represents over 10% of Nike's revenue, it seems likely the company will want to protect this fanatic customer base, even if just for the must-have optics. This may lead Nike to save its biggest launches for its brick-and-mortar distribution channels while offering more mainstream lines through Amazon.

In addition, a significant portion of Foot Locker’s sales is received in cash, a unique characteristic of its customer base and perhaps providing some protection from the e-commerce threat. Foot Locker also offers Nike valuable consumer insights into regional buying tendencies.

This complex relationship with one of their leading retail partners may cause Nike to segment its product lines, at least in the near-term. Ultimately, the Amazon partnership may provide less of a negative impact on Foot Locker’s results than bearish investors anticipate.

History of Market Overreacting to Amazon

Amazon continues to throw its weight around, with recent headlines including its acquisition of Whole Foods (NasdaqGS: WFM), launching a competing service to Best Buy’s (NYSE: BBY) Geek Squad, and Sears Holdings announcing it would sell Kenmore appliances on Amazon.

Related stocks such as Kroger (NYSE: KR), Home Depot (NYSE: HD) and Lowe’s (NYSE: LOW) all fell on the news. However, investors appear to have overreacted as all three stocks have pushed higher since the initial sell-offs.

If these stocks are any indication of what’s to come, Foot Locker could see a similar near-term rebound.

Foot Locker Valuation: 60% Upside

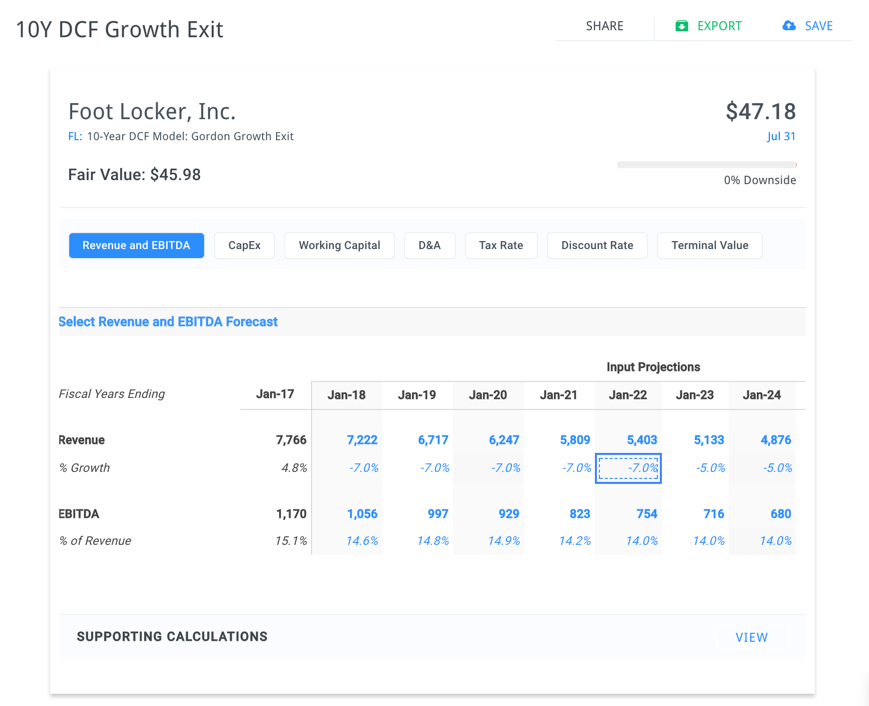

What does Foot Locker’s current stock price say about market expectations? At $46.02 per share, the market is painting a pretty bleak picture. Wall Street analysts project low-to-mid-single digit revenue growth with a modest EBITDA margin contraction over the medium-term. Given that Foot Locker has grown revenues at a mid-to-high single-digit clip over the past five years, these assumptions seem fairly reasonable.

Employing these assumptions across eleven of finbox.io’s valuation models generate an average fair value estimate of $76.96, implying over 60% upside to the stock.

To arrive at the market’s current share price, one needs to assume -7% growth each year for the next 5 years, a drastic drop-off. This suggests that investors may be overreacting to Nike's Amazon partnership.

Source: finbox.io DCF model

Wall Street’s consensus one-year target is a bit lower at $68.95 but still represents nearly 50% upside. Foot Locker shares also offer additional return with its current 2.6% dividend yield.

Trading near its 52-week low and showing significant short interest with 8.43% of the float short, the smallest bit of good news for Foot Locker may create a surge in demand for the stock and a corresponding jump in share price.

Conclusion: Another Amazon Overreaction

The smart money has been showing its contrarian side, opening positions in retail stocks battered by negative sentiment. Investors looking to follow the smart money may wish to focus on footwear, a business generally considered to be more resilient against e-commerce. Foot Locker, with 82% of its revenues from athletic footwear, certainly fits the bill.

A recent partnership between Nike and Amazon has cast doubt on Foot Locker’s prospects and its stock has taken a hit. However, a closer look at Foot Locker’s business shows incentives for Nike to be cautious with the relationship going forward. Nike has a launch-heavy business model and places great value on the regional buying preferences it receives from Foot Locker’s customers. These factors will likely lead Nike to segment its products across its distribution channels.

Note this is not a buy or sell recommendation on any company mentioned.

Photo Credit: LinkedIn

{kind=link}