- Recreational vehicle market is smashing records driven by strong demographic tailwinds.

- Thor's strategic acquisition of Jayco expanded its product offering and provided additional manufacturing capabilities.

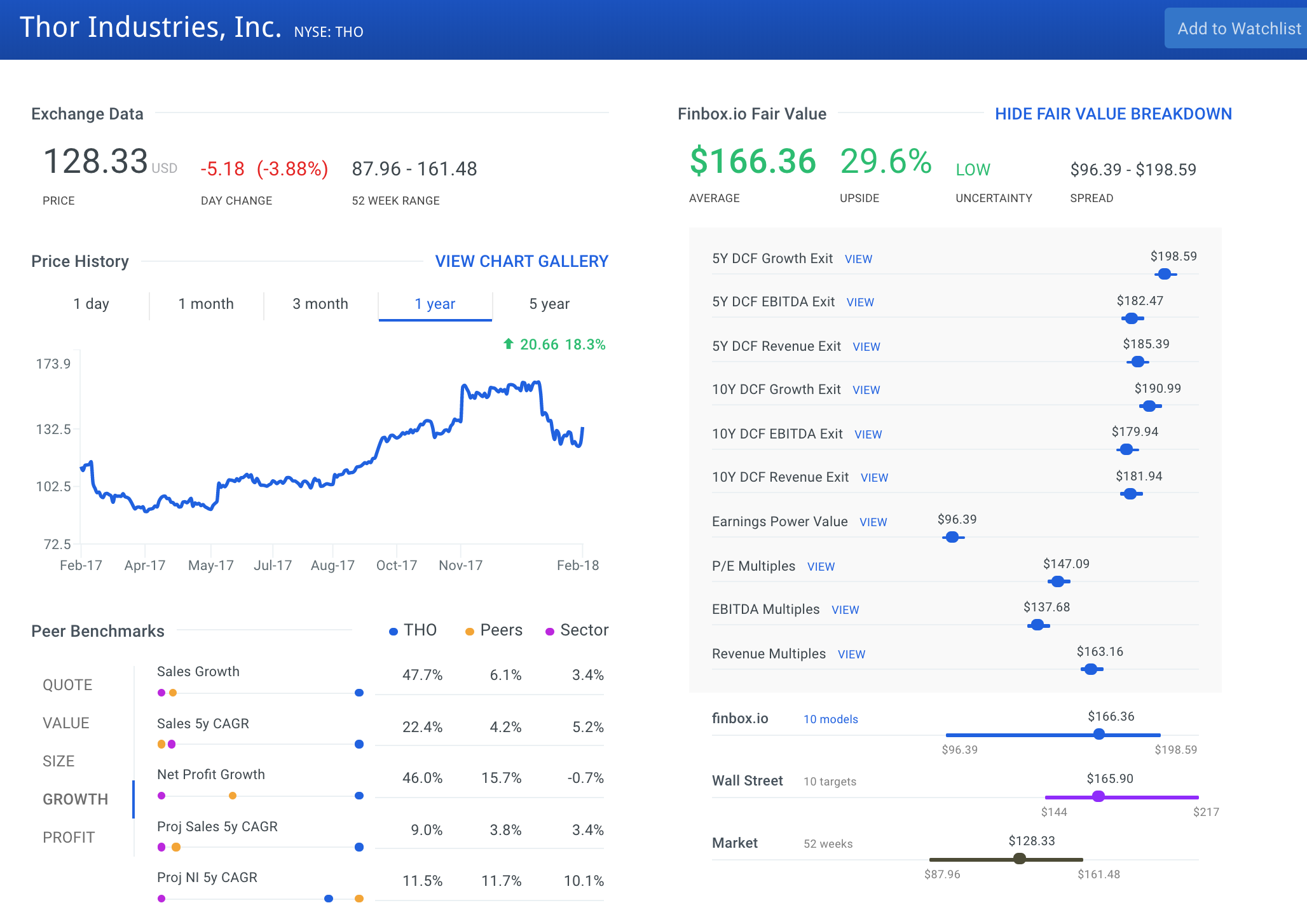

- Wall Street analysts and market multiples relative to peers point to the stock being significantly undervalued.

Strong Recreational Vehicle Growth

The recreational vehicle (RV) industry, which is comprised of towable trailers and motorized vehicles, has seen strong growth since the last recession. The number of RVs shipped grew by double digits in 2016 and 2017 (15.1% and 17.2%, respectively) according to the industry’s trade group RVIA. As Forbes recently noted, RV sales are being driven by the two largest U.S. population groups: “Experience-craving millennials, joined by retiring baby boomers are helping fuel an unprecedented boom in sales.”

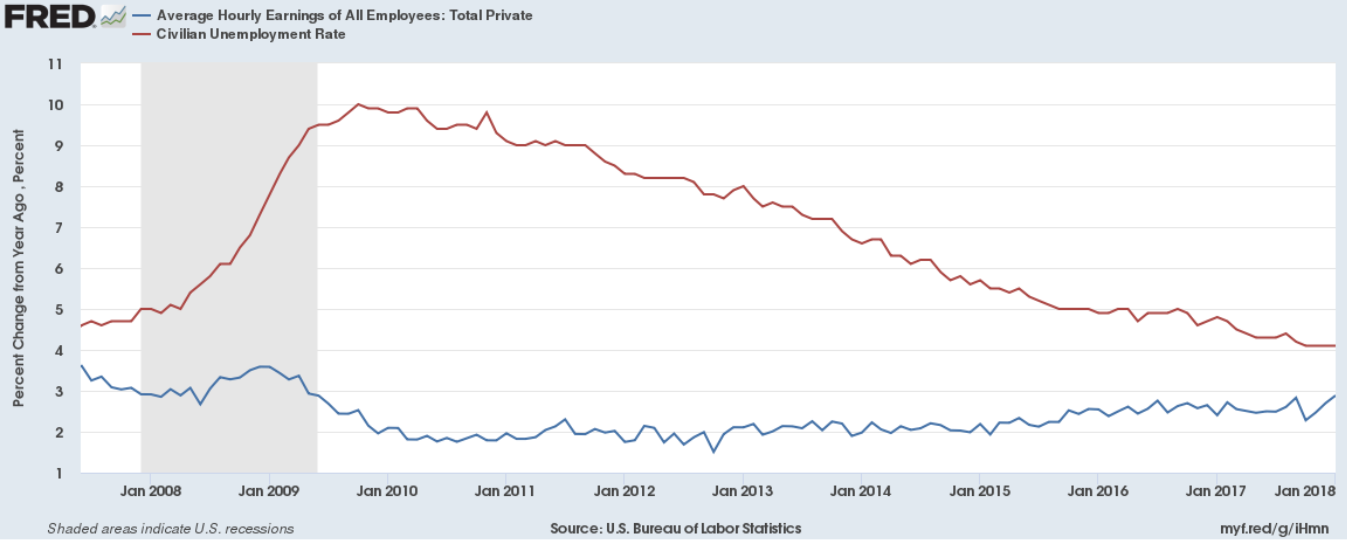

The industry will continue to enjoy strong tailwinds as demographics collide with a nine-year-old economic expansion. Thanks to record-setting financial markets, baby boomers have seen their portfolios recover, and Millennials are enjoying a strong job market with wage growth (chart, blue line). The red line shows that unemployment has fallen to near 4%.

Source: US Bureau of Labor Statistics

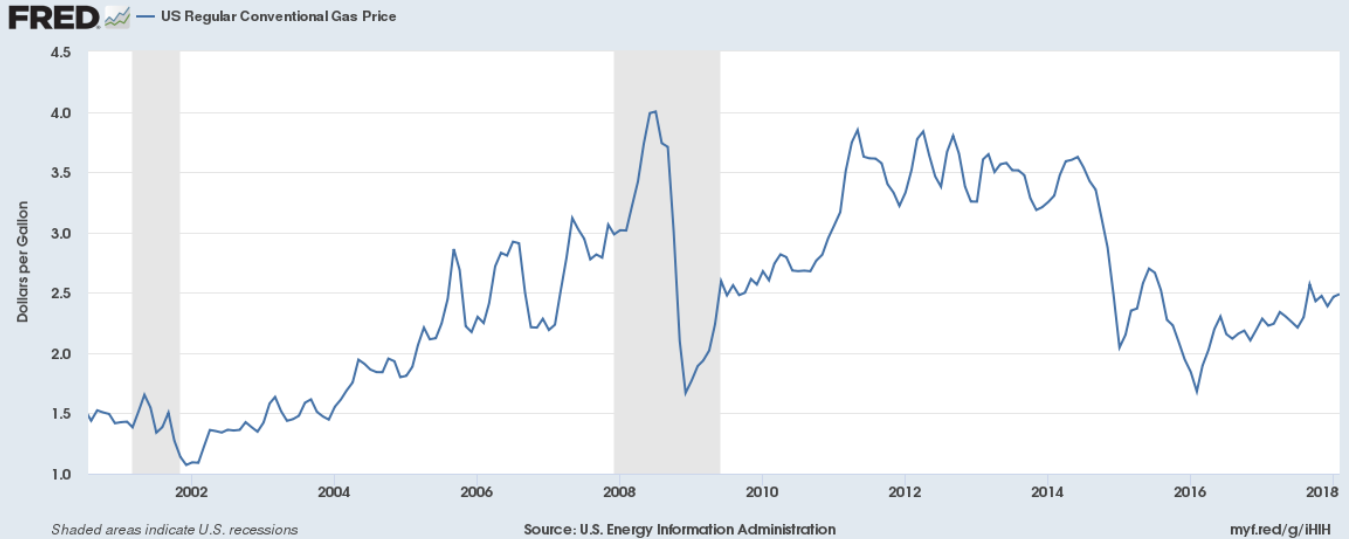

Stable, low gas prices (chart below) have also helped drive the motorized RV segment. This has also led to more pickups and SUVs on the road which can tow the majority of trailers, especially as manufacturers have focused on making lighter units. Forbes reported, “that auto sales have rapidly flipped to about 60 percent-40 percent SUVs and pickup trucks over sedans, from the reverse percentage just a few years ago.” This means that first-time buyers are likely already set to tow their new camper home.

Source: US Energy Information Administration

Low-interest rates and credit availability have also helped fuel the growth. However, one tax sweetener that buyers had enjoyed was mangled in the recent tax reform. Most RVs can be counted as a second home, allowing for the deduction of mortgage interest. In their haste, Congress passed a tax bill that specified that only motorized RVs would be eligible, thus leaving the larger towable trailer market out in the cold. Industry trade group RVIA hopes to clean up the language in a maintenance bill this year, but all signs indicate that this process will drag for some time.

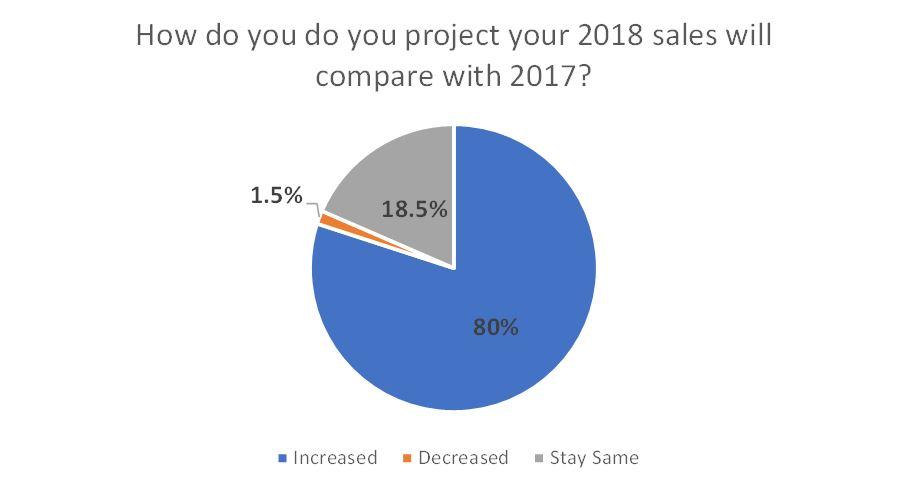

The expectation for continued record industry growth is also confirmed at the dealer level. A November 2017 survey by RV PRO magazine indicates that 80% of dealer respondents expect 2018 sales to beat an already great 2017.

Source: RV PRO Magazine

Catering to both Baby Boomers and Millennials can be daunting. The broad economic stratification of the RV buyer, in general, has always been a challenge as the market demanded everything from a simple, light overnight trailer to an Italian marble clad million-dollar bus. The ability to penetrate and profit from these varied price segments with well-known brands has driven consolidation, and Thor Industries (THO) has become the largest RV manufacturer in the world via strategic acquisition.

Thor Industries Investment Case

The recent market correction knocked 20% off the stock, putting Thor in prime position for an entry point purchase. The company’s broad product line, superior margins, low fixed cost structure, and investment in expansion should reward investors that want to profit from the growth in the RV industry.

Source: finbox.io

Thor comes with a 37-year pedigree and has never had an unprofitable year. It operates 18 subsidiaries covering every nook and cranny of the industry and allows these entities to operate independently and entrepreneurially. In 2016, it purchased Jayco, the 3rd largest RV manufacturer, adding four additional respected brands to its lineup. Maybe more important in this economic climate, the acquisition provided additional manufacturing capacity.

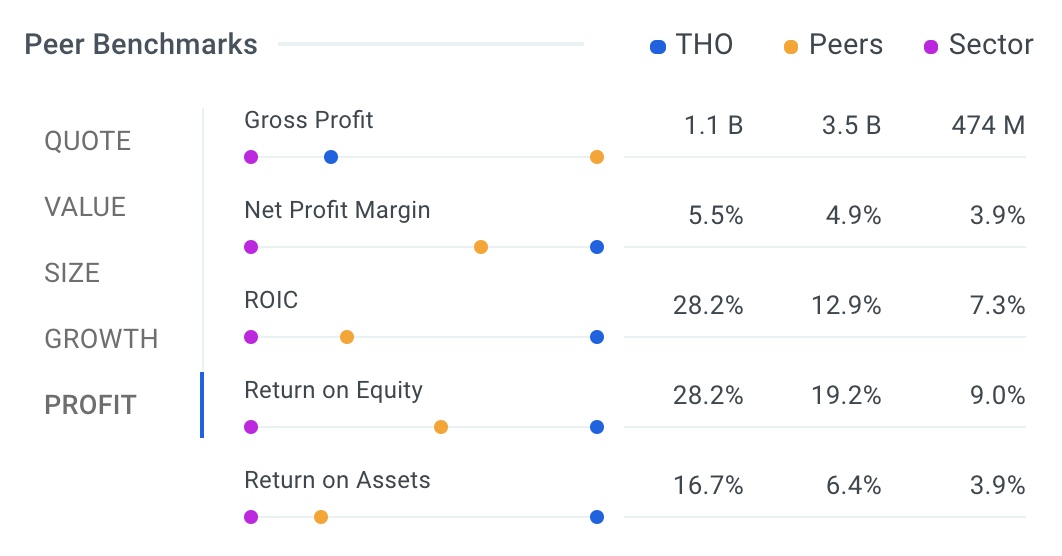

The peer benchmark section of finbox.io’s dashboard highlights Thor’s superior execution metrics with high net profit margins, ROIC, ROE, and ROA.

Source: finbox.io

As a cyclical consumer company should, Thor’s management touts its low fixed cost structure. This gives companies financial flexibility during the bad times when a clean balance sheet is necessary. Thor’s debt to equity ratio is by far the lowest of its direct peers.

Source: finbox.io

Industry growth can be both a boon and a cross to bear. Results from last quarter indicate both record growth (revenues and net income) and a record level of backlog (up 70% to $3.7 billion) which are orders the company has yet to deliver. To help with capacity constraints, the company is investing in organic growth opportunities such as a $40 million expansion of Airstream’s facilities in Ohio. Overall, Thor invested $115 million during its fiscal 2017 on property, plant and equipment, and expects to deploy $185 million 2018

Thor’s Valuation Looks Attractive

Based on Tuesday’s price of $128.33, both market analysts and finbox.io’s impartial quant composite see upside of nearly 30%. Wall Street professionals clearly embrace management’s approach and recognize the industry’s growth potential.

Source: finbox.io

Despite its success and price appreciation over the last year, Thor still sports the lowest P/E and Price/Sales multiples among direct competitors. Sales multiples are always a great comparative metric as it is not as engineered as earnings can be. However, the company’s P/E of 15.5x is surprisingly low with the DJIA at 26.9x and S&P 500 at 25.5x. Relative to the market and its peers, Thor looks undervalued based on market multiples.

Source: finbox.io

Thor is expected to report earnings on March 7th. The company has had 10%+ positive EPS surprises over the last three quarters, partially driven by impressive growth and also because management does not provide guidance. Analysts are predicting a 47% y/y jump in EPS, which presents a high hurdle.

Thor Industries Conclusion: Shares Picking Up Speed

Thor’s broad product line has put it in place to serve the needs of a diverse group of buyers. Furthermore, with an expanding economy, tax cuts, wage growth, loose credit, and retiring Baby Boomers, the company is set to extend its record sales and profit figures. Investment in expansion remains the key to executing and the company’s financial discipline provides the flexibility to grow strategically, rather than react tactically.

Wall Street analysts and finbox.io’s model-driven target price both predict big upside while market multiples also point to the stock being undervalued. Thor shares appear to have room to pick up speed moving forward.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

%20Stock%2030%25%20Undervalued%3F){kind=link}