Interested in discovering the intrinsic value of a stock? Do you use the same Excel model for every company you analyze? Many analysts find it difficult when choosing the correct valuation methodology or are biased towards one specific approach. This is often a mistake which can negatively impact investment decisions and result in trading losses or missed opportunities!

While more than one valuation approach is often appropriate, the best equity research analysts understand that some are better than others when analyzing a given company. No two companies are the same and every business consists of unique characteristics that may require you to adjust your analysis. In this article, I’ll provide simple steps that will help you figure out which valuation method is most appropriate for any company you want to analyze. Note that these are the general recommendations of valuation expert Aswath Damodaran. Here’s what we'll cover:

- How to select the right valuation model (e.g. DCF, DDM or RI model)

- How to determine the appropriate forecast period (e.g. 10-yr / 5-yr / stable growth)

- Apply what we’ve learned to figure out the best valuation approach for Apple (AAPL).

Note that comparable company valuation models (relative approach) are not specifically mentioned in this article because should always be used.

1. Choosing the Right Valuation Model######

*Is leverage expected to change or stay the same over time?* Understanding leverage trends is the first step when determining the best valuation model for a specific company.An unlevered Discounted Cash Flow (DCF) model is most appropriate when leverage or debt is expected to fluctuate over time. The reason for this is because projecting debt payments is difficult and requires numerous assumptions. Therefore, debt payments as well as interest expense is excluded when projecting unlevered free cash flows. In addition, the discount rate (WACC) should not change dramatically over the projection period.

But what about when a company's leverage doesn’t fluctuate or is expected to remain stable over time? Then, an equity valuation model will likely be more accurate and the better valuation technique. The reason for this is because when leverage is stable, interest expense on debt can be projected with more reliability.

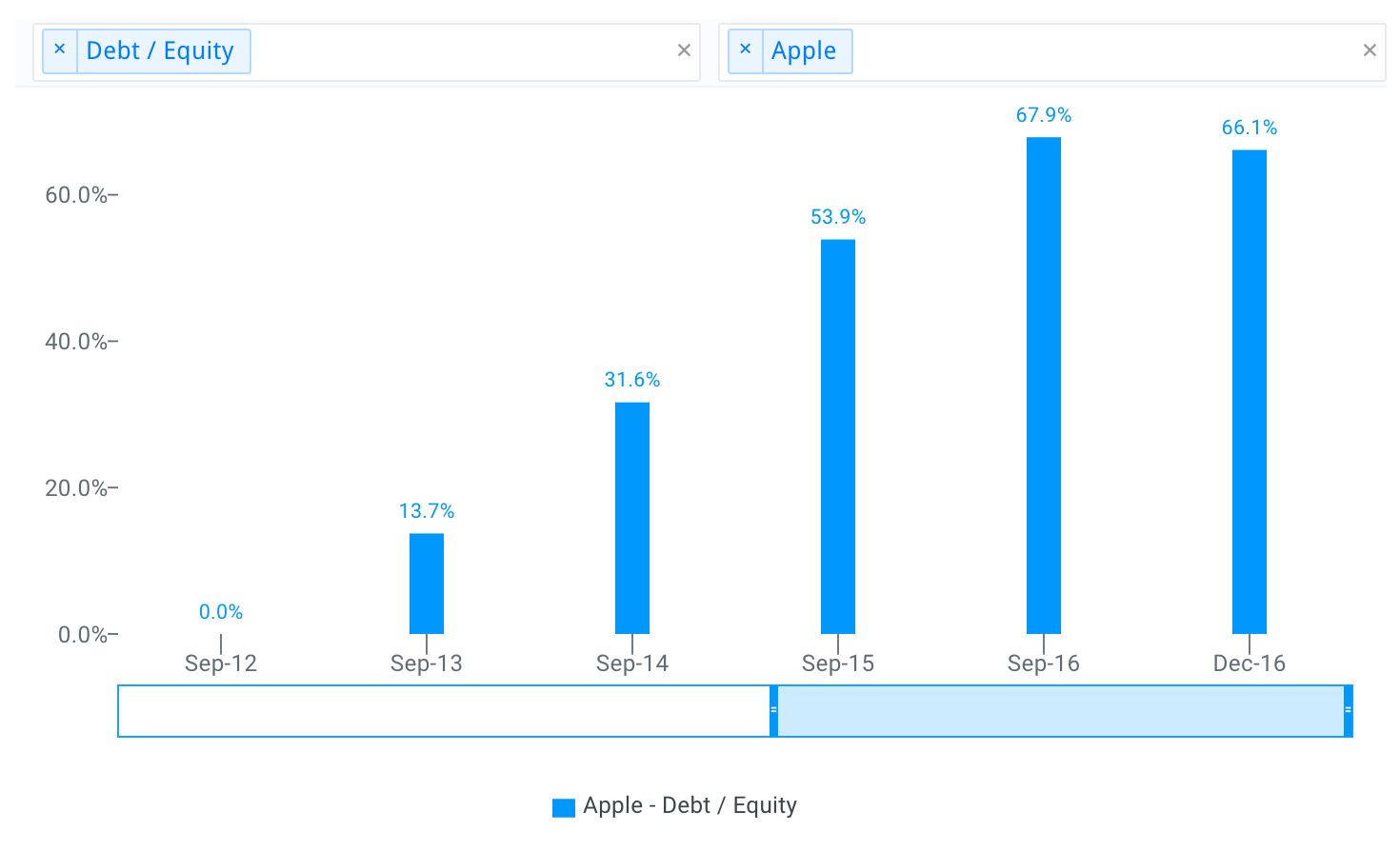

So how do we check if a company's leverage has been fluctuating or is expected to do so? This isn't always straight forward but checking debt ratio trends over the last three to five years can be a good indicator. For example, take a look at Apple's debt to equity ratio over the last five years in the chart below:

The graph above helps illustrate how Apple went from having no debt in 2012 to having over $50 billion of debt by fiscal year 2015. Leverage seems to have fluctuated considerably leading to the conclusion that a DCF model is likely the best valuation approach for Apple. However, lets assume Apple's leverage wasn't as volatile leading to the question of which equity valuation model should be used?

- Dividend Discount Model (DDM) or

- Residual Income (RI) or

- Levered DCF (also known as an Equity DCF)

Does the company pay dividends?

Understanding dividend payment trends is the first step when determining the best equity valuation model.

A DDM is most appropriate when a company's paid dividends are equal to or close to levered free cash flow over an extended period of time. It’s best to value a company’s stock price by projecting dividends when the company continues to pay the majority of its cash flows in the form of dividends. A payout ratio between 80% and 110% is a good indicator you should be applying the DDM technique. When outside this range, a levered DCF or RI model should be used.

2. Choosing the Appropriate Forecast Period######

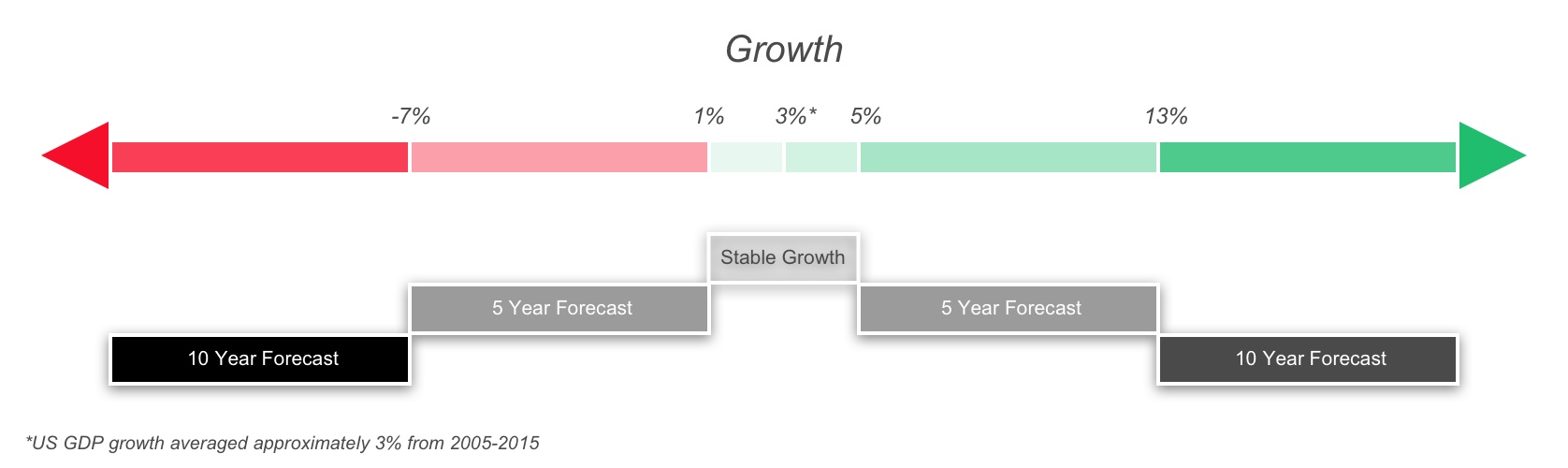

Figuring out the best projection period length typically depends on whether a company is in a stable, moderate or high growth phase. The best way to determine this is by comparing a company’s recent growth trends to the growth of the economy in which it operates (US GDP is often used as a benchmark). The graphic below provides guidelines on selecting the best forecast period based on growth indicators.

Stable Growth - A stable growth rate is fitting for a mature company that has consistently grown within 2% of the overall economy. Stable growth is also frequently referred to as the Gordon Growth approach.

5 year Forecast Period - A five year projection period is best for a company that is growing or declining at a moderate rate.

10 year Forecast Period - A ten year projection period should be used for a company that is growing or declining at a high rate.

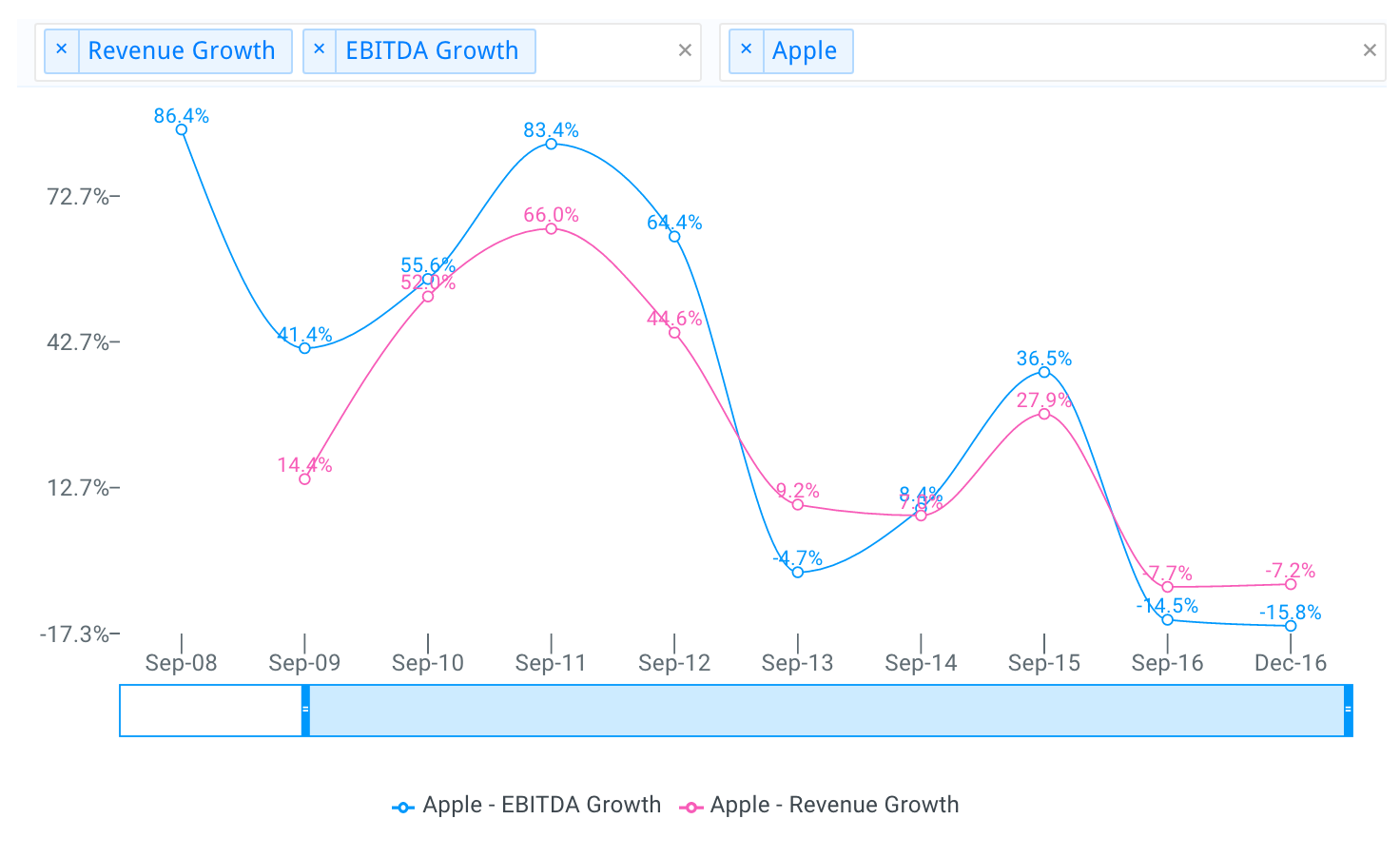

Now what projection period is best for Apple?

The chart above shows that Apple has recently experienced moderate as well as high growth phases. Therefor, a five or ten year forecast is reasonable.

3. Choosing the Best Stock Valuation Method for Apple######

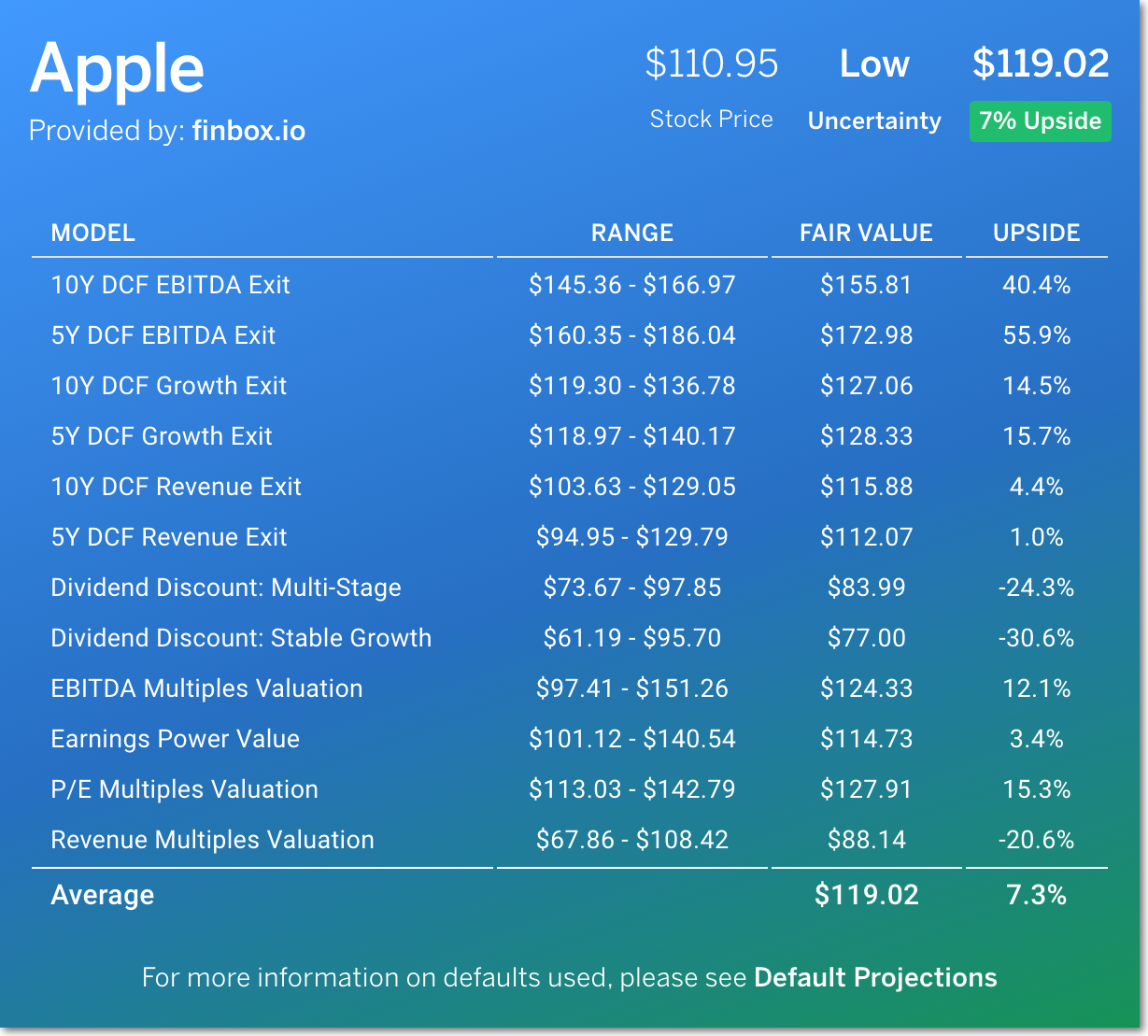

Based on the guidelines outlined above, a five or ten year unlevered DCF analysis appears to be the best valuation method for Apple. However, it’s important to note that it’s wise to use multiple valuation approaches to help triangulate a fair value conclusion. For example, notice Apple's fair value estimate below provided by finbox.io which applies 12 unique valuation models.

Discovering the fair value for a company can sometimes be difficult. Choosing the most appropriate valuation methodologies shouldn’t be. Stick to the suggestions above and start making smarter investment decisions that will likely result in higher stock returns.

{kind=link}