- Charlie Munger and Warren Buffett have long put a premium on businesses that benefit from pricing power.

- Sweet baked goods leader Hostess Brands Inc (NASDAQ: TWNK) portfolio of popular brands commands an 81% price premium over peers.

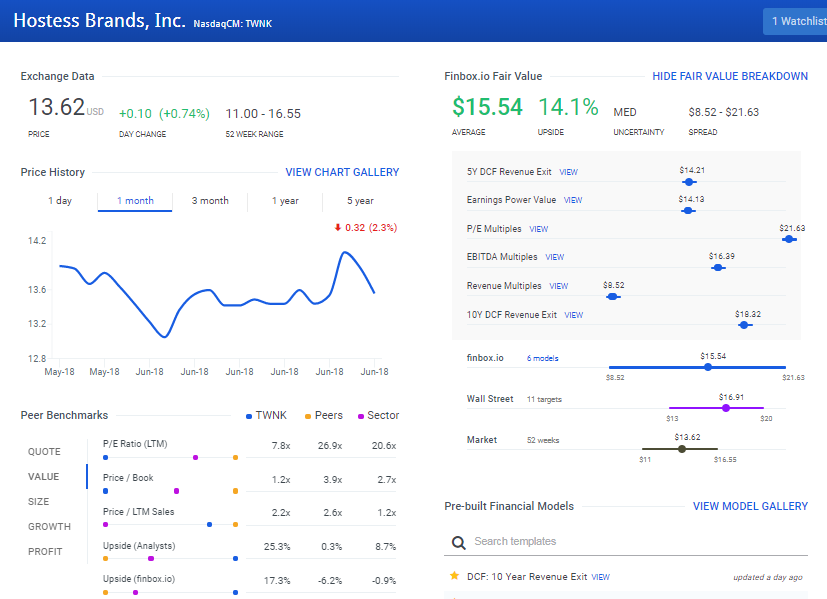

- With finbox.io valuation models showing nearly 20% upside, Hostess Brands offers the rare combination of quality assets at a value price.

Prioritizing Pricing Power

In Charlie Munger’s 1994 commencement speech to students at the University of Southern California, Munger touched on the rarity of businesses that benefit from superior pricing power:

“There are actually businesses that you will find a few times in a lifetime where any manager could raise the return enormously just by raising prices.”

While these types of businesses are rare, Munger’s investing partner Warren Buffett also prioritizes the ability to raise prices:

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business.”

Buffett reiterated the importance of pricing power as an indicator of extraordinary businesses:

> “The extraordinary business does not require good management.”

Perhaps a surprising comment to some, but it underscores Buffett’s belief in the value of pricing power. And for companies that benefit from pricing power but have a few question marks at management, Buffett’s comments should ease investor concern.

There may be no better example of such a company than Hostess Brands, Inc. (NASDAQ: TWNK). The producer of a plethora of beloved sweet baked goods recently transitioned to new management and benefits from superior pricing power (more on that below). What’s more, finbox.io valuation models show nearly 20% upside to recent trading levels. As such, let’s look at TWNK’s business model, recent results, and management’s strategic initiatives.

Hostess Brands’ Business Model

Hostess Brands is a leading developer, manufacturer, and marketer of fresh, sweet baked goods in the United States. The company has two reportable segments: “Sweet Baked Goods” ($733.8M in 2017 net revenue representing >90%) and “In-Store Bakery” ($42.4M). Within the Sweet Baked Goods (SBG) market category, Hostess is the second leading brand by market share and holds the leading market position within SBG’s two largest segments: Donut and Snack Cake.

Hostess’s portfolio of popular brands include Twinkies, Donettes, Ding Dongs, Suzy Qs, Fruit Pies, and Ho Hos. Customers include supermarkets, mass merchandisers, distributors, convenience, and drug and dollar stores. In 2017, Wal-Mart and affiliates represented 20.4% of net revenue.

Latest Quarter Results, a Pricing Power Advantage, and Management Initiatives

First Quarter Results

Hostess Brands’ net revenue increased 13.1% (5.2% excluding its Cloverhill acquisition) in its fiscal 2018 first quarter ending March 31. Gains were attributed to continued momentum from product innovations. TWNK’s top 7 brands, representing 69% of net revenue, showed point-of-sale growth of 8.5%. Adjusted EBITDA came in at $47 million compared to $54.5 million in the first quarter of 2017. Negative gross profit from the Chicago bakery and increased transportation costs drove the decline. Adjusted EPS was $0.14 ($0.15 in 2017) while cash flow and CapEx stood at $38.3 and $9.2 million respectively.

Pricing Power Premium

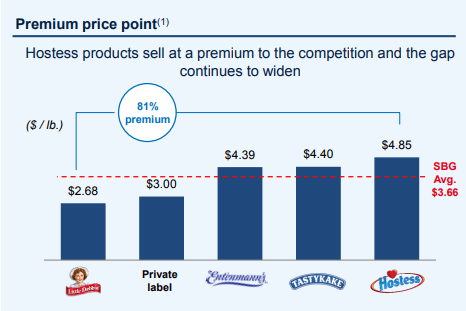

Within SBG, 60% of retail sales come from the category’s top three brands and private label has a limited presence (3.5%). Strong brand names, such as Hostess with 90% brand awareness, helps to solidify leadership. TWNK’s popular portfolio of brands have translated into pricing power over its peers:

Source: Hostess Brands, Investor Presentation

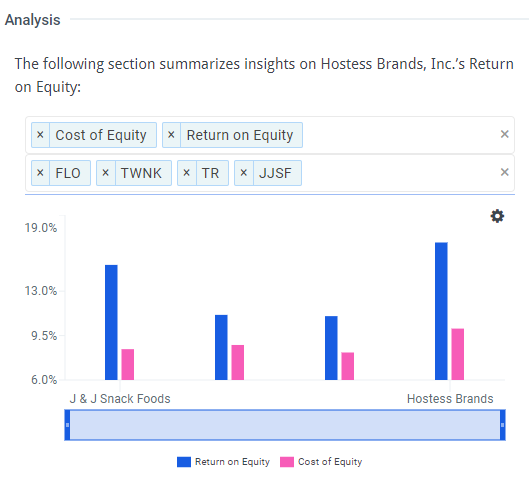

Compared to category leader Little Debbie, Hostess’ products garner roughly an 80% premium. Premium pricing boosts profits for retailers, strengthening their ties to Hostess. The pricing advantage also looks to support efficiency measures; TWNK’s return on equity (16.8%) versus its cost of equity (10%) compares favorably to direct peers:

Source: Hostess Brands, Return on Equity, finbox.io

Strategic Initiatives and Sources of Growth

Management has laid out a four-pronged approach for growth and efficiency, which includes expanding core distribution, product innovation, expanding white space, and acquisitions. Hostess has transitioned from a direct store distribution model to a warehouse model and management plans to leverage its favorable pricing economics to increase product-carrying stores.

Catering to the healthier eating trend, Hostess launched its Bakery Petites platform last year which features no artificial flavors or high fructose corn syrup. Management expects new product launches to post 1% growth in 2018. In-store bakery (ISB) also presents a source of growth, albeit at lower margins and a greater private label presence. Building on the Cloverhill bakery acquisition, Hostess is exploring opportunities in indulgent snacking and expanding ISB.

Estimating TWNK’s Intrinsic Value:

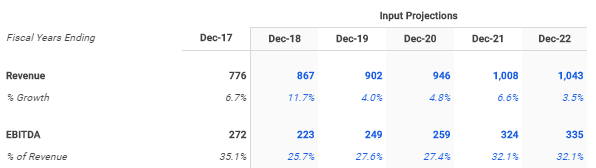

Incorporating these initiatives, Wall Street analysts see 11.7% revenue growth in 2018 and 25.7% EBITDA margin:

Source: Hostess Brands 5-Year DCF Model, finbox.io

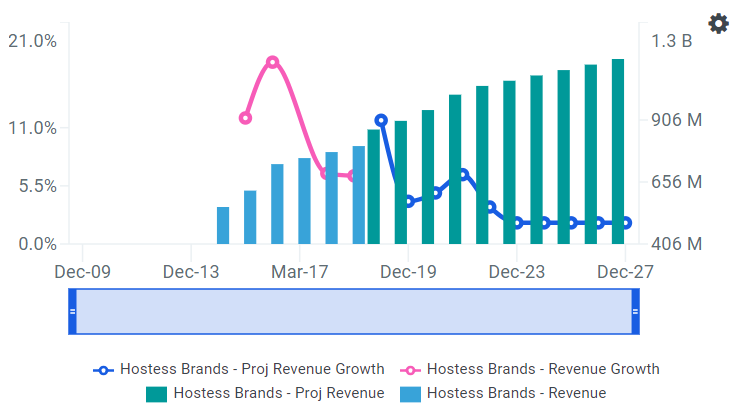

Over the next five years, revenue growth is expected to moderate to the mid-single digits as EBITDA margin expands.

Source: Hostess Bands, finbox.io Revenue Explorer

Assuming these forecasts across six Finbox.io valuation models produces an average estimate of intrinsic value of $15.54 per share. This suggests almost 15% upside to recent trading levels:

Source: Hostess Bands, finbox.io

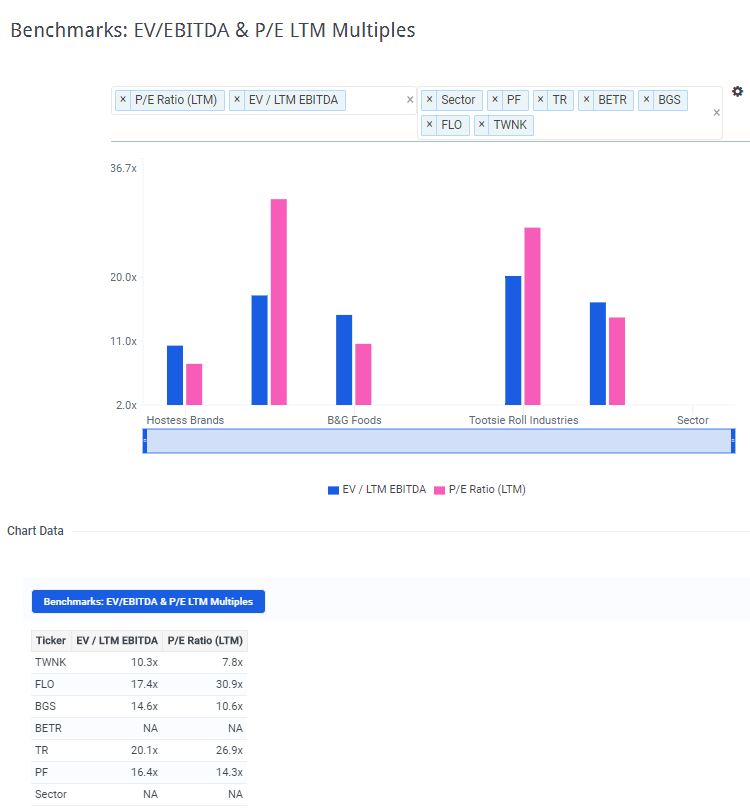

Wall Street’s consensus 1-year target is even higher at $16.91, implying almost 25% upside. A blended estimate of intrinsic value (50% Wall Street consensus and 50% Finbox.io) results in a $16.23 per share estimate, or almost 20% upside. TWNK looks priced favorably to peers based on enterprise value and P/E multiples as well:

Source: Hostess Brands, finbox.io Market Valuation

Risks:

Hostess Brands operates in a highly competitive industry with a trend towards healthier eating. Management’s ability to maintain market position and deliver on product innovation is significant. TWNK uses advance purchase contracts to lock in prices for raw materials, packaging, and fuel, but sustained volatility in these prices could affect profitability.

Hostess Brands Conclusion:

Buffett and Munger prefer to invest in companies that operate with strong pricing power. Hostess Brands has the ability to charge premium prices and product innovation looks to support growth. Trading with nearly 20% upside, value investors should give Hostess Brands a closer look.

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

{kind=link}