- Top brands that command premium pricing and customer loyalty can create significant competitive advantages over peers.

- General Mills, Inc (NYSE: GIS) offers a portfolio of leading brands and recently acquired high-growth pet food leader Blue Buffalo.

- Center-store weakness persists, but trading at 5-year lows and showing nearly 30% upside General Mills looks attractive for value investors.

The Power of a Brand

When Warren Buffett began practicing Benjamin Graham’s style of value investing, he didn’t give much thought to brands or business quality. Graham’s net-net strategy (stocks selling for less than net current assets) inherently provided the margin of safety that value investors require.

It was only when Charlie Munger introduced Buffett to the idea of the power of brands that Buffett tweaked his style. One of Buffett’s well-known successes with the investment shift was See’s Candies. To understand the power of See’s brand, Buffett once explained:

"If you give your girlfriend See's Candy and she kisses you, we've got you for life."

Later, Buffett recognized a similar brand loyalty from The Coca-Cola Co (NYSE: KO) customer:

“If you gave me $100 billion and said take away the soft drink leadership of Coca-Cola in the world, I’d give it back to you and say it can’t be done.”

That degree of brand power is rare, of course. Still, searching for solid brands at an attractive stock price was how Buffett evolved as a value investor.

Today’s value investors might consider consumer packaged foods leader General Mills (NYSE: GIS). General Mills offers a portfolio of well-known brands and finbox.io valuation models show nearly 30% upside.

The General Mills Business Model

General Mills’ generated $15.6 billion in consolidated net sales with an additional $1.0 billion from its proportionate share of joint venture net sales ($0.8 billion from Cereal Partners Worldwide and $0.2 billion from Häagen-Dazs Japan). The company is managed under four operating segments: North America Retail (65% fiscal 2017 net sales), Convenience Stores & Foodservice (12%), Europe & Australia (12%) and Asia & Latin America (11%). Products are split among five global categories including snacks, ready-to-eat cereal, convenient meals, yogurt, and super-premium ice cream:

Source: General Mills 2017 Annual Report

General Mills sells its products through retail stores and supplies products to the North American foodservice and commercial baking industries. Popular brands include Cheerios, Wheaties, Betty Crocker, Green Giant, Pillsbury, Haagen-Dazs, and Yoplait. Walmart Inc (NYSE: WMT) represented 20% of the company’s 2017 consolidated net sales and 29% of its North America Retail segment.

Latest Quarterly Results, “Moat” Analysis, and Growth Outlook

Third-Quarter Results

In its third quarter, General Mills posted a 1% increase in organic net sales and net sales increased 2% to $3.9 billion. The North America Retail unit sales were up 1% compared to the previous year. Results were helped by the Canada operating unit (6% increase), U.S. snacks (3%), and U.S. Meals & Baking (2%), but were pressured by U.S. Yogurt (-8%) and cereal (-1%).

Management cited increases in freight and commodity costs as weighing on its adjusted diluted EPS of $0.79 (an 8% increase in constant currency). To help offset these costs, strategic initiatives include increasing freight carriers and alternative transportation as well as optimizing the distribution network and its administrative structure.

The General Mills “Moat”

As management works to trim costs, General Mills’ strong lineup of brands and wide scale look to continue to give it a competitive advantage over peers. Cheerios, Honey Nut Cheerios, and Cinnamon Toast Crunch are all top-5 leading brands in ready-to-eat cereal. Leading brands including Old El Paso, Haagen-Dazs, Yoplait, and Pillsbury round out the rest of General Mills’ categories. The quality of these brands can command pricing power and superior shelf space over peers. General Mills’ wide distribution lowers unit costs versus smaller peers and its larger scale helps to maximize advertising’s impact. In all, it seems General Mills has built a significant competitive advantage versus its peers.

Sources of Growth

This isn’t to say that General Mills and other packaged food companies aren’t facing challenges. Center-store weakness (as customers move to fresher foods on the perimeter) has taken its toll. To compensate, management plans to reinvest in its brands and new products. Its acquisition of Blue Buffalo, while at a premium price, should also provide some support to top-line growth while supporting General Mills’ overall moat. Blue Buffalo is the leader (30%+ market share) in the U.S. pet food’s wholesome natural segment with 12% sales growth and a 25% EBITDA margin. Also helping margins is management’s targeting of $750 million in annual savings (including $50 million Blue Buffalo synergies).

Estimating Generals Mills’ Intrinsic Value

While Buffett moved on from Graham’s net-net strategy to buying quality brands, he still required his investments to trade at a reasonable discount, or margin of safety. Buffett held over this principle to provide protection against unfavorable business developments.

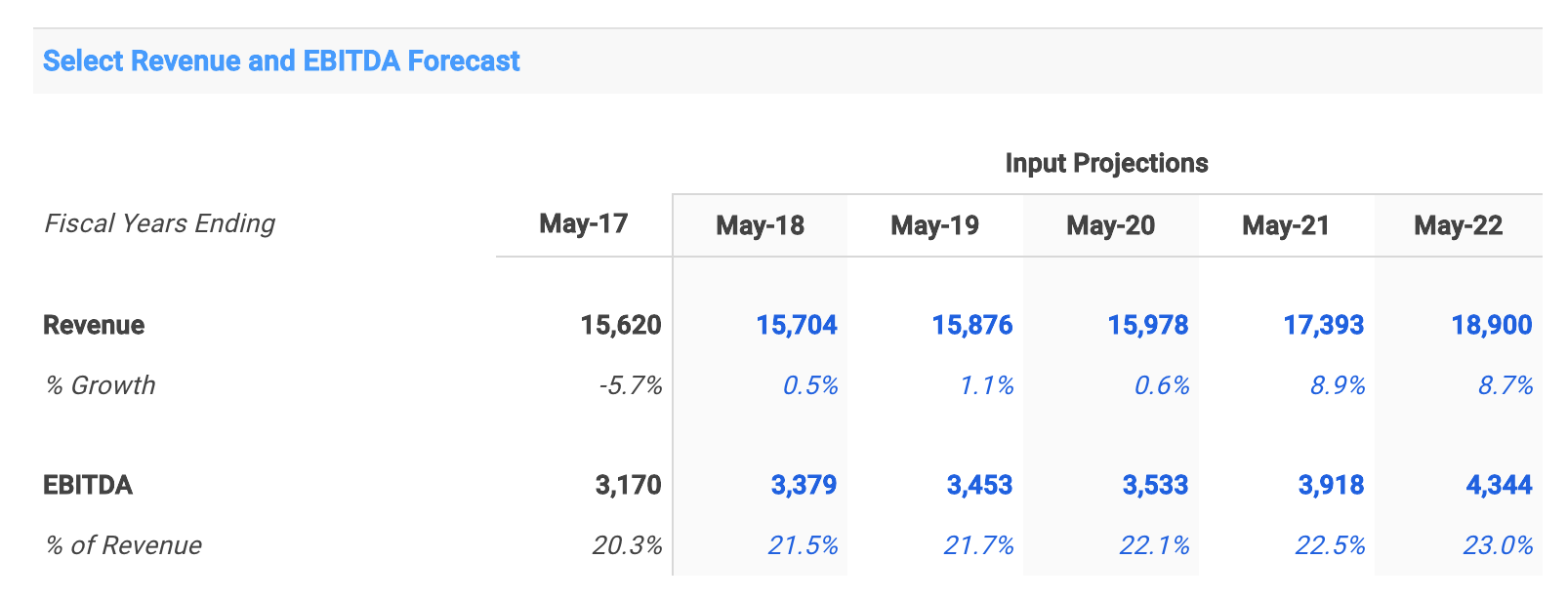

So does General Mills offer much in the way of a margin of safety? It sure looks like it. Wall Street analysts expect low single-digit revenue growth to ramp up into the high-single digits with steady EBITDA margin expansion:

Source: General Mills 5-Year DCF Model, finbox.io

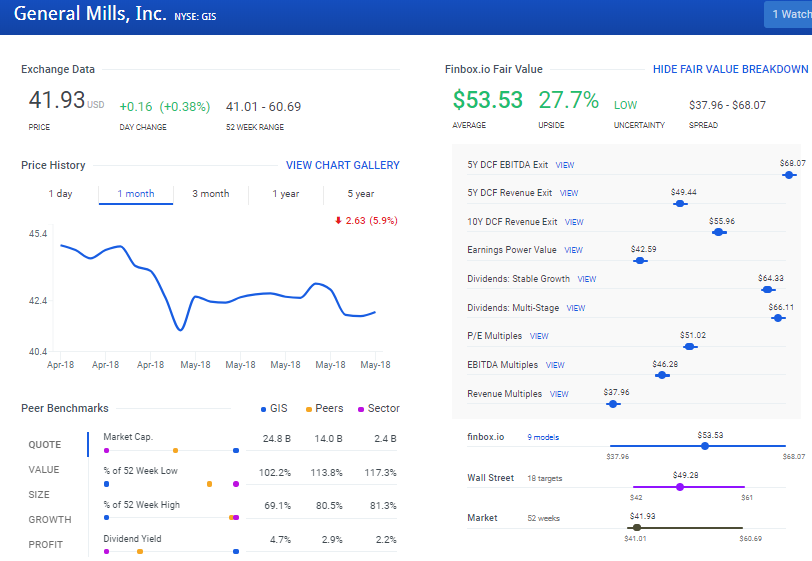

Incorporating these projections across nine finbox.io valuation models generates an average fair value of $53.53 per share. That estimate implies nearly 30% upside to current trading levels:

Source: finbox.io

That’s more upside compared to General Mills’ direct peers and its dividend yield also compares favorably:

Risks:

Greater-than-expected weakness in the center store could weigh on General Mills’ top line. Volatile commodity costs and increased competition from incumbents and smaller players also pose risks. The Blue Buffalo integration and capturing the targeted $50M in synergies could also prove challenging.

General Mills Conclusion:

With a portfolio of leading brands and a recent acquisition of another, General Mills offers the high-quality brands that value investors seek out. Though customers have prioritized perimeter store offerings of late, brand reinvestment and new product development look to support the top line. With a 4.7% dividend yield and 30% upside, it’s time value investors give General Mills another look.

Photo Credit: General Mills 2017 Annual Report

Author: Andy Pai

Expertise: financial modeling, mergers & acquisitions

Andy is also a founder at finbox.io, where he's focused on building tools that make it faster and easier for investors to do investment research. Andy's background is in investment banking where he led the analysis on over 50 board advisory engagements involving mergers and acquisitions, fairness opinions and solvency opinions. Some of his board advisory highlights:

- Sears Holdings Corp.'s $620 mm spin-off via rights offering of Sears Outlet, Hometown Stores and Sears Hardware Stores.

- Cerberus Capital Management's $3.3 bn acquisition of SUPERVALU Inc.'s New Albertsons, Inc. assets.

Andy can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

{kind=link}