- While U.S. stocks have shown resilience, the maturing bull market and a flattening yield curve suggest caution is warranted.

- In this environment, value-priced stocks with businesses that benefit during an economic pullback appear to be worthy of consideration.

- Leading discounter Dollar Tree Inc. has become a popular alternative to mass-merchants and Finbox.io valuation models show almost 15% upside to recent trading levels.

Downside Focus

While assessing a stock’s upside is imperative, some of the most respected investors begin with a shift in focus: the downside. Top value investor Seth Klarman has gone so far as to make it a central tenet to his investing philosophy:

“Loss avoidance must be the cornerstone of your investment philosophy.”

With stock market indices hitting or approaching new records daily, it can be easy to get fixated on returns even in the face of lofty valuations. That may be a recipe for disaster, however, in this aging bull market:

“The road to long-term investment success runs through risk control more than through aggressiveness.”

Cautionary words from value investor Howard Marks, whose investment writings Warren Buffett highly admires. An investor wanting to acknowledge today’s risks might put more of a focus on the flattening yield curve, inflation at 6-year highs, and high levels of corporate debt.

How can one position themselves amid today’s threats? Businesses that benefit during general economic weakness is a place to start - especially when those businesses are trading at a discount to their intrinsic value.

Consumer defensive stock and leading discount variety store Dollar Tree, Inc. (NASDAQ: DLTR) could see an uptick in business during economic weakness. Additionally, Finbox.io valuations show almost 15% upside to recent trading levels. Let’s take a closer look at Dollar Tree’s business model, recent results, and growth prospects.

Dollar Tree’s Business Model

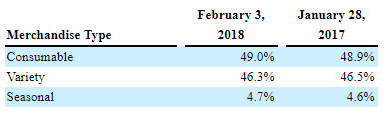

Dollar Tree is the largest discount retailer in North America with over 14,900 stores (225 stores in Canada). The company operates with two reporting segments: Dollar Tree and Family Dollar. Dollar Tree is the leader in offering merchandise at the fixed $1 price point. Goods include Consumable (candy and food, health and beauty care, and everyday consumables), Variety (toys, durables, gifts, etc.) and Seasonal. Percentage of sales for each product group:

Source: Dollar Tree 10-K

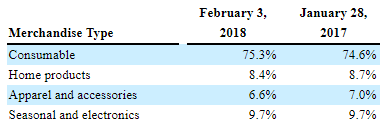

The Family Dollar segment includes its neighborhood variety stores offering goods between $1 and $10. The merchandise mix includes Consumable (food, tobacco, health and beauty, pet food, etc.), home products (housewares, home décor, giftware, and domestics), apparel and accessories, and seasonal and electronics:

Source: Dollar Tree 10-K

Recent Results, Competitive Position, and Sources of Growth

First Quarter 2018 Results

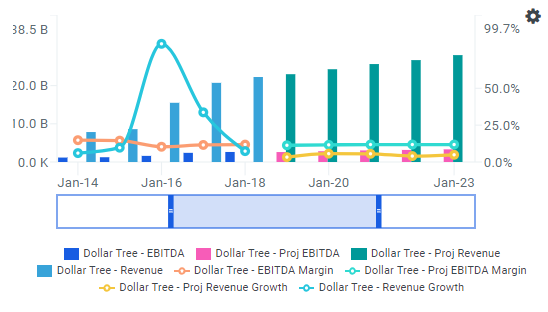

Dollar Tree’s sales grew 5% to $5.55 billion in its fiscal first quarter while same-store sales increased 1.4%. The Dollar Tree segment showed consistent comp growth at 4%. The Family Dollar banner was off 1.1% due to apparel and lawn and garden misses attributed to the colder-than-normal spring and early Easter.

Operating income increased to $437.6 million versus $388.8 million in the prior year period; adjusted net income grew 21.4% to $1.19 per share versus $0.98. Cash and cash equivalents totaled $475.2 million.

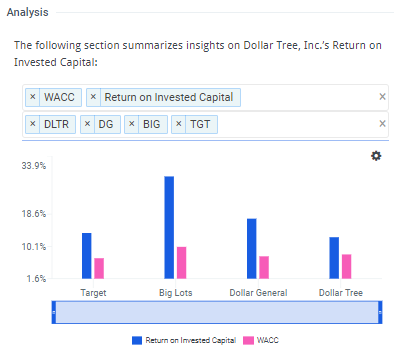

Assessing DLTR’s Moat

Dollar Tree has been able to generate returns on invested capital (12.5%) above its cost of capital (8%), consistent with several of its peers:

Source: Dollar Tree, Return on Invested Capital, Finbox.io

This suggests that Dollar Tree does benefit from a moderate moat or competitive advantage versus smaller players. With the acquisition of Family Dollar, Dollar Tree’s increased size helps its bargaining power during the procurement process. Its store count and relatively closely-positioned stores also help to reduce Dollar Tree’s distribution costs.

While the shift to online commerce has squeezed mass merchants’ margins, discounters have been relatively more immune to the trend. In addition, consumers are increasingly viewing discounters as a mass-merchant alternative. Dollar Tree and Family Dollar’s ability to charge higher prices than mass merchants for consumers prioritizing convenience provides another boost to DLTR’s return on invested capital.

Growth Outlook

Dollar Tree opened 130 new stores (68 Dollar Trees and 62 Family Dollars) in the first quarter bringing its total to 14,957 stores. Management has stated its belief to support up to 25,000 stores in the United States. To help increase foot traffic, Dollar Tree has added more consumables and has rolled out frozen and refrigerated foods. After adding freezers and coolers to 104 Dollar Tree stores in the first quarter, over 5,300 Dollar Tree stores now include the offering.

Dollar Tree’s Fair Value:

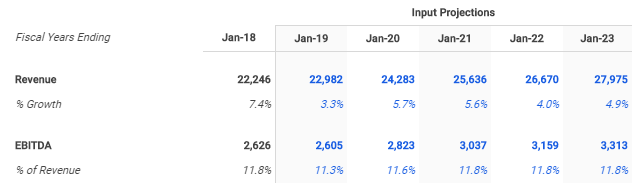

Dollar Tree’s competitive advantages and management’s growth plans appear to have the company positioned well. How will this translate into the company’s financials going forward? The consensus Wall Street estimate for 2019 is 3.3% revenue growth and 11.3% EBITDA margin:

Source: Dollar Tree 5-Year DCF Model, finbox.io

Over the longer term, analysts expect revenue growth to increase into the mid-single digits. EBITDA margin is also expected to expand slightly.

Source: Dollar Tree, finbox.io Revenue Explorer

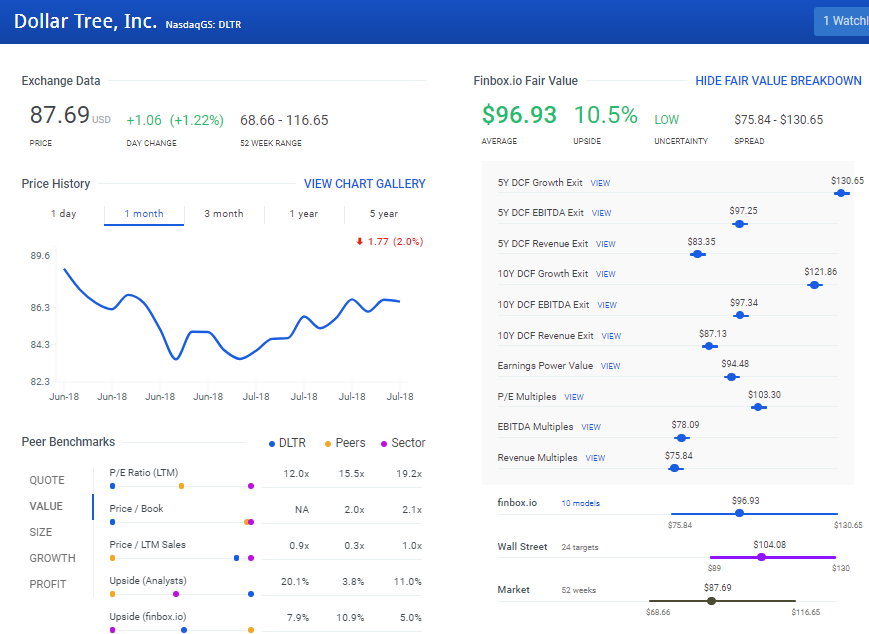

Using these estimates in ten Finbox.io valuation models generates an average estimate of fair value of $96.93 per share. This implies 10.5% upside to recent trading levels:

Source: Dollar Tree, finbox.io

The 1-year consensus from Wall Street is a bit higher at $104.08, or 18.7% upside. Using a blended valuation (50% finbox.io and 50% Wall Street) generates a $100.60 per share estimate of intrinsic value, or almost 15% upside.

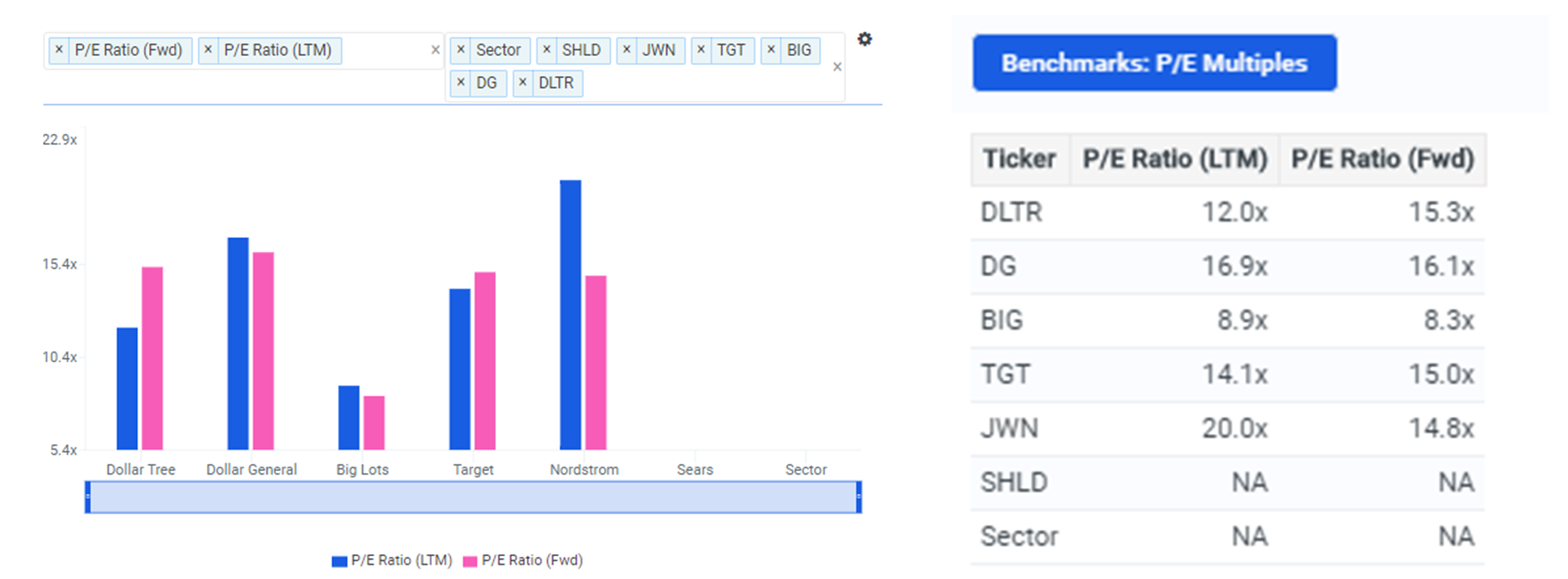

On a price-multiples basis, Dollar Tree also looks attractive relative to direct peer Dollar General:

Source: Dollar Tree, finbox.io Market Valuation

Risks:

The proliferation of deep discounters like Aldi and Lidl along with competition from mass merchants could pressure Dollar Tree’s prices. Any significant shift in social benefits or higher costs affecting discretionary income also pose risks. Fully optimizing the Family Dollar acquisition also could prove challenging.

Dollar Tree Conclusion:

Though the stock market has shrugged off negative news lately, complacency towards downside risks can become problematic. Consumer defensive stocks trading at discounts to fair value can serve as a hedge.

Dollar Tree earns returns on invested capital in line with businesses displaying a moderate competitive advantage and management’s initiatives look to support growth. Showing almost 15% upside to recent trading levels, Dollar Tree appears worth a closer look ahead of its earnings announcement next month.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

{kind=link}