- Macro data shows that a sustained upswing in the economy should continue to drive a strong housing market.

- Through a regional and diversified price-point strategy, management has put D.R. Horton in a great position to profit as Millennials buy starter homes, families go bigger, and empty nesters downsize.

- Shares of the company look highly attractive after falling 13.6% over the last 30 days in the face of rising mortgage rates.

Squeezing the Most Out of the Cyclical Upswing

Homebuilding is a cyclical industry, which means that companies need to profit during economic expansions without building a house of cards that won’t survive a downswing. In determining if a homebuilder can continue to grow over the next year, an investor must be confident that homes remain affordable, and demand will continue to expand along with the economy, i.e. the market is not over-supplied.

Inflation is an indicator of a growing economy, but also means home prices are rising. It results in part from wage growth, which means workers are better off financially. Containing inflation is one of the Federal Reserve’s mandates and have been slowly hiking interest rates in the hope of keeping a lid on prices without slowing the economy. The Fed can, directly and indirectly, control rates, and its economic outlook heavily influences Treasury yields and mortgage rates.

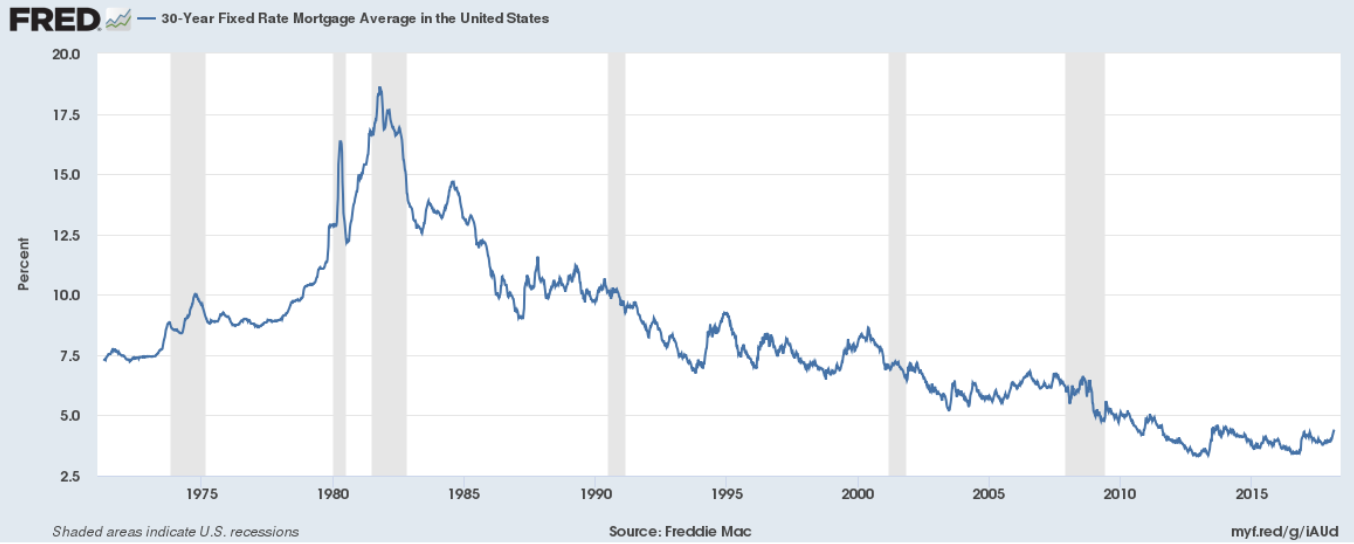

The Fed recently reiterated their positive outlook and expectations for three rate hikes in 2018 to keep inflation around 2%. This will drive mortgage rates up, meaning home buyers will have higher payments. However, as seen in the chart below of 30-year mortgage rates, rates are still historically low, and have a lot of room to rise before impacting the market.

Source: Freddie Mac

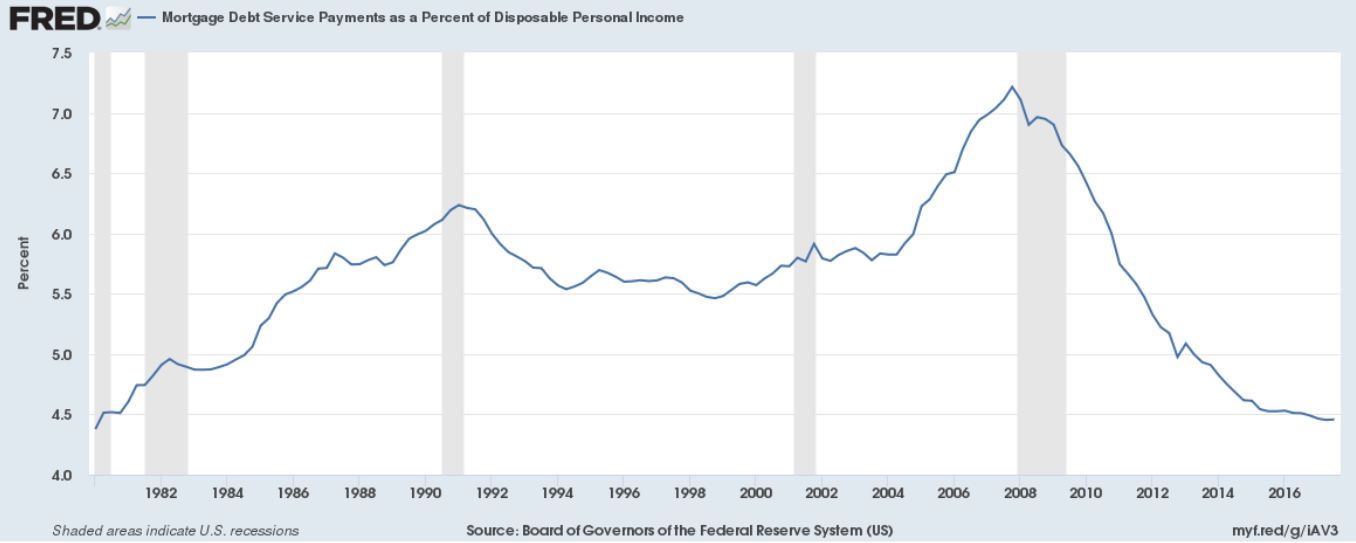

Also indicating that buyers will not be negatively impacted in the near-term by inflation is another historically low rate, that of mortgage payments as a percent of disposable personal income. This affordability metric is affected by both rates and home prices; thus, high home prices are also a concern.

Source: Federal Reserve

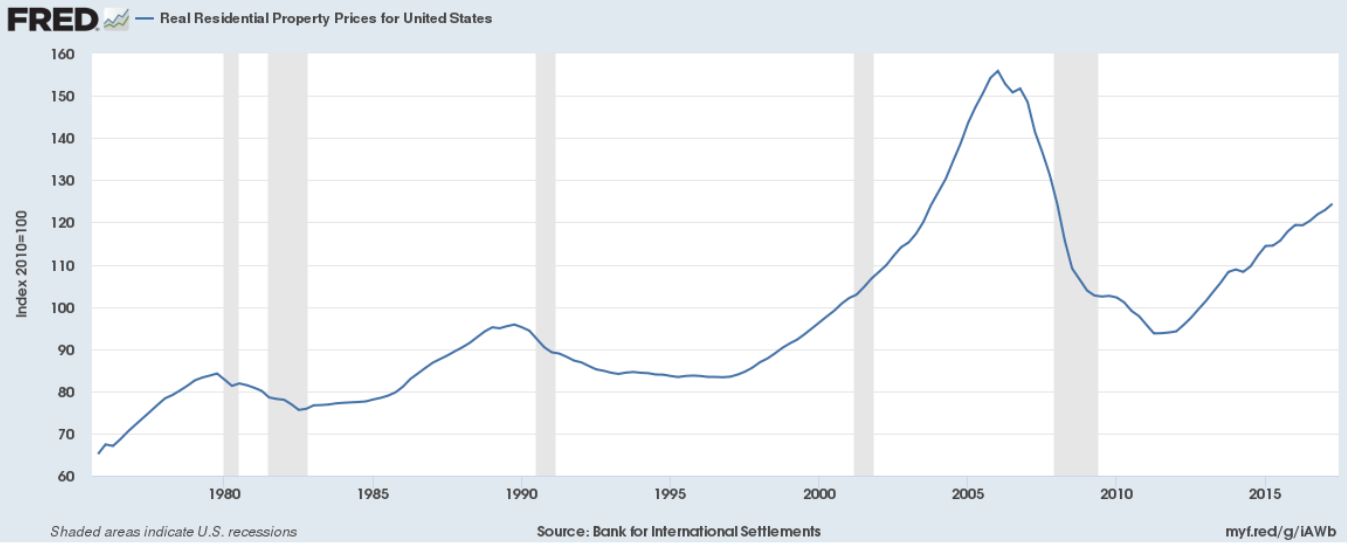

Home prices have been steadily rising. This is expected in a growing economy, and it can be noted that the economy’s growth has offset higher prices. While prices have been increasing since 2010 as seen below, affordability, as shown above, has continued to improve.

Source: Federal Reserve

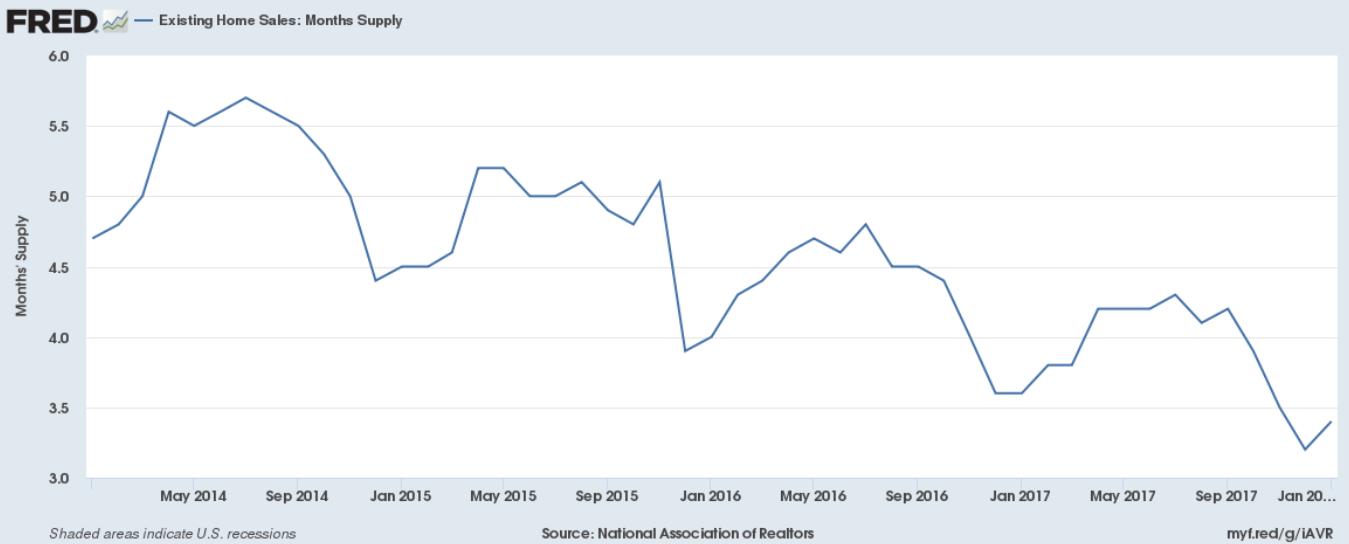

With buyers able to afford houses, the question is, can they find them? A good measure of availability is months supply of homes available. The fewer months of supply available to the market, or fewer homes for sale, the stronger demand is. This is also a positive metric for home builders who can add new supply to a tight market. Buyers of homes also have a better experience dealing with builders, as a tight market means that they are probably losing out to all-cash offers, stuck in bidding wars, or not even getting to see the house due to immediate above listing price offers. With home builders, house hunters can build a home from scratch or buy a spec house – one that was built on the homebuilder’s dime that can be moved into relatively quickly.

Source: National Association of Realtors

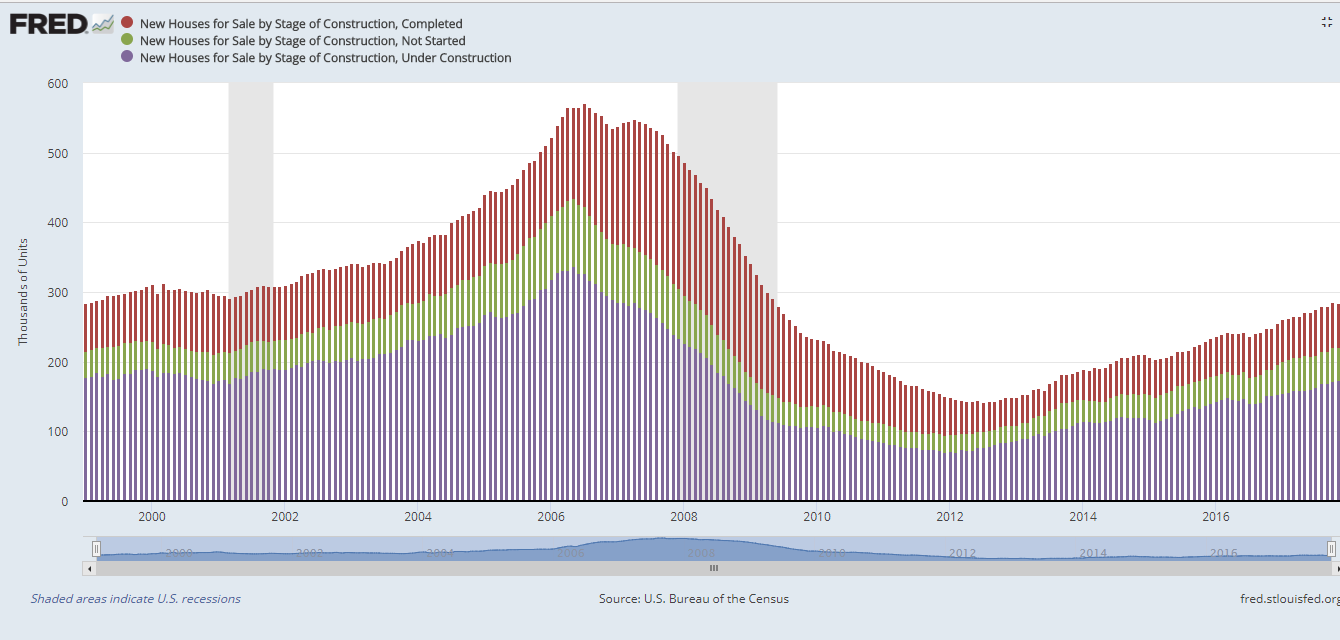

The good news is that it does not look like home builders are as overexpanded as they were in the last bubble. New homes for sale are just reaching levels from back in 2000, and builder inventory, as indicated by the red bar, is healthy, but not high, for a strong economy.

Source: U.S. Census

The sustained upswing in the economy should continue to drive the housing market while affordability does not appear to be a concern. A home builder that attacks multiple price points is in a great position to profit as Millennials buy starter homes, families go bigger, and empty nesters downsize. D.R. Horton, Inc. (NYSE: DHI) has done an excellent job of this by offering four distinct price brands.

D.R. Horton Investment Case

D.R. Horton is a well-positioned homebuilder that’s run by a strong management team (as illustrated by superior margins/returns relative to peers and sector). It has built the most houses in the industry for 16 consecutive years after growing from a local Texas homebuilder to serving 26 states within 79 markets. Management has focused on the single-family market, and expanded to become a full-service experience including financing and title insurance.

Source: finbox.io

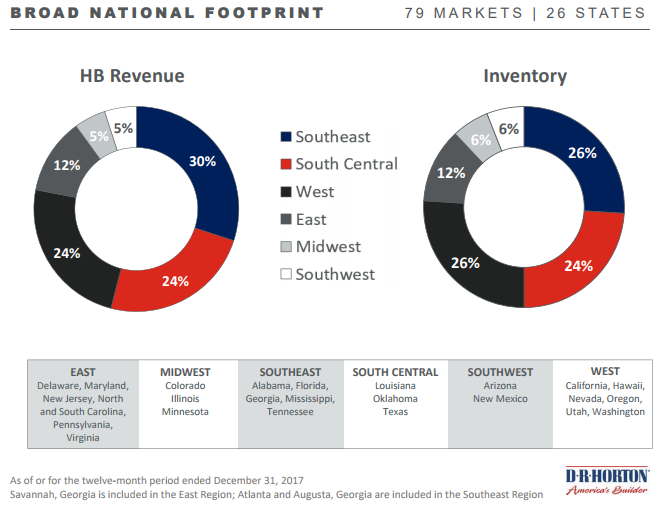

The company’s revenues are geographically diverse, with three regions generating around 25% each. This broad footprint reduces risks to regional shocks and provides the builder ample opportunity to profit from an expansion.

Source: [D.R. Horton Q1 2018 Investor Presentation](http://investor.drhorton.com/~/media/Files/D/D-R-Horton-IR/Q1 2018 Investor Presentation.pdf)

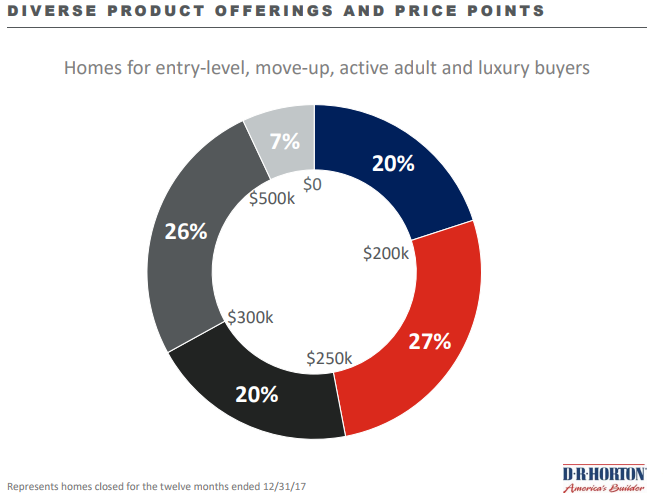

D.R. Horton’s ability to offer four distinct price-based brands also separates itself from the smaller builders. Its units sold are evenly spread across the affordability spectrum.

Source: D.R. Horton Q1 2018 Investor Presentation

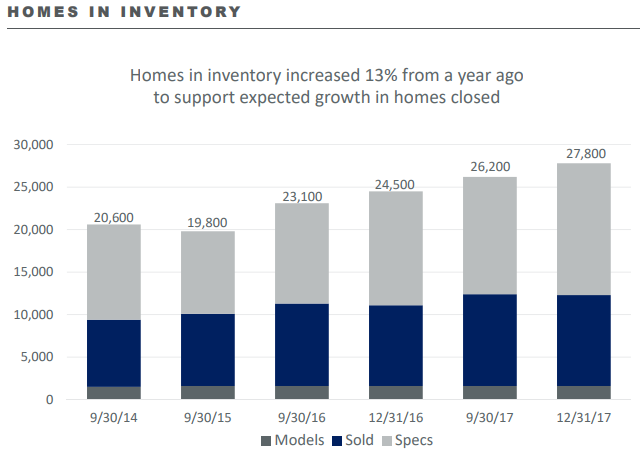

As noted earlier, it does not appear that homebuilders have overexpanded themselves. Overexpansion can be seen in inventory (unsold homes) and lots/land. DHI’s inventory has grown but seems reasonable for the state of the economy.

Source: D.R. Horton Q1 2018 Investor Presentation

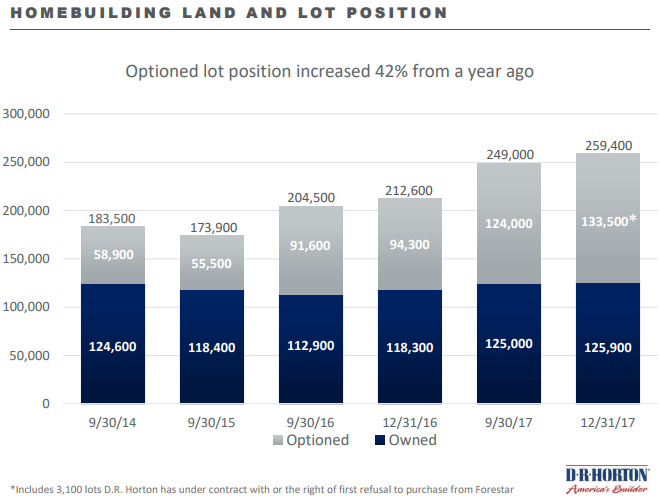

To grow, builders must also have land to use. D.R. Horton’s acquisition of Forestar in 2017, a residential developer, added lots and options on lots for the company. As economic expansion matures, homebuilders should be prepared for a downturn. The graphic below indicates that DHI is positioning itself strategically by assuring its upside, but protecting the downside, by increasing lot options rather than buying real estate.

Source: D.R. Horton Q1 2018 Investor Presentation

Providing a full-service offering for a complex purchase (like that of a home) aids in creating a better customer experience. Driving buyers to your own mortgage company is a no-brainer, especially since more than 73% of new homes are bought with conventional mortgages. According to company guidance, the financial services arm is expected to generate a 30% operating margin in 2018. Sales for this division also increased 18% YoY for fiscal 2017. However, this is still truly a convenience for customers, as its revenues are only 3% of sales.

D.R. Horton Valuation: 30% Add-on

Source: finbox.io

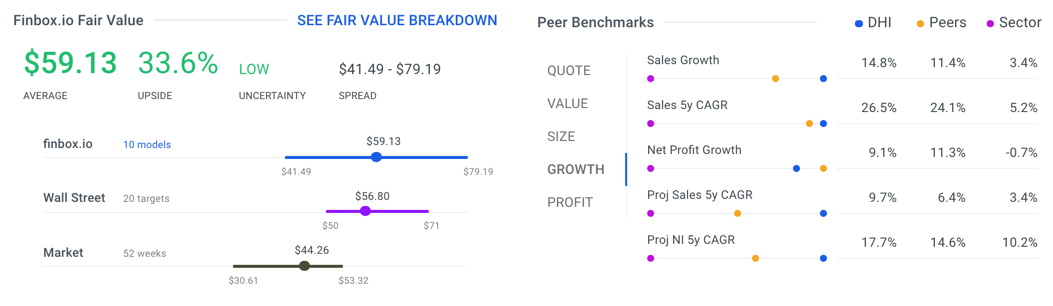

Finbox.io’s dashboard provides investors with a quick valuation overview with the ability to get under the hood of a stock quickly. Starting with expectations for DHI, the fair value section shows that both Wall Street analysts and quantitative risk models conclude impressive upside. The agreement of 20 professional analysts and 10 separate valuation models adds confidence to this positive outlook.

For further confirmation, peer comparisons can add context to how attractively the stock is priced. A quick look at the Peer Benchmark section shows that the homebuilder’s growth metrics outpace its peers and sector in almost every case.

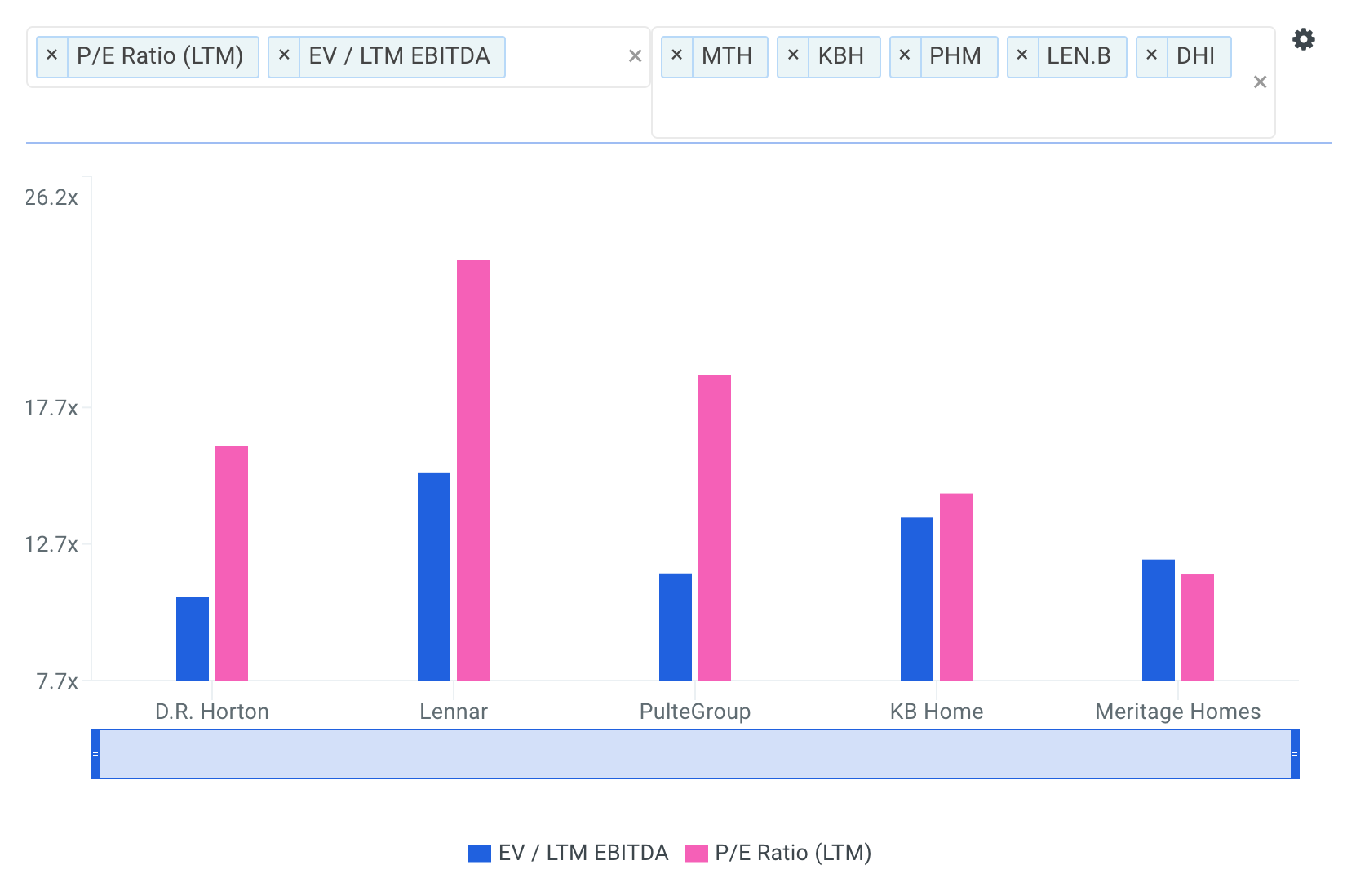

Further peer analysis can be accomplished using price multiples to help show if the builder is priced inline with similar stocks. DHI has the second lowest P/E among its four peers indicating a mild undervaluation. However, earnings are not always a great apples to apples comparison due to differences in capital structure. Therefore, it is also helpful to look at EBITDA multiples as a check. In this case, EV / EBITDA shows the stock is trading at a discount to its entire peer group.

Source: finbox.io

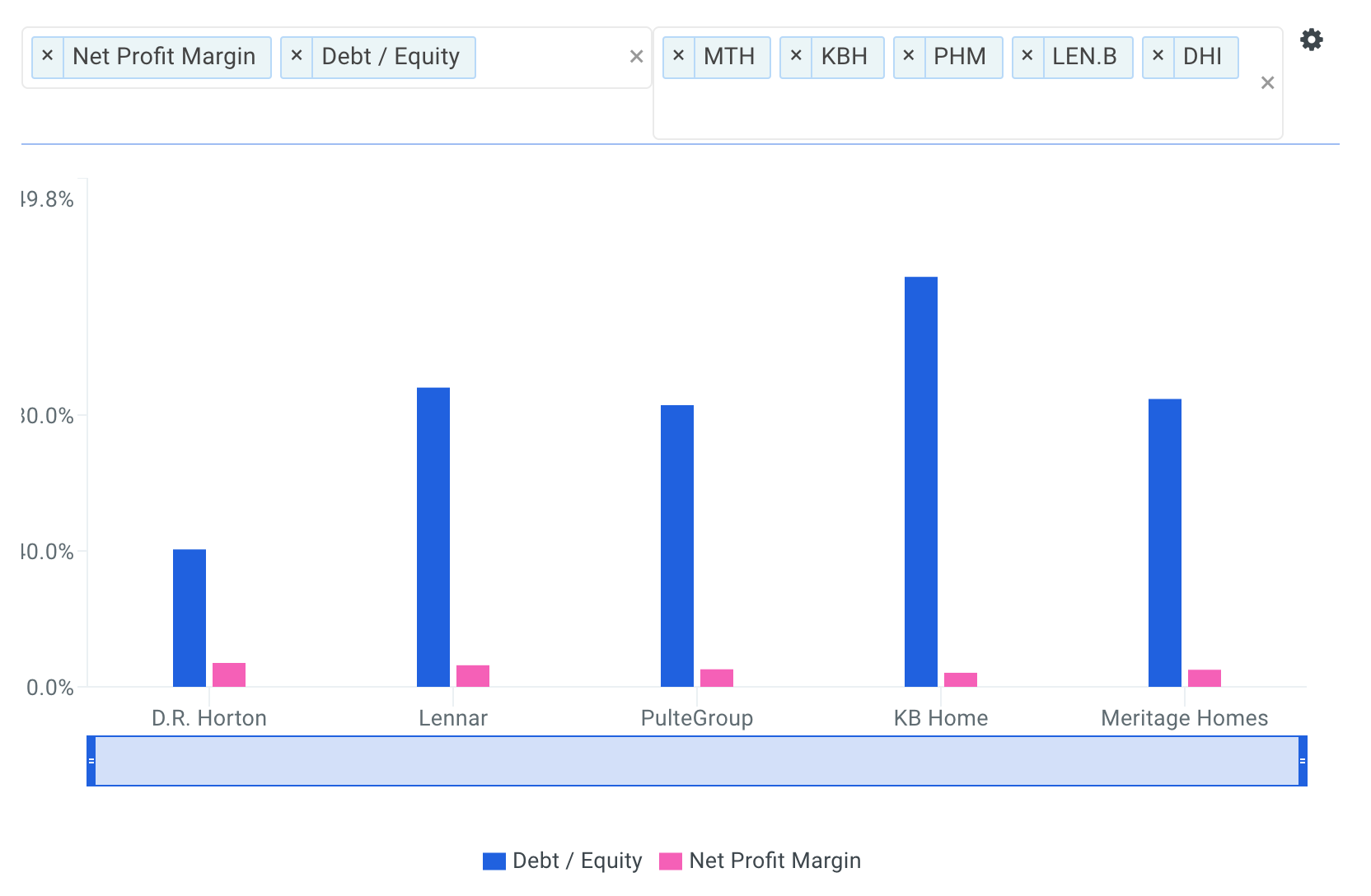

Operating margins in addition to low debt makes the stock even more attractive. D.R. Horton has the best net profit margin amongst its peers as illustrated below. In addition, the company’s Debt/Equity ratio is lower than its peers, indicating that it may be better able to weather any storms.

Source: finbox.io

D.R. Horton Conclusion: Foundation In Place For 30% Gain

The firm’s regional and price-point diversity strategy has been paying off. With a strong economy, and a housing market that is hot, but not too hot, DHI is in a great position to squeeze more earnings out of this economic expansion.

Wall Street, finbox.io’s fair value estimate, and trading multiples all support at least 30% upside potential. Management has positioned the company to outperform with a broad footprint strategy, scale, strategic acquisitions, better margins, and a low debt level.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

{kind=link}