Earnings Preview

Dollar General’s (NYSE:DG) is expected to report earnings on Thursday before the market opens. The company's shares last traded at $72.78 as of Tuesday afternoon, approximately 74% of its 52 week high. Dollar General’s stock has traded lower in the aftermath of Target’s (NYSE:TGT) disappointing earnings results which were announced on February 28th. Target's CEO Brian Cornell subsequently noted that the retail industry is seeing a seismic shift in buying trends as consumers turn to digital resources and focus on pricing.

<img width="80%" src='http://res.cloudinary.com/finbox/image/upload/v1489534295/DG_Stock_Price_own066.jpg' alt= ‘Dollar General (DG) Stock Price Chart’>

More recently, Buckingham Research downgraded Dollar General shares citing that the company faces increasing margin competition, with Wal-Mart (NYSE:WMT) and Target both aggressively looking to take market share.

With unfavorable news dragging shares lower, could now be the time to buy? Below I use the company’s historical performance to help project future cash flows to help answer this question.

Historical Performance

Dollar General’s revenues have grown from $11.8 billion in fiscal year 2010 to $21.3 billion in the last twelve months (LTM) as of October. However, the chart below illustrates how the company’s revenue growth has declined from nearly 15% to 6% over the same period. This deceleration has investors concerned.

<img src='http://res.cloudinary.com/finbox/image/upload/v1489534295/DG_Revenue_Chart_nv33sc.jpg' alt= ‘Dollar General (DG) Revenue Growth Chart’>

Although top line growth has come down, 6% growth is not terrible. Especially when considering a weak US economy that's growing barely above inflation.

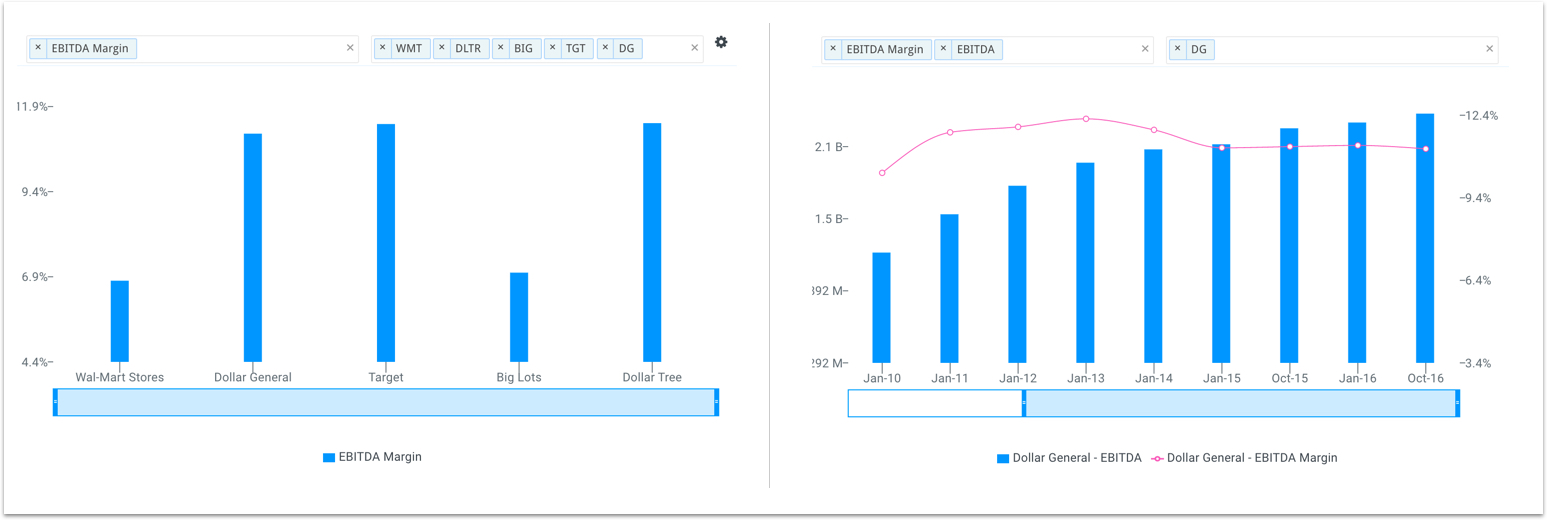

Another concern is related to the company's margin compression. While Dollar General’s EBITDA has continuously grown since 2010, margins have been under pressure since 2014. The company’s 11.1% LTM EBITDA margin is at its lowest level since 2010. In addition, Wall Street projects this figure to decline to 10.6% by fiscal year 2021.

<img src='http://res.cloudinary.com/finbox/image/upload/v1489534290/DG_EBITDA_Margins_rajoja.jpg' alt= ‘Dollar General (DG) Peer EBITDA Margin Chart’>

It is no surprise that investors prefer companies with increasing margins but is an 11% or even 10% cash flow margin that bad? It sure doesn’t look bad when compared to Big Lots (NYSE:BIG) and Wal-mart’s sub 7% margin. Additionally, Dollar General's EBITDA margin is only slightly below Target’s and Dollar Tree’s (NasdaqGS:DLTR).

Projected Performance

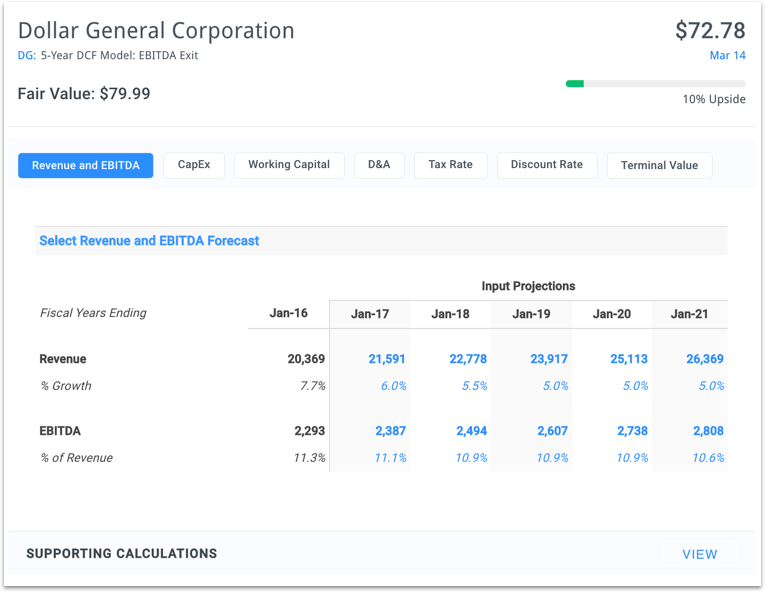

I projected revenue and EBITDA for the next five years based on recent developments and the company's historical performance. The forecast below estimates revenue growth at roughly 5% over the next five years and EBITDA margins to decline to 10.6% by fiscal year 2021. These assumptions are fairly conservative based on Dollar General’s historical performance and Wall Street’s expectations. Comparatively, Wall Street has revenue and EBITDA reaching $28.5 billion and $3.1 billion by 2021, respectively.

<img src='http://res.cloudinary.com/finbox/image/upload/v1489534290/DG_Forecast_juvupo.jpg' alt= ‘Dollar General (DG) Discounted Cash Flow (DCF) Analysis’>

View full DG DCF analysis

Applying the forecast above in finbox.io’s discounted cash flow (DCF) analysis results in an intrinsic value of approximately $80 per share. This implies that Dollar General’s stock is 10% undervalued based on its recent $72.78 trading price.

Final Notes

Overall, demand for the company's merchandise is generally stable and not widely affected by changes in the economy. This helps make Dollar General's cash flows less risky than other retailers like Wal-Mart and Target. As a result, the assumptions in the discounted cash flow (DCF) analysis could actually be too conservative which would imply that Dollar General is more than 10% undervalued. Not a ridiculous thought considering the company’s shares were trading above $95 last July.

Value investors may want to take a closer look at the stock prior to earnings on Thursday.

Get Started Now!

photo credit: Rita Reviews

Note this is not a buy or sell recommendation on any company mentioned.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}