- Businesses that benefit from a “network effect” can differentiate themselves from peer companies and enjoy strong customer loyalty. Value investor Warren Buffett has frequently and recently targeted these types of businesses.

- eBay Inc’s (NASDAQ: EBAY) leading Marketplace unit appears to benefit from such a network effect; management’s latest improvement initiatives look to enhance the dynamic.

- While retail e-commerce competition is strong, eBay’s stock price offers 25% upside to recent trading levels, providing downside protection for value investors.

Targeting Network Effects

The big news from Berkshire Hathaway (NYSE: BRK.B) last week was Warren Buffett’s targeting of leading ride-hailing firm Uber Technologies. While the $3B proposed deal ultimately didn’t materialize, the interest from Berkshire is in line with one of Buffett’s preferred investment strategies.

Buffett provided insight into this strategy in his 1989 annual letter to Berkshire shareholders:

"In other instances, a great investment opportunity occurs when a marvelous business encounters a one-time huge, but solvable, problem as was the case many years back at both American Express Company (NYSE: AXP) and GEICO. Overall, however, we've done better by avoiding dragons than by slaying them.”

Uber’s string of problems over the past year is no secret, satisfying Buffett’s “huge problem” criteria. And Buffett has long admired new CEO Dara Khosrowshahi, implying his confidence in solving Uber’s problems. But what evidence is there of Uber being a “marvelous business?”

Buffett likes to invest in companies with wide moats or strong competitive advantages; one type of a moat comes in the form of a network effect. A network effect develops when a company’s products and services become more valuable to its customers the more customers it attracts. Like American Express and GEICO that Buffett mentioned, Uber’s customers benefit when more drivers and ride-hailers use the service (for example, more riders attract additional drivers, which cuts down on wait times).

A network effect is powerful and when value investors can identify one within a stock trading at an attractive price, it can present a great investment opportunity. eBay’s (NASDAQ: EBAY) commerce business appears to benefit from such a network effect (more on that below) and its current stock price implies nearly 25% upside. As such, let’s take a closer look at eBay’s competitive position and how management is navigating a challenging retail environment.

eBay’s Business Model

eBay is a global commerce leader through its Marketplace, StubHub, and Classifieds platforms. Marketplace includes the www.ebay.com and mobile platforms; StubHub is eBay’s online ticket platform www.stubhub.com and Classifieds offer online classifieds through mobile.de, Kijiji, Gumtree, and other brands.

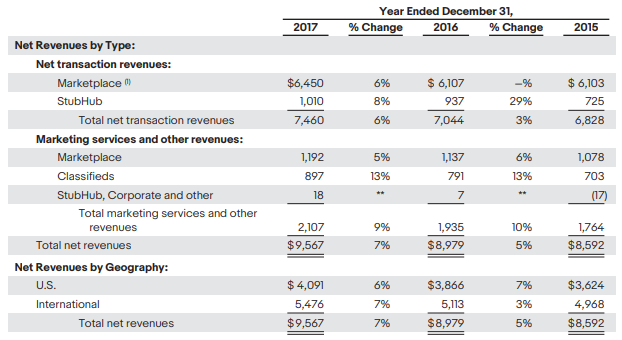

Revenues are generated both as fees on transactions (fees payable on Marketplace and StubHub platforms) as well as marketing services (advertising and marketing fees):

Source: eBay 2017 Annual Report

International revenue contributed 57% of total net revenue in 2017 with the U.S. market providing the balance. eBay’s $88 billion in gross merchandise volume (GMV) represented roughly 4% of the world e-commerce market.

First Quarter Results, Assessing eBay’s Network Effect, and Growth Prospects

Latest Quarter Results

In eBay’s 2018 first quarter, its top line increased 7% (currency-neutral basis) YoY to $2.6B with total GMV up by the same percentage. Trailing 12-month active buyer growth was up 4% YoY to 171 million (25M+ active buyers); the deceleration of 1% compared to the previous quarter was attributed to Korea and eBay.com short-term headwinds. Cost of revenue declined 60 bps with customer service and Korea inventory investments offsetting savings and site operations.

GAAP EPS came in at $0.40 versus $0.94 the prior year, which was supported by a non-cash income-tax benefit of $695M. End-of-quarter cash and short-term investments stood at $4.8 billion with debt of $9.3 billion.

eBay’s “Network Effect”

With such a large base of active buyers and sellers, eBay appears to benefit from a network effect. Smaller firms looking to enter the space have much to overcome in selling their value propositions. eBay’s take rates (7.69% and 22.35% for Marketplace and StubHub, respectively) also compare favorably to an estimated 15% for Amazon.com, Inc (Nasdaq: AMZN). eBay’s partnership with payments company Adyen should also lower costs, thereby improving the seller experience and supporting eBay’s network effect. In all, it appears eBay maintains a moderately-sized moat, or competitive advantage, against peers.

Management Initiatives and Sources of Growth

Management is working on its “back-to-basics” strategy, in part, to compete against Amazon’s own third-party platform enhancements. The strategy includes streamlined listing processes, data-driven merchandising, and AI investments. As far as growth, StubHub poses a source of long-term growth and an agreement to acquire Giosis’ Japan business provides exposure to a leading e-commerce, high mobile adoption market.

List Price: Valuing eBay

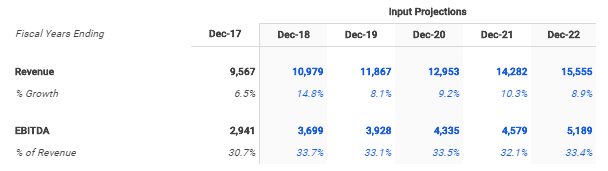

Wall Street analysts expect mid-teen, top-line growth and EBITDA margin expansion from 30.7% to 33.7% in 2018:

Source: eBay 5-Year DCF Model, finbox.io

Source: eBay, finbox.io Revenue Explorer

Thereafter, revenue is expected to experience high-single-digit growth with relatively steady EBITDA margin. Using these assumptions across nine of finbox.io’s valuation models produces an average fair value estimate of $45.97 per share, or 15% upside to recent trading levels. Wall Street’s 1-year target price is even higher at $48.47, providing nearly 25% upside:

Source: finbox.io

Risks:

A competitive e-commerce environment including large players such as Amazon (and its third-party offerings) loom. The effectiveness of management’s “back-to-basics” plan is significant. Adverse economic conditions and a weakening consumer along with foreign currency and data security also pose risks.

eBay Conclusion:

Buffett’s targeting of companies with “marvelous businesses” often feature businesses that benefit from a strong network effect. eBay’s Marketplace unit offers such a dynamic and management’s efforts to improve its service offerings look to support this source of what appears to be a moderately-sized moat.

Management needs to continue to drive organic traffic, but eBay’s current stock price offers downside protection with nearly 25% upside. Buffett-style value investors should take a closer look at eBay ahead of its earnings announcement next month.

Author: Matt Hogan

Expertise: Valuation, financial statement analysis

Matt Hogan is also a co-founder of finbox.io. His expertise is in investment decision making. Prior to finbox.io, Matt worked for an investment banking group providing fairness opinions in connection to stock acquisitions. He spent much of his time building valuation models to help clients determine an asset’s fair value. He believes that these same valuation models should be used by all investors before buying or selling a stock.

His work is frequently published at InvestorPlace, Benzinga, ValueWalk, AAII, Barron's, Seeking Alpha and investing.com.

Matt can be reached at [email protected].

As of this writing, I did not hold a position in any of the aforementioned securities and this is not a buy or sell recommendation on any security mentioned.

{kind=link}