Akamai Technologies (Nasdaq:AKAM) is the world’s largest content delivery network (CDN) provider for media and software delivery related solutions. Generally, the company engages in services to make the Internet fast, reliable and secure.

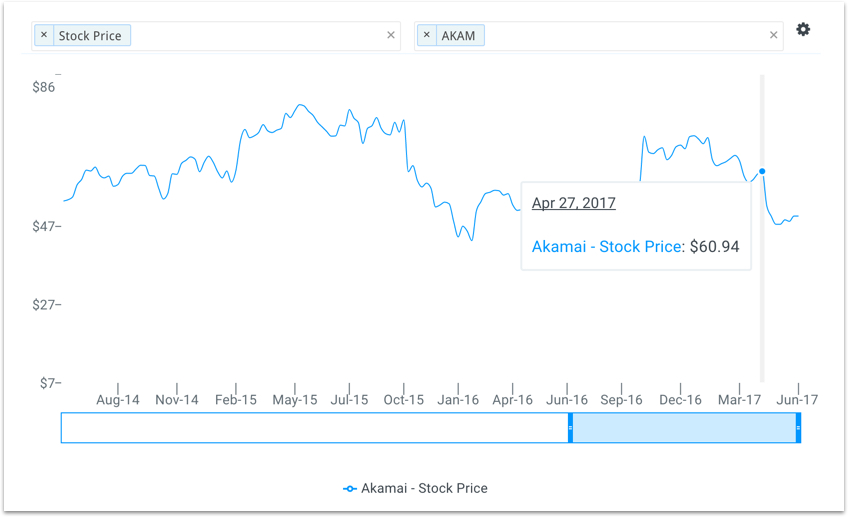

Shares of Akamai Technologies have trended lower after the company beat both its Q1’17 earnings and revenue estimates but offered disappointing Q2’17 guidance. This clearly disappointed investors as the stock has since lost over 20% of its value. However, the sharp selloff of AKAM shares may have created an opportunity for investors.

As Warren Buffett stated in his 2004 annual shareholder letter, “be fearful when others are greedy and greedy only when others are fearful.”

Here’s why value investors may want to be greedy as it relates to Akamai Technologies.

A High Growth Industry

Technology strategist Michael Wolf predicts that internet access providers will see their revenues grow at an average rate of 6.3% a year from 2016 to 2021, via the Wall Street Journal.

Media consumption across the globe is increasingly prevalent in digital formats. The increase in the number of devices capable of supporting digital media along with faster internet speed, has provided consumers with an option to access media content from anywhere. Simply put, anyone with a smart phone can catch up on news, entertainment or their social activity anytime and virtually anywhere.

Media consumption in the US has shown tremendous growth and has seen a significant jump away from traditional media to new (digital) media. More and more media consumption is happening on digital formats and people also spend more time on digital media as compared to traditional media. This industry tailwind is a very positive sign for shares of Akamai Technologies.

A Sharp Sell Off

The company beat its Q1’17 revenue estimate by $4.5 million and per-share earnings estimate by $0.02. However, management warned investors that Q2’17 revenues would likely fall short of estimates by $20 million.

The weak Q2 guidance was a disappointing surprise and, as expected, the stock dropped. But shares dropped in excess of 16% which appears to be an overreaction especially when revenues and earnings are still growing.

<img src='http://res.cloudinary.com/finbox/image/upload/v1497971322/AKAM_Stock_Price_s7ozra.jpg' alt= ‘AKAM Stock Price Chart’>

Source: finbox.io

Furthermore, the company’s margins are fairly stable, has a cash heavy balance sheet, generates strong cash flows and has a long term growth story that looks promising.

Akamai Transitions Toward More Profitable Security Market

Akamai's cloud security sales increased 44% in 2016 and show no signs of slowing down. Content delivery revenue dropped 10%, but the company seems quiet comfortable with its new entry into the security market.

This is likely because the cloud security market is anticipated to expand at a CAGR of 12.8% from 2015 to 2022.

The security focused future looks bright for the AKAM shares.

Two Major Catalysts Driving AKAM Shares

-

The continued shift from linear TV to internet TV. Over-the-top (OTT) video consumption is performance-sensitive, especially when dealing with high definition and/or live streaming. This will help increase demand for AKAM’s high-quality offerings.

-

The shift in the gaming world towards augmented reality or virtual reality also creates demand for AKAM solutions as these services are also performance sensitive.

In both the media and gaming industries, the major product categories are moving towards performance sensitive mediums. AKAM is able to differentiate itself through quality which will help stimulate demand and ultimately growth.

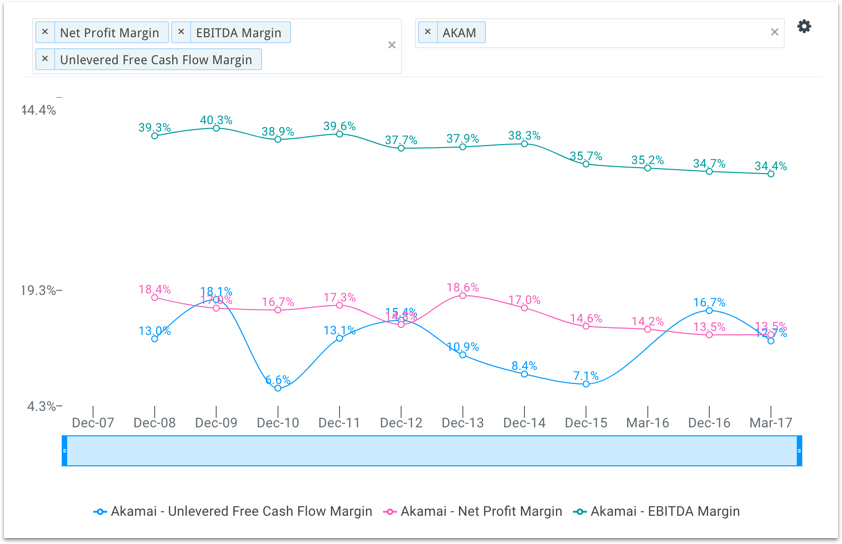

Strong Financials

AKAM’s cash flows are strong and have been strong since 2007. Although the company’s EBITDA and Net Profit margins have trended slightly lower over the last few years, free cash flow margins have improved.

<img src='http://res.cloudinary.com/finbox/image/upload/v1497971322/AKAM_Margins_b85sah.jpg' alt= ‘AKAM Cash Flow Margins Chart’>

Source: finbox.io

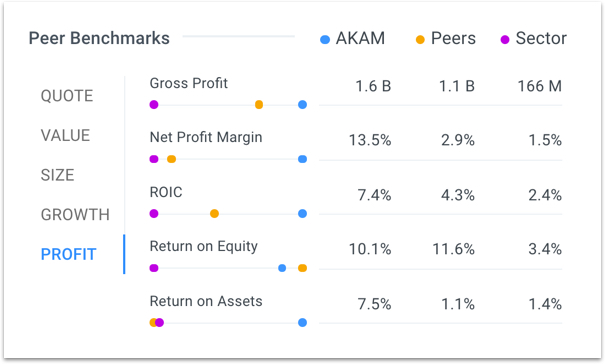

AKAM’s margins and returns are also very impressive when compared to its peers and the sector average as illustrated below.

<img src='http://res.cloudinary.com/finbox/image/upload/v1497971322/AKAM_Peer_Chart_bdkx1p.jpg' alt= ‘AKAM Peer Comparison Chart’>

Source: finbox.io

The CEO Likes The Valuation

CEO Tom Leighton bought 21,196 shares of AKAM stock on May 31st at an average price of $47.17. He then bought another 20,397 shares at an average price of $49.02 on June 15th illustrating how undervalued Mr. Leighton believes the stock trades.

Finbox.io's eight valuation models conclude an average fair value price target of $60.51 per share, well above its current trading price of around $49.50. Wall Street’s consensus is even higher than the finbox.io average fair value at $62.68. Overall, the eight models and 22 Wall Street targets imply that the stock is 20%-25% undervalued.

<img src='http://res.cloudinary.com/finbox/image/upload/v1497971321/AKAM_FV_wbfrqh.jpg' alt= ‘AKAM Finbox.io Fair Value Estimate’>

Source: finbox.io

With strong fundamentals in place, consistent margins and strong industry tailwinds, Akamai Technologies investors can expect above average returns at current prices.

Note this is not a buy or sell recommendation on any company mentioned.

Photo Credit: bidnessetc

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}